在可量化的敞口上,软体被描述为私募信贷中、由私募股权支持企业所构成的最大单一产业:在中型市场 CLOs 中,依 S&P Global Ratings 的分析,软体占投资组合的 19%;而 KBRA 以其自有的借款人分类方法,横跨中型市场 CLOs、BDCs 与以经常性收入作担保的债券,发现按价值计算有 22% 的可比债务由软体公司所欠。本月的法说会上,KKR、Apollo 等管理人表示过去几年已透过出售降低软体曝险;另一些如 Ares 则称其软体占比远低于业界平均。放款人也强调较低的 loan-to-value 结构:Blue Owl 的 Marc Lipschultz 表示其软体贷款平均约为借款人企业价值的 30%,意味著放款人只有在总业务价值被摧毁超过 70% 时才会承受重大损失;作者反驳说,在估值处于高峰的发行批次(peak-vintage valuations)以企业价值作锚定可能有风险,而且软体借款人的信用指标较弱,S&P 指出其在中型市场借款人中具有最高的中位数杠杆比率与最低的利息保障倍数,即使两者近年都略有改善。

前瞻性的压力点在于再融资与流动性,而不只是按市价计量(mark-to-market)的价值:UBS 策略师估计,约 1-fifth 受到 AI 破坏影响的私募股权支持公司将需要在 2028 为债务再融资,而近期 BDC 提款潮显示取得新资金可能更困难,推升利息成本并挤压股权缓冲与违约风险。有些投资者认为这波抛售已过头,并引用报导称 Carlyle、BlackRock 等正在买入折价的软体债务以提高 CLO 获利;作者则指出,像是债权人对债权人(creditor-on-creditor)的争议等额外风险,更常见于规模更大、放款人较多的交易,而非中型市场的私募债务。文中将潜在外溢效应界定为具宏观相关性,因为杠杆贷款与私募信贷市场合计约有 $3.5 trillion 的债务;在最糟的尾端情境下,UBS 估计全系统损失可能达到 $275 billion,足以普遍收紧融资,并可能削弱与 AI 热潮本身相关的资本支出与投资计划。

The column argues that while AI fears have already jolted stock and bond markets, loan and private-credit investors may be behind in assessing where software-related debt is exposed, partly because industry classifications are inconsistent and can hide software businesses inside categories like retail or food. That makes it harder for holders of loan-focused mutual funds, collateralized loan obligations (CLOs), business-development companies (BDCs), and private-credit funds to identify which credits face higher default or refinancing risk as AI reshapes software economics. Within BDCs alone, Bloomberg News found at least 250 loans to software firms worth more than $9 billion that were categorized as other industries by 1 or more vehicles, illustrating how labeling noise can mask concentration even when underlying business risk is unchanged.

