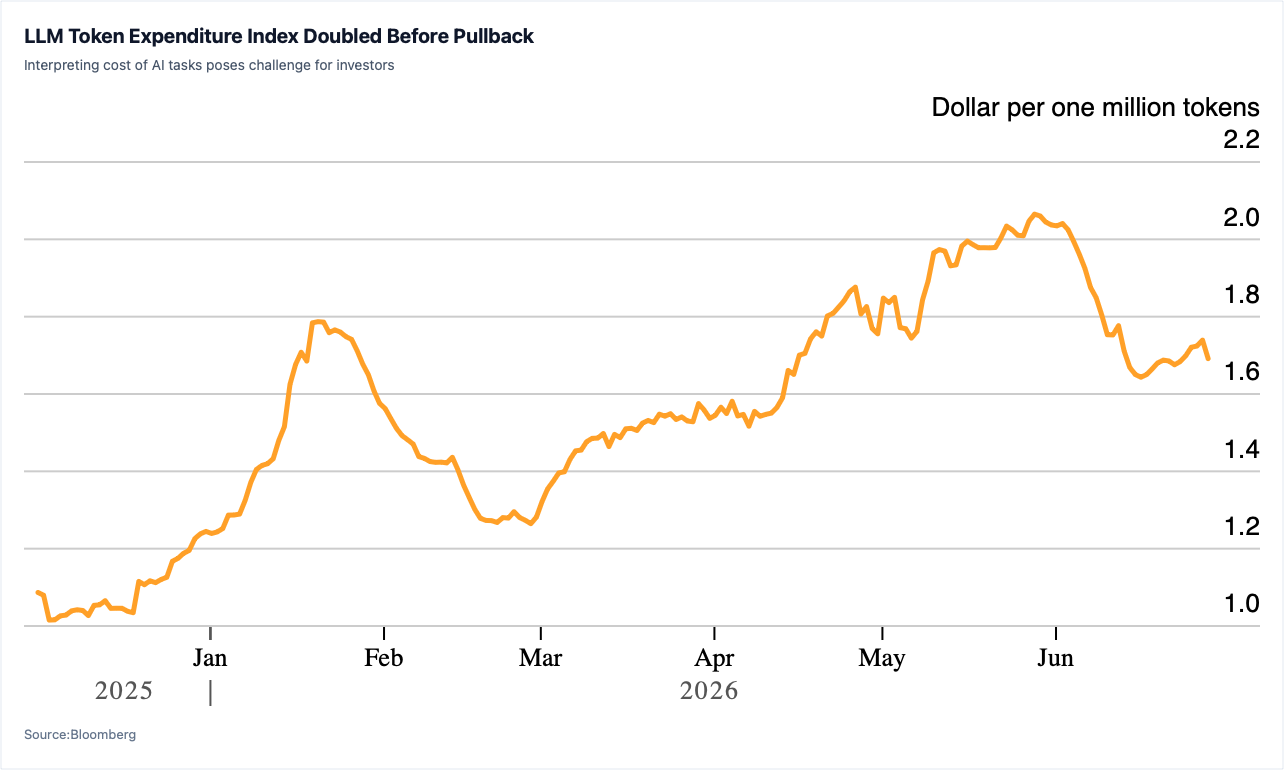

对股票投资者而言,该指数的走软可能预示AI公司正在失去定价能力,客户的成本敏感度日益上升。资深投资人Louis Navellier指出,越来越多AI用户因高昂成本而不得不限制使用量,OpenAI推迟IPO至明年也被视为盈利能力仍存问题的讯号。安联研究报告显示,AI投资与销售之间的增长差距接近46%,甚至超过2001年电信泡沫时期32%的差距,令空方更加警惕。

不过多头阵营仍有支撑:指数的下行趋势已暂时停歇,顶级GPU和高频宽记忆体在2026年前已售罄,硬体需求并未崩塌。此外,欧盟AI法案和美国政府对前沿模型的监管限制虽未直接压低价格,却增加了顶级平台的合规负担,可能促使企业将工作负载转向更便宜的模型。文章结论认为,该代币指数具有双面含义:若近期企稳持续,则廉价代币将继续扩大市场、资本支出合理;若客户支付意愿见顶且监管压力推动需求下移,则最昂贵的交易环节将首先承压。

The Silicon Data LLM Token Expenditure Index, which measures what users pay for AI tokens, has dropped nearly 20% from its May peak after almost doubling since its December inception. While token prices have plunged over 90% since 2023, total spending has roughly doubled year-over-year, suggesting that cheaper tokens have expanded the addressable market. However, a decline in the index can signal multiple scenarios—falling list prices, a demand shift toward cheaper models, or a genuine weakening in buyers' willingness to pay—each carrying distinct implications for investors.

For equity investors, the softening index may warn that AI companies are losing pricing power amid rising cost sensitivity. Veteran investor Louis Navellier noted growing reports of users restraining AI usage due to high costs, and OpenAI's rumored IPO delay is seen as evidence of persistent profitability challenges. Allianz Research found a nearly 46% growth gap between AI investment and sales, exceeding the 32% divergence seen during the 2001 telecom bust, fueling bearish concerns that the AI trade's foundation could crack.

Still, the bull case remains alive: the index's downward trend has paused, top-end GPUs and high-bandwidth memory are sold out through 2026, and hardware demand points to a mix shift toward inference-optimized parts rather than an outright glut. Meanwhile, regulatory developments—including the EU AI Act and US restrictions on frontier model deployment—add compliance burdens to leading platforms, potentially nudging workloads toward cheaper alternatives. The article concludes that the token index cuts both ways: if the recent flattening holds, capex remains justified and the bull case stays intact; but if customers' willingness to pay has peaked as regulatory headwinds push demand down-market, the most expensive segment of the AI trade will be the first to falter.