从历史上看,Fed 只有在名目成长率超过 8% 时才少数几次降息,而其中多数发生在 1970s;那是一个与容易导致通膨的政策结果相关的年代,投资人不希望重演。同时,美元走弱也有量化依据:DXY 指数在过去 1 年约下跌 10%,在货币已经贬值的情况下进一步降息,可能意味著即便 Treasury 反复重申强势美元意图,政策仍转向「弱美元」体制。作者质疑「AI 驱动的生产力提升将足以带来通缩、从而支撑美元」的乐观说法,转而指出去全球化以及贸易与劳动限制带来的通膨压力,并提到像 NFIB 小型企业定价意图调查等领先指标仍在上行。

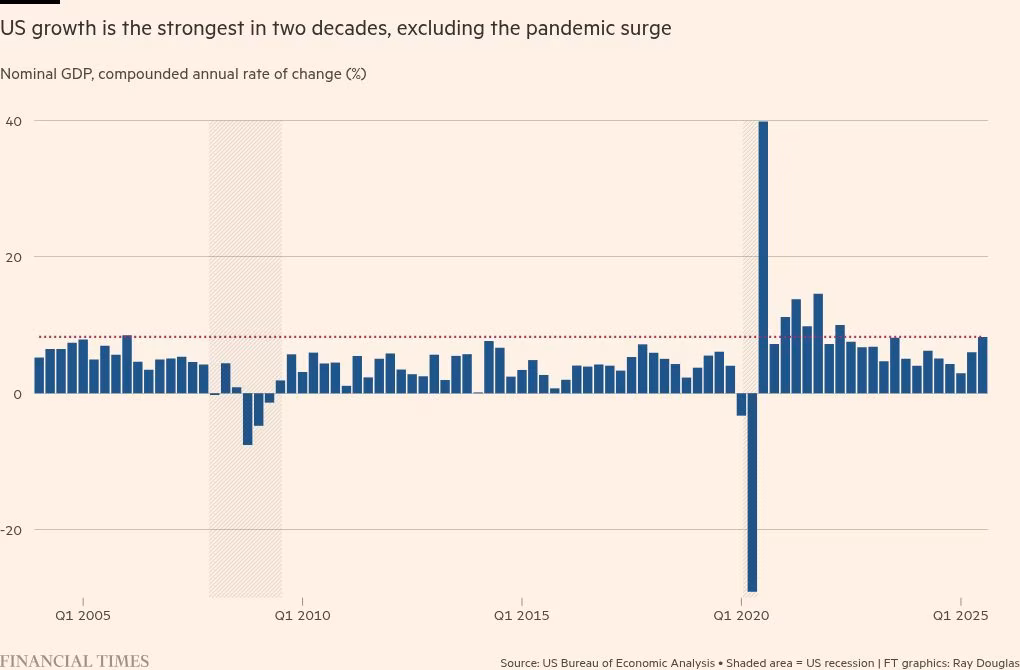

"文章主张,2026 年美国联准会可能在经济看似健康且美元走弱的情况下仍选择降息,这种组合作者称在现代美国经济史上未曾出现,因而可视为真正的「未曾涉足领域」。文中以名目指标来界定经济强劲:最新公布季度的名目 GDP 成长率高于 8%,被形容为除疫情后时期外 20 年来最强;而根据亚特兰大联准会 GDP 估计的短期追踪,加上 1 年期抗通膨公债(TIPS)讯号,显示未来 1-2 个季度名目成长可能仍高于 7%。",

The article argues that in 2026 the US Federal Reserve may enter truly “uncharted territory” by cutting interest rates even though the economy looks healthy and the US dollar is weakening, a combination the author says has not occurred in modern US economic history. The economy’s strength is framed in nominal terms: the latest reported quarter’s nominal GDP growth was above 8%, described as the strongest in 20 years outside the post-pandemic period, and near-term tracking based on Atlanta Fed GDP estimates plus 1-year inflation-protected Treasury signals suggests nominal growth above 7% over the next 1-2 quarters.

Historically, the Fed has cut rates only a handful of times when nominal growth exceeded 8%, and most of those episodes occurred in the 1970s, a decade associated with inflation-prone policy outcomes that investors would not want repeated. At the same time, the dollar’s weakness is quantified: the DXY index is down roughly 10% over the past year, and cutting rates into an already-depreciating currency could imply a shift toward a “weak dollar” regime even as the Treasury reiterates strong-dollar intentions. The author challenges optimistic claims that AI-driven productivity will be disinflationary enough to support the dollar, pointing instead to inflationary pressures from de-globalisation and trade and labor restrictions, and notes that leading indicators like NFIB small-business pricing-intentions surveys are still moving upward.

Given US investors have not faced a persistently weak dollar in nearly 2 decades, the piece recommends positioning for outcomes where inflation is higher than consensus and long-term rates rise, which would likely hurt longer-duration assets and longer-duration equities. As portfolio responses, it highlights international equities and “shorter duration” (more dividend-oriented) stocks, emphasizing relative metrics: US investors are significantly underweight non-US equities versus the roughly 40% non-US weight in the MSCI All-Country World Index; non-US equities (MSCI ACWI ex US) are cited as having about double the dividend yield versus US equities (2.5% vs 1.2%) and cheaper valuations (18x trailing earnings vs 26x for US). It also argues dividends are a practical duration proxy and a historically powerful compounding mechanism, noting that over the past 25 years the S&P Dividend Aristocrat Index’s total return has been roughly neck-and-neck with the Nasdaq but with considerably less volatility, implying non-US and dividend-paying stocks may be better suited if the 2026 policy mix proves unprecedented.