该情境显示AI行业呈现“高速增长与高投入不匹配”的结构。用户规模迅速扩大:ChatGPT周活跃用户超过9亿,Google Gemini月活跃用户从2025年5月的4亿增长至超过7.5亿,增长约87.5%。收入亦快速上升,OpenAI年化收入从约60亿美元增至超过200亿美元(约3.3倍),Anthropic预计接近200亿美元。但商业模式仍以订阅为主,价格从每月数百美元到潜在数千美元不等,尚未形成稳定盈利路径。

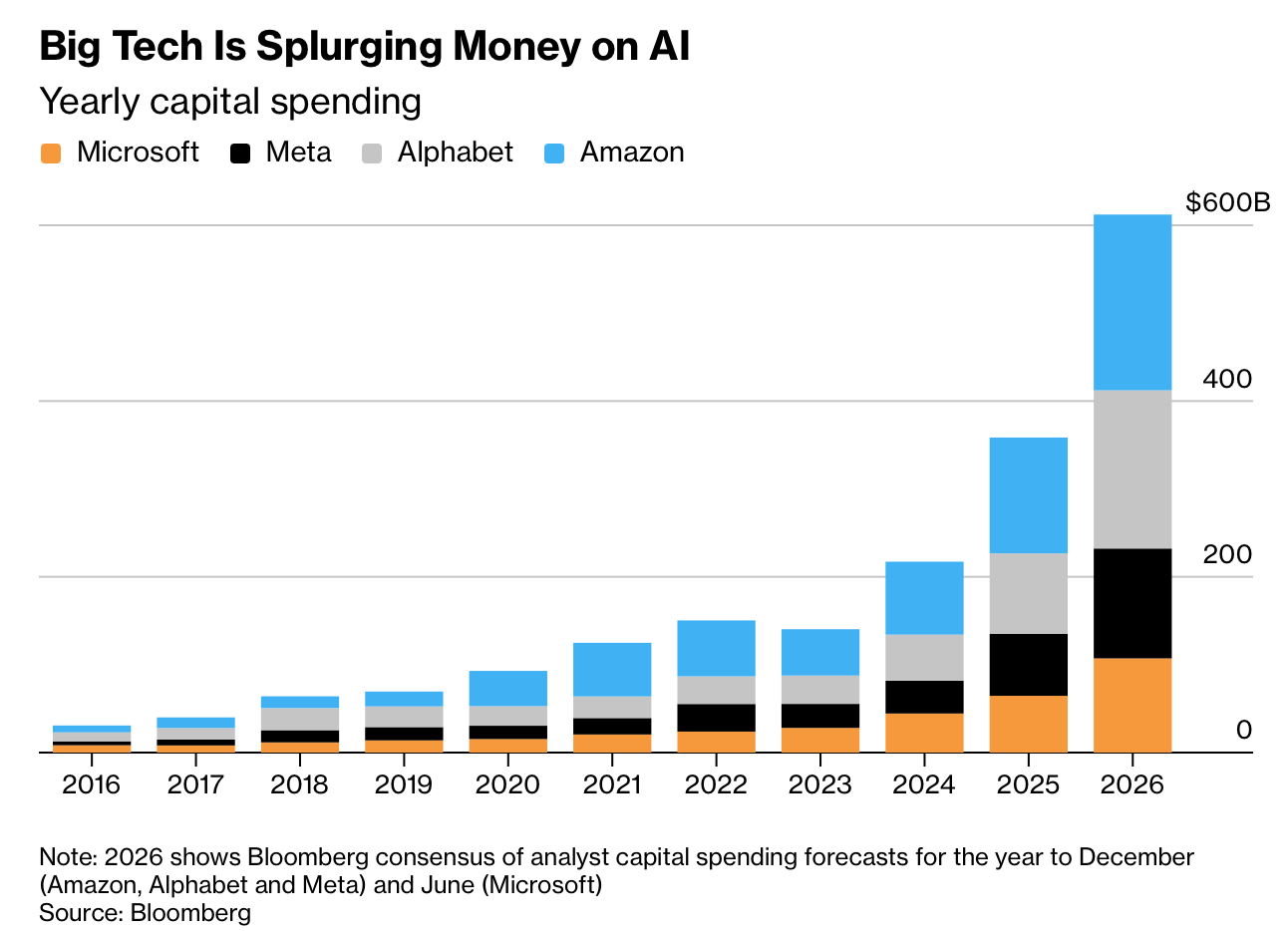

成本端呈指数级扩张。四大科技公司2026年资本支出预计约6500亿美元,OpenAI未来投入超过1.4万亿美元,Anthropic计划投入500亿美元。行业整体到2030年需约2万亿美元年收入以覆盖计算成本,但预计将短缺8000亿美元,缺口约40%。同时债务融资加速,超大规模云厂商借款从2025年的1650亿美元升至2026年的4000亿美元,增长约2.4倍,反映资金压力显著上升。

生产率与回报存在不确定性。研究显示AI对客服生产率提升约15%,但对开发者任务反而延长19%,结果分化明显;个别公司报告高达200%效率提升,但缺乏广泛验证。劳动力影响有限,仅2%企业因实际AI应用裁员。与此同时,中国开源模型下载占比达约17%,首次超过美国,削弱定价能力。整体呈现“用户与收入快速增长(>2×)+资本支出更快扩张(万亿美元级)+生产率与盈利不确定”的不平衡格局。

The context shows a structural mismatch in the AI industry between rapid growth and massive spending. User bases are expanding quickly: ChatGPT has over 900 million weekly users, while Google Gemini grew from 400 million monthly users in May 2025 to over 750 million, an increase of about 87.5%. Revenue is also rising fast, with OpenAI’s annualized revenue increasing from about $6 billion to over $20 billion (roughly 3.3×), and Anthropic approaching $20 billion. However, the business model remains subscription-based, ranging from hundreds to potentially thousands of dollars per month, without a clearly proven path to profitability.

Costs are expanding at an exponential scale. Four major tech firms forecast about $650 billion in capital expenditures for 2026, while OpenAI plans to spend over $1.4 trillion and Anthropic about $50 billion. Industry estimates suggest $2 trillion in annual revenue will be needed by 2030 to cover computing demand, but projections fall short by $800 billion, a gap of about 40%. Debt financing is also rising sharply, with hyperscaler borrowing increasing from $165 billion in 2025 to $400 billion in 2026, about 2.4× growth, indicating mounting financial pressure.

Productivity gains and returns remain uncertain. Studies show about a 15% productivity increase for customer service workers, but a 19% slowdown for software developers, indicating mixed outcomes; some firms report gains up to 200%, though not broadly validated. Labor market impact is limited, with only 2% of firms cutting jobs due to actual AI use. Meanwhile, Chinese open-source models account for about 17% of downloads, surpassing US models and potentially limiting pricing power. The overall pattern reflects imbalance: rapid user and revenue growth (>2×), faster capital expansion (trillion-scale), and uncertain productivity and profitability outcomes.