希腊已成为更广泛海运争夺的缩影:COSCO控股的比雷埃夫斯每年处理超过400万个集装箱,美国支持的埃莱夫西纳项目距其仅30公里,且在其北方500公里处塞萨洛尼基出现中俄资本入场,亚历山大罗波利斯附近美军与北约的后勤基地更强化了安全属性。普华永道预计到2035年,全球港口基础设施支出将增长超过三分之一,达到每年900亿美元,而目前海运已承载全球约80%的贸易量,因此航道可靠性已成为商业与地缘战略并重的变量。

中国企业在至少129个海外港口拥有经营或财务份额,并在全球已至少投资800亿美元建设港口,其中超过三分之一位于马六甲、霍尔木兹和苏伊士等关键海峡周边,使其在关键地缘节点上具有高控制权。研究显示,签署码头运营合同时,与中国的总贸易额会增加超过20%,但若中国企业在某港口全部接管码头,该国对外出口却可能下滑19%,这种“增加贸易—抑制第三方贸易”的双向结果与优先调度与议价权集中相符。

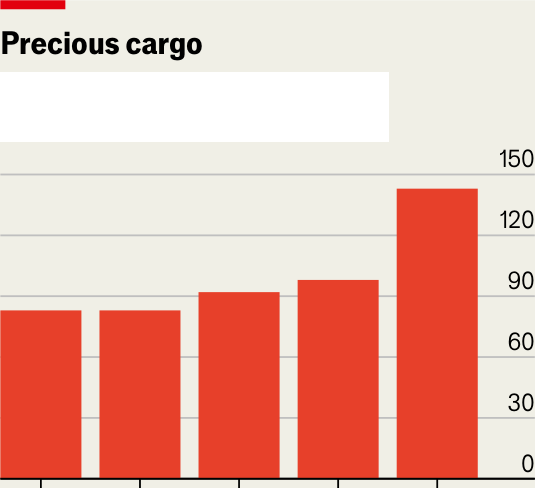

面对地缘压力,非中国企业自2021年起已宣布约1400亿美元并购,包括Stonepeak与CMA CGM成立的100亿美元联合企业United Ports、APM Terminals与Eurogate在北海的10亿欧元扩建、沙特4.5亿美元的吉达港交易以及新加坡200亿美元自动化港口计划;印度则宣布港口建设将持续到2047年。与此同时,美国对巴拿马运河的监管压力正在升温,运河承载美国约40%的货运、约占全球海运贸易5%或2700亿美元。

Greece is now a concentrated example of the global port battle: COSCO-majority Piraeus moves more than 4 million containers a year, U.S.-backed development at Elefsina is only 30 km away, Chinese-Russian capital has moved into Thessaloniki 500 km farther north, and a U.S./NATO logistics footprint at Alexandroupolis reinforces the security dimension. PwC projects annual port infrastructure spending to rise by more than one-third to $90 billion by 2035, while sea transport already carries about 80% of global trade by volume, making route reliability both a commercial and strategic variable.

Chinese firms have operating or financial stakes in at least 129 foreign ports and have invested at least $80 billion in port construction, with more than one-third of these assets near chokepoints such as Malacca, Hormuz, and Suez. After terminal operation contracts are signed, total trade with China rises by over 20%, yet in countries where Chinese operators control all terminals at one port, exports to the rest of the world have been observed to fall 19%, reflecting combined effects of operational priority and leverage.

Non-Chinese firms have responded hard: since 2021 they announced about $140 billion in maritime acquisitions, including a $10 billion Stonepeak–CMA CGM United Ports JV, a €1 billion APM Terminals–Eurogate expansion in the North Sea, Saudi Arabia’s $450 million Jeddah port deal, and Singapore’s $20 billion automated hub, while India’s port expansion is projected through 2047 and U.S. pressure around the Panama Canal has risen, where the canal carries 40% of U.S. cargo, about 5% of global sea trade, or $270 billion. Operational stress is increasing as Hormuz rerouting and higher energy volumes through Panama raise delays and freight rates, and the post-hutchison/Hutchison-legacy Panama episode (including a $23 billion MSC-linked terminal transfer) shows how geopolitics can rapidly reprice port access, even as structural indicators like Chinese shares above 70% of ship-to-shore cranes, 95% of containers, and software reach across at least 24 countries and 86 ports signal that margins above 40% are unlikely to hold under duplication-heavy competition.

Source: A storm in every port

Subtitle: PIRAEUS AND DUBAI Countries are rushing to build ports in a contest to secure maritime trade routes

Dateline: The Economist May 2nd 2026