驱动这一转型的是价格结构,而非叙事偏好。太阳能在中午同时发电,造成短时过剩,压低批发电价至低值甚至负值。南澳在 2025 年 12 月季度的日照时段,批发电价有 88% 时间低于 0。收益最高时段反而在晨晚尖峰,亦即面板输出较弱之时。对专案开发商而言,单纯加大面板配置的回报被侵蚀;相对地,电池、氢能与追日系统可将低价中午电力移转至高价时段。随著电池成本在过去一年下降 26%,太阳能加储能组合正更频繁地低于最便宜化石燃料机组的成本,同时提供可调度、较稳定的供电。

文章将此视为成熟技术的典型演化,而非衰退讯号。随著光伏在澳洲、智利、荷兰与西班牙等市场已提供超过五分之一发电量,未来几年更多市场可能复制同一路径,且大型太阳能专案将愈来愈常与电池、电解槽或其他备援打包销售。地缘政治也强化此趋势:相较受冲突扰动的 LNG 供应链,再生能源资产一旦部署可运行数十年。历史上 IBM 与 Texas Instruments 在产品商品化后转向高附加价值环节并在近六个月创名目市值高点;但 Blackberry、HP、Intel、Nokia 的案例也提示,若商业模式创新速度落后技术创新,制造商将被淘汰。

The article’s central claim is that the most important new trend in solar is not newer panel formats, but major manufacturers moving into anything other than panels themselves. Chinese firms produce more than 80% of global modules, yet leading companies are shifting growth toward storage and green-hydrogen equipment. Longi Green Energy Technology Co. has become a top-five electrolyzer producer and took control of Canadian storage-system maker PotisEdge in November 2025; JinkoSolar expects its battery division to double in 2026. Investor attention has shifted in parallel: on Canadian Solar’s November 13, 2025 earnings call, “storage” was mentioned 62 times versus 33 for “solar”; four days later, JinkoSolar showed 57 versus 21.

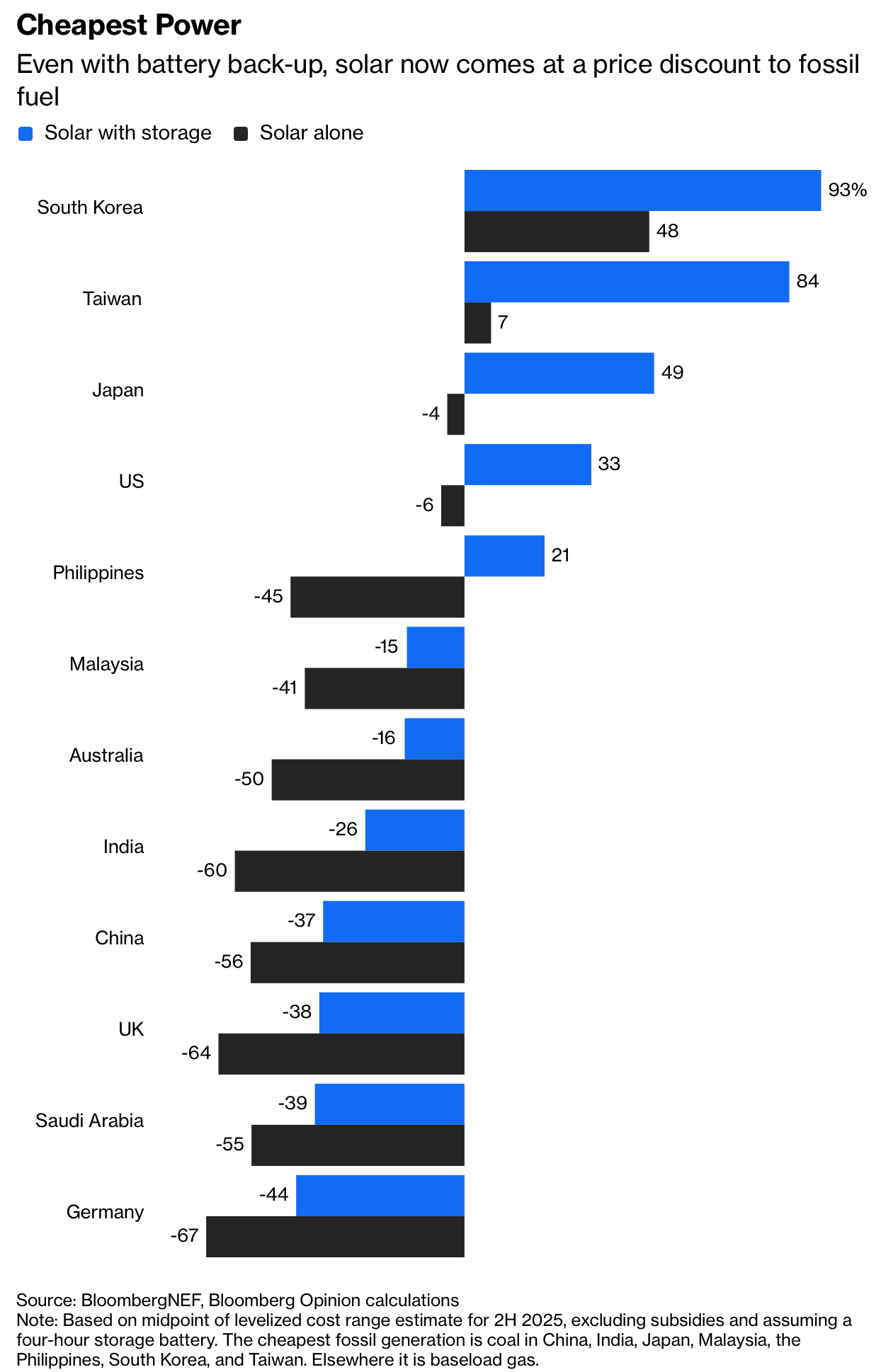

The transition is driven by market pricing mechanics, not branding. Solar panels generate at the same midday hours, creating temporary oversupply that can push wholesale prices low or below zero. In South Australia during the December 2025 quarter, daylight wholesale prices were below zero 88% of the time. The highest-value periods are morning and evening peaks, when panel output is weaker. For project developers, simply adding panel capacity now faces shrinking returns; by contrast, batteries, hydrogen systems, and trackers can shift cheap midday electricity into higher-price windows. With battery costs down 26% over the past year, solar-plus-storage increasingly undercuts the cheapest fossil generation while delivering more dispatchable and stable supply.

The piece frames this as a classic maturity cycle, not a retreat. As photovoltaics already supply more than one-fifth of generation in markets including Australia, Chile, the Netherlands, and Spain, many more markets are likely to follow in the next few years, and utility-scale solar will more often be sold bundled with batteries, electrolyzers, or other backup. Geopolitics reinforces this advantage: unlike LNG supply chains disrupted by conflict, renewable assets can keep operating for decades once deployed. History shows both outcomes: IBM and Texas Instruments moved into higher-value niches after core products commoditized and reached nominal market-cap peaks within the past six months, while Blackberry, HP, Intel, and Nokia show the downside if business-model innovation lags technology innovation.