在伊朗战争的大部分期间,投资者普遍押注不会发生经济灾难;即使石油和天然气价格大幅上升,也被认为只是“痛苦”而非毁灭,除非涨幅足以压垮霍尔木兹海峡燃油需求并引发衰退和高通胀。结果是大宗商品已抬升但未到灾难区间,计划中的海峡重启暂时印证了这种乐观,股债双双反弹,标普500指数仅比一月下旬的历史高点低约3%。

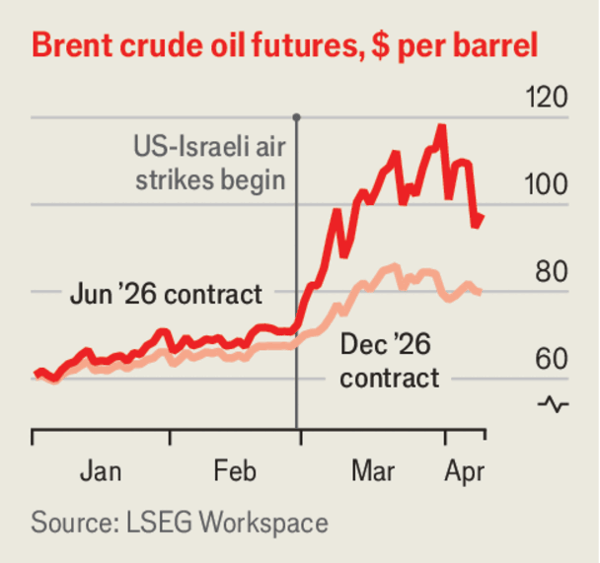

海湾国家已把原油产量下调了1,000万桶/日,约占全球供应的10%,并且恢复产能、重新调配油轮以及支付更高保险费都需要时间;即便制裁未彻底解除,伊朗可能新增通行费也会继续带来不确定性。期货已将年底布伦特油价定在约75美元,约高于2026年初预期的四分之一,其他大宗商品也存在同类后遗症,包括天然气、石化、氦和铝;卡塔尔拉斯拉凡在无人机袭击中已损失17%产能,修复将耗时,而化肥短缺已扰乱北半球及非洲部分地区的播种季,预示着食物供应下降和全球饥荒风险上升。

综合效应是拖累全球增长并明显推高通胀,促使央行把利率维持在略高水平并压低投资回报,同时企业在已经历COVID、俄乌战争和美国关税之后,还必须把政治、流行病和战争风险作为新的附加代价。市场之所以出现“特氟龙”式弹性,来自纪律化治理和适应能力,但尾部风险仍然庞大,从台湾危机到AI危机皆在列;能源对单一海湾水道的依赖正推动长期向可再生能源、更多天然气来源及美国2010年代页岩革命这样的技术转向,而这类技术同样根源于20世纪70年代的能源危机,并有望帮助全球避免重现70年代式衰退。

Investors largely bet through most of the Iran war that no economic catastrophe would occur; even a major oil-and-gas price spike was seen as painful but not disastrous unless it rose high enough to crush fuel demand through Hormuz and trigger recession and high inflation. As a result, commodity prices rose but stayed below disaster levels, and the planned reopening of the strait briefly validated that optimism as both stocks and bonds rallied and the S&P 500 remained only about 3% below its late-January record.

Gulf countries have cut crude output by 10 million barrels per day, about 10% of global supply, and rebuilding output, re-routing tankers, and paying higher insurance will all take time; Iranian tolls could add further uncertainty even if no full settlement succeeds. Futures already imply Brent near $75 by year-end, roughly 25% above expectations at the start of 2026, with similar hangovers in gas, petrochemicals, helium, and aluminium, while Qatar’s Ras Laffan lost 17% capacity in a drone attack and fertilizer shortages have already disrupted planting in the Northern Hemisphere and parts of Africa, pointing to reduced food supply and a higher global hunger risk.

The combined effect is to weaken global growth and push inflation materially higher, leading central banks to keep rates modestly higher and lowering investor returns, while firms add political, pandemic, and war risk premiums after already absorbing shocks from Covid, the Ukraine war, and U.S. tariffs. The “Teflon economy” image reflects market resilience and policy discipline, but large tail risks remain—from a Taiwan crisis to an AI crisis—and dependence on one Gulf waterway is now reinforcing a long-term shift to renewables, diversified gas supplies, and technologies like the U.S. 2010s shale boom, whose roots date to the 1970s oil shocks and could help avoid another 1970s-style slump.

Source: A ceasefire will not prevent the Iran war’s economic harm

Subtitle: Even if the Strait of Hormuz reopens, expect lasting change to energy markets

Dateline: 4月 09, 2026 05:12 上午