數據顯示,中國的電動汽車專用生產線及混合工廠的總產能約為2500萬輛,而今年國內電動汽車銷量預計將達到1700萬至2000萬輛,產能利用率處於非常健康的水平。事實上,小米、蔚來等新興電動車廠甚至面臨供不應求的局面,這說明電動車領域並不存在普遍的產能過剩。

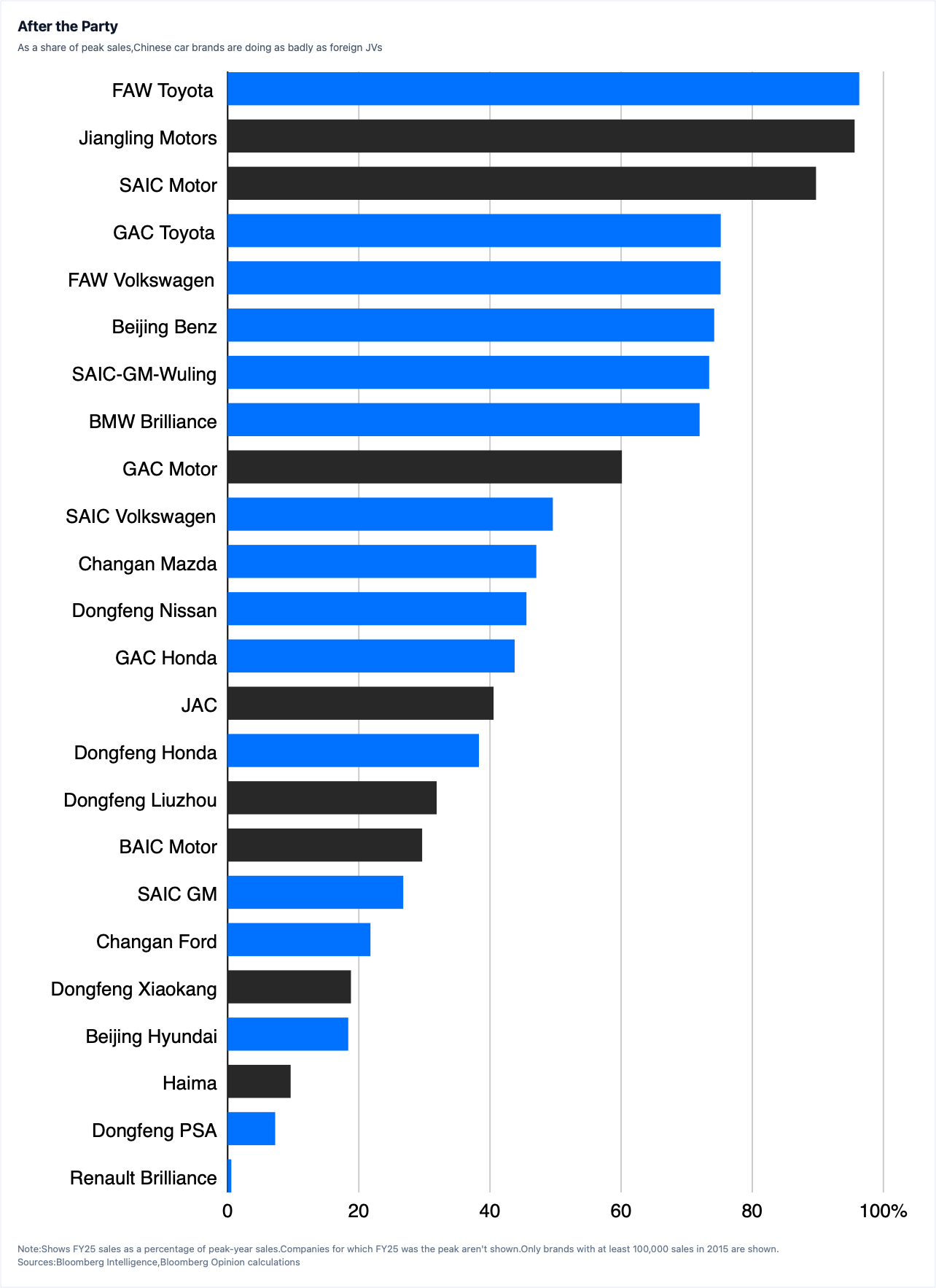

真正的產能過剩存在於轉型緩慢的傳統國有企業及中外合資企業的燃油車工廠。隨著消費者停止購買汽油車,這些工廠的產能利用率暴跌,這實質上是新技術取代舊技術的正常資本主義「創造性破壞」過程,而非國家產業政策所致。

Many Western analysts and policymakers accuse China of having severe overcapacity in electric vehicles and exporting excess production to solve domestic market saturation. However, this view ignores the dramatic shift in China's automotive market structure, where consumer demand for conventional gasoline cars has plunged while demand for EVs has grown rapidly.

Data shows that China's total EV capacity from dedicated and mixed lines is around 25 million vehicles, while domestic EV sales this year are expected to reach 17 to 20 million, keeping utilization rates at a very healthy level. In fact, emerging EV makers like Xiaomi and Nio are struggling to meet high demand, indicating that there is no general overcapacity in the EV sector. (Key numbers: 2500, 1700, 2000)

The real overcapacity lies in the gasoline vehicle factories of traditional state-owned enterprises and foreign joint ventures that were slow to transition to EVs. As consumers stop buying gasoline cars, the utilization rates of these plants have plummeted, reflecting a typical process of creative destruction where new technology displaces the old.