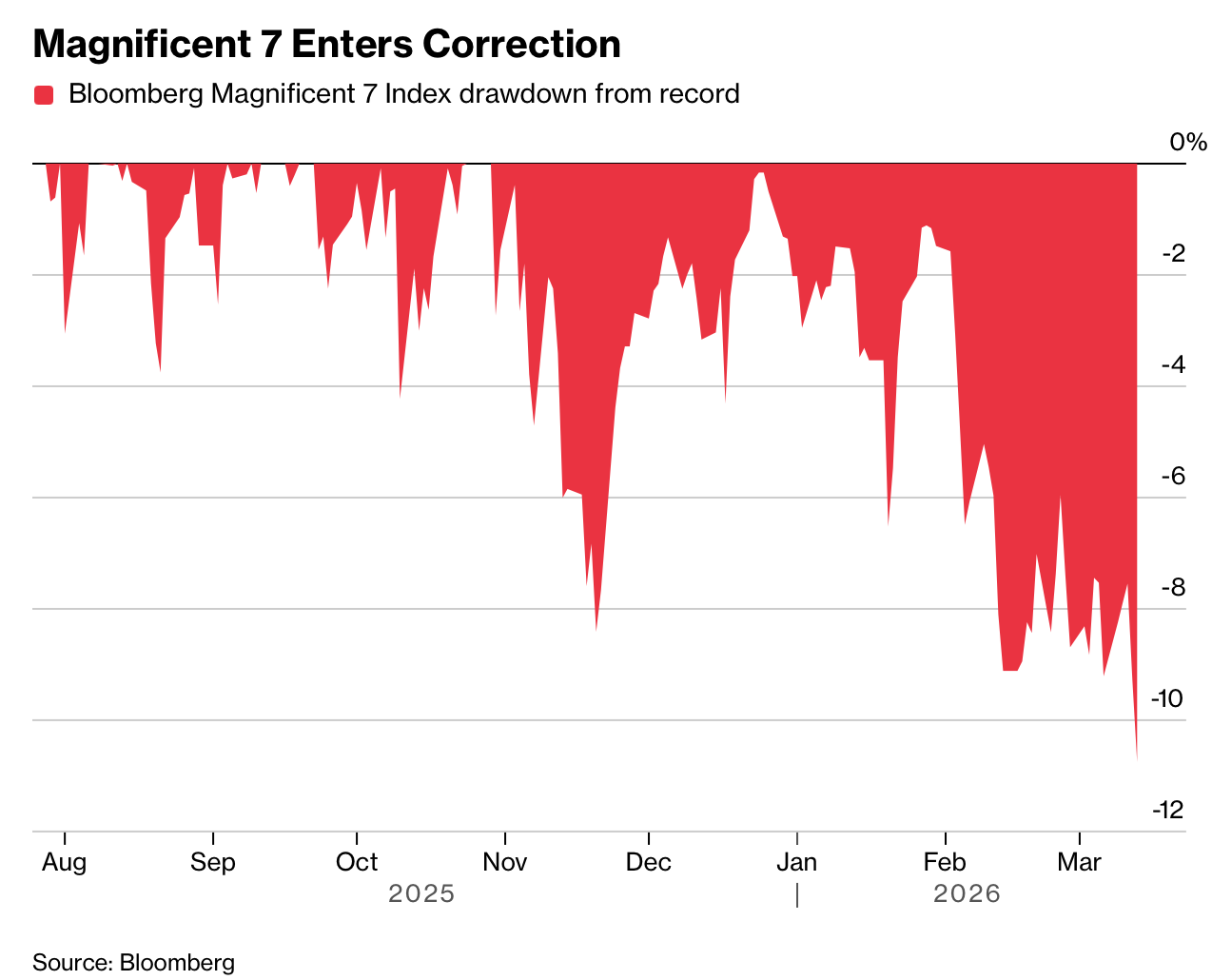

“Magnificent Seven”大型科技股指数在2026年3月进入技术性回调区间。该指数收盘较2025年10月的历史高点下跌超过10%,达到市场通常定义的回调门槛。最近两天跌幅加速:周四下跌1.9%,周五再跌1.6%。这一变化标志着过去三年强劲上涨趋势的逆转。在此前周期中,该指数在2023年上涨107%,2024年上涨67%,2025年上涨25%,成为推动标普500牛市的重要力量。2026年迄今,七家公司股价全部转为负收益。

投资者情绪转弱主要与人工智能投资回报不确定性和宏观风险上升有关。大型科技公司已承诺投入数千亿美元发展AI,但盈利路径仍不清晰,使投资者开始质疑资本支出规模。同时,新AI工具可能对软件等行业产生颠覆效应,加剧市场不确定性。其中Microsoft表现最弱,年内股价下跌超过18%。在地缘政治方面,美国与伊朗战争以及油价上涨进一步增加市场波动,促使资金从高风险资产转向更防御性的能源和公用事业板块。

尽管价格回调,这些公司的估值仍高于整体市场。一些投资者认为大型科技公司仍具备“避险资产”特征,因为其盈利增长稳定、资产负债表强劲且对大宗商品价格依赖较低。例如一家管理约27亿美元资产的投资机构指出,大型科技公司的盈利收益率接近美国国债收益率水平,因此仍能提供相对稳定回报。对这些投资者而言,当前超过10%的回调意味着潜在的折价买入机会。

The “Magnificent Seven” mega-cap technology stock index entered a technical correction in March 2026. The index closed more than 10% below its October 2025 record, the commonly used threshold for a correction. Losses accelerated over two sessions, falling 1.9% on Thursday and another 1.6% on Friday. The shift marks a reversal from the strong rally of the previous three years, when the group rose 107% in 2023, 67% in 2024, and 25% in 2025, driving much of the S&P 500 bull market. In 2026 so far, shares of all seven companies have turned negative.

Investor sentiment has weakened due to uncertainty about returns on artificial intelligence investments and rising macro risks. Large technology firms have pledged hundreds of billions of dollars to develop AI, but the path to profitability remains unclear, prompting investors to question capital spending levels. At the same time, new AI tools may disrupt industries such as software, adding further uncertainty. Microsoft has been the biggest laggard, with shares down more than 18% this year. Geopolitical tensions related to the US war with Iran and rising oil prices have also increased volatility and pushed investors toward defensive sectors such as energy and utilities.

Despite the price decline, valuations for the group remain higher than the broader market. Some investors argue that mega-cap technology stocks still function as relative safe havens because of strong earnings growth, solid balance sheets, and limited exposure to commodity prices. One asset manager overseeing about $2.7 billion noted that big tech earnings yields resemble US Treasury yields, suggesting stable return potential. For these investors, the more than 10% correction represents a potential discounted buying opportunity.