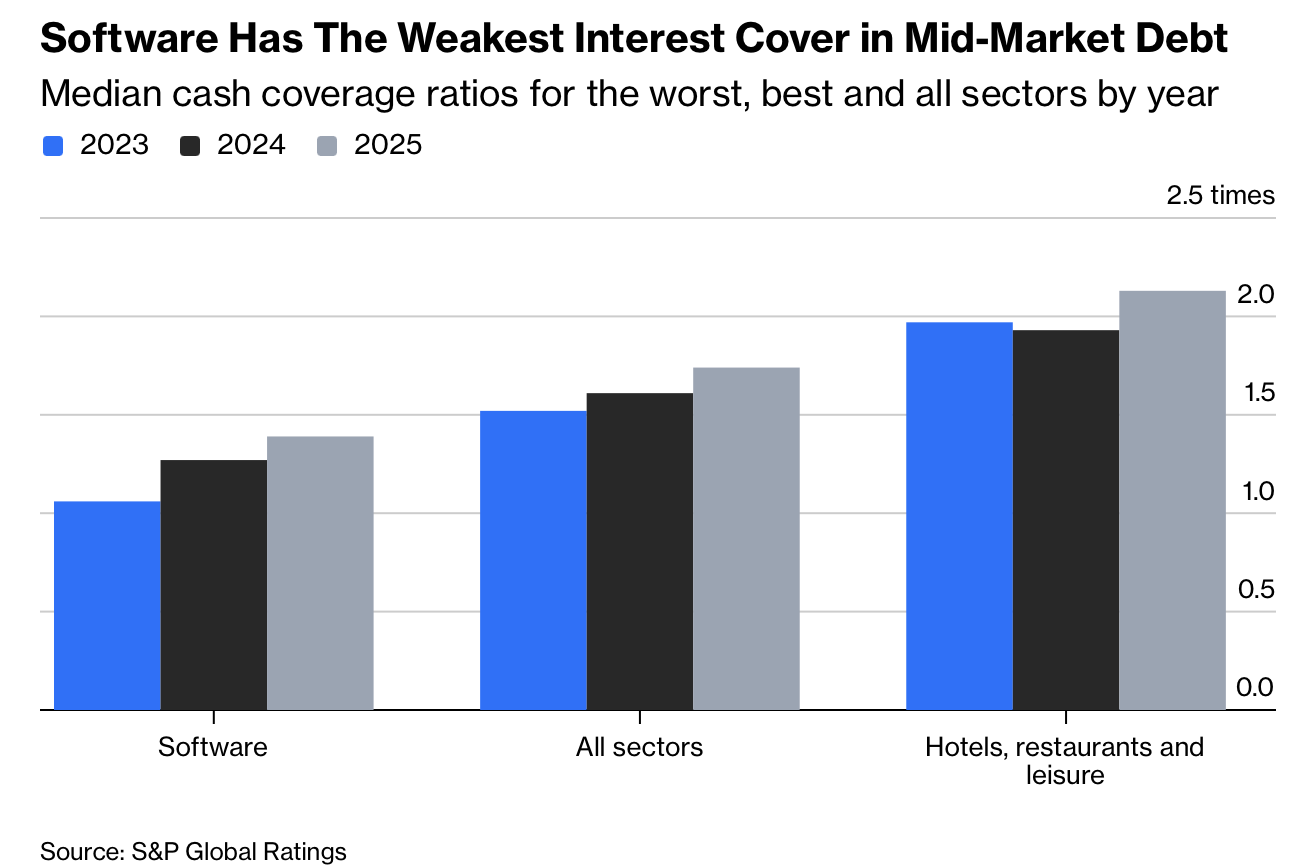

On measured exposure, software is described as the largest single industry among private-equity-backed businesses across private credit: in mid-market CLOs, software is 19% of portfolios by S&P Global Ratings’ analysis, while KBRA found 22% of comparable debt by value was owed by software firms using its own borrower categorization across mid-market CLOs, BDCs, and recurring-revenue-backed bonds. Managers such as KKR and Apollo said on earnings calls this month they have reduced software exposure via sales over the past couple of years, while others like Ares said their software share is well below the industry average. Lenders also point to low loan-to-value structures: Blue Owl’s Marc Lipschultz said its software loans averaged 30% of borrowers’ enterprise values, implying lenders would take major losses only if more than 70% of total business value were destroyed; the author counters that enterprise-value anchoring can be risky at peak-vintage valuations and that software borrowers show weaker credit metrics, with S&P indicating the highest median leverage ratios and lowest interest coverage ratios among mid-market borrowers, even if both have improved slightly in recent years.

The forward-looking stress point is refinancing and liquidity rather than just mark-to-market value: UBS strategists estimate about 1-fifth of private-equity-backed companies exposed to AI disruption will need to refinance debt in 2028, and recent BDC withdrawal waves suggest fresh funding could be harder to secure, raising interest costs and pressuring equity cushions and default risk. Some investors argue the selloff has gone too far, citing reports that Carlyle, BlackRock, and others are buying discounted software debt to boost CLO profits, while the author notes additional risks like creditor-on-creditor disputes are more typical in larger multi-lender deals than in mid-market private debt. The potential spillover is framed as macro-relevant because leveraged loan and private credit markets total about $3.5 trillion of debt; in a worst-case tail scenario, UBS estimates systemwide losses could reach $275 billion, large enough to tighten financing broadly and potentially undercut capital spending and investment plans tied to the AI boom itself.