油价上涨对企业是双重打击:先是投入品与运营成本上升压缩利润率,随后消费者因生活开支被挤压而削减可选支出。美国几乎所有家庭都有车且多半拥有两辆以上,汽油从每加仑约3美元升至4美元后,典型家庭每年将多花约1000美元,约占可支配支出的八分之一,并且自伊朗冲突后,油价已从2026年初约每桶60美元波动到约100美元,终端油价也从2月末的每加仑3美元升到4美元。

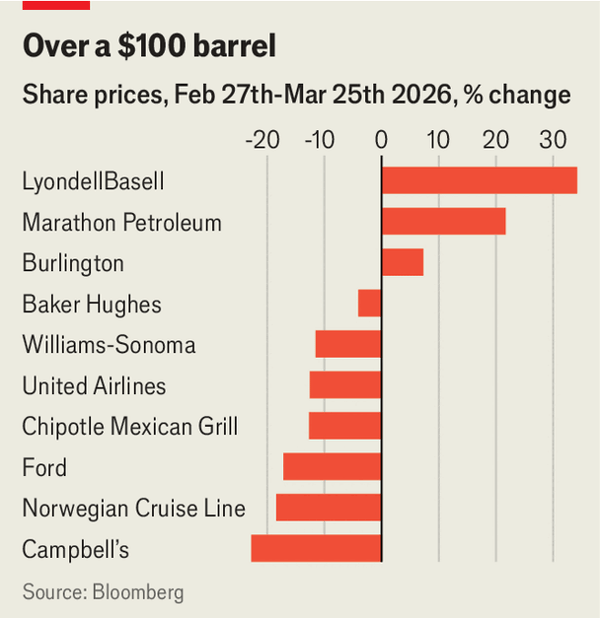

美国企业出现明显的“输赢”分化:自2月27日以来,石油天然气板块上市公司平均上涨超过8%,而航空板块却承压,American Airlines下跌20%、United下跌13%,Delta仅因其拥有约四分之三国内燃油供应的宾州炼厂而上涨3%。可选消费股Chipotle、Nike与Williams Sonoma自2月末分别下跌12%到15%,但LyondellBasell与Dow约涨30%,CF Industries也受益上涨,且打折连锁Burlington过去一个月上涨约7%;相比之下,Campbell’s与General Mills在战争后均下跌超过20%,超市型企业如Costco、Kroger和Walmart则大致持平。

总体上,市场预期企业将面临更高成本和更谨慎消费者,油田服务商Baker Hughes在中东项目担忧后回落到危机前略低水平,暗示对“油价上涨→产量大幅反弹”持怀疑。若油价高位持续,汽车行业受创更明显:Ford和General Motors自战争开始以来股价转弱,BYD同比上涨15%,电池龙头CATL涨幅更高,类似1970年代油价冲击导致美国汽车厂商受挫、消费者从高油耗车型转向日本高效车型的历史轨迹值得关注,这场冲击的商业后果可能长期延续到战争结束之后。

Rising fuel prices hit businesses in two stages: first through higher input and operating costs that squeeze margins, then through consumers cutting discretionary spending after essentials take priority. With almost all U.S. households owning at least one car and most owning two, moving from about $3 a gallon to $4 adds roughly $1,000 per year for a typical family, about one-eighth of discretionary spending, and since the Iran strike the oil market has moved from about $60 a barrel at the start of 2026 to around $100, with pump prices already up to $4 from $3 at the end of February.

U.S. equities show sharp winner-loser splits: listed oil-and-gas firms are up over 8% on average since Feb. 27, while airlines are weak (American -20%, United -13%) except Delta, which is up 3% after insulating about three-quarters of its domestic fuel with a Pennsylvania refinery. Discretionary names Chipotle, Nike and Williams Sonoma are down 12–15%, but LyondellBasell and Dow are up about 30% and CF Industries has also surged as cheap North American gas offsets higher hydrocarbon input costs; Burlington is up around 7%, whereas Campbell’s and General Mills are down more than 20%, with grocery competitors like Costco, Kroger and Walmart largely flat as shoppers shift to private labels.

Investors generally expect tighter cost conditions and more frugal buyers, and Baker Hughes trading just below pre-crisis levels suggests skepticism that higher fuel prices will trigger a major production rebound. Automakers are already under pressure, with Ford and General Motors weakening since the conflict, while BYD is up 15% and CATL even more as the shock revives the case for reduced gasoline demand and stronger electrification, echoing the 1970s episode when Detroit was hurt as consumers moved from gas-guzzlers to Japanese fuel-efficient cars; the effects are likely to persist after the conflict ends.

Source: The war’s biggest corporate winners and losers may surprise you

Subtitle: Markets are beginning to signal the long-term consequences of the surge in fuel prices

Dateline: 3月 26, 2026 04:46 上午 | Washington, DC