水泥作为现代文明中仅次于水的高使用量材料,年使用量约为250亿至300亿吨,约为煤炭开采量的三倍,同时贡献了全球约8%的年度碳排放。然而,在经历数十年增长后,全球水泥消费已触顶。2021年全球产量峰值为44亿吨,当前趋势显示即便印度、东南亚和非洲继续工业化,也可能无法重返该水平。中国占全球产量近一半,但其水泥繁荣期已结束,且下行仍在持续。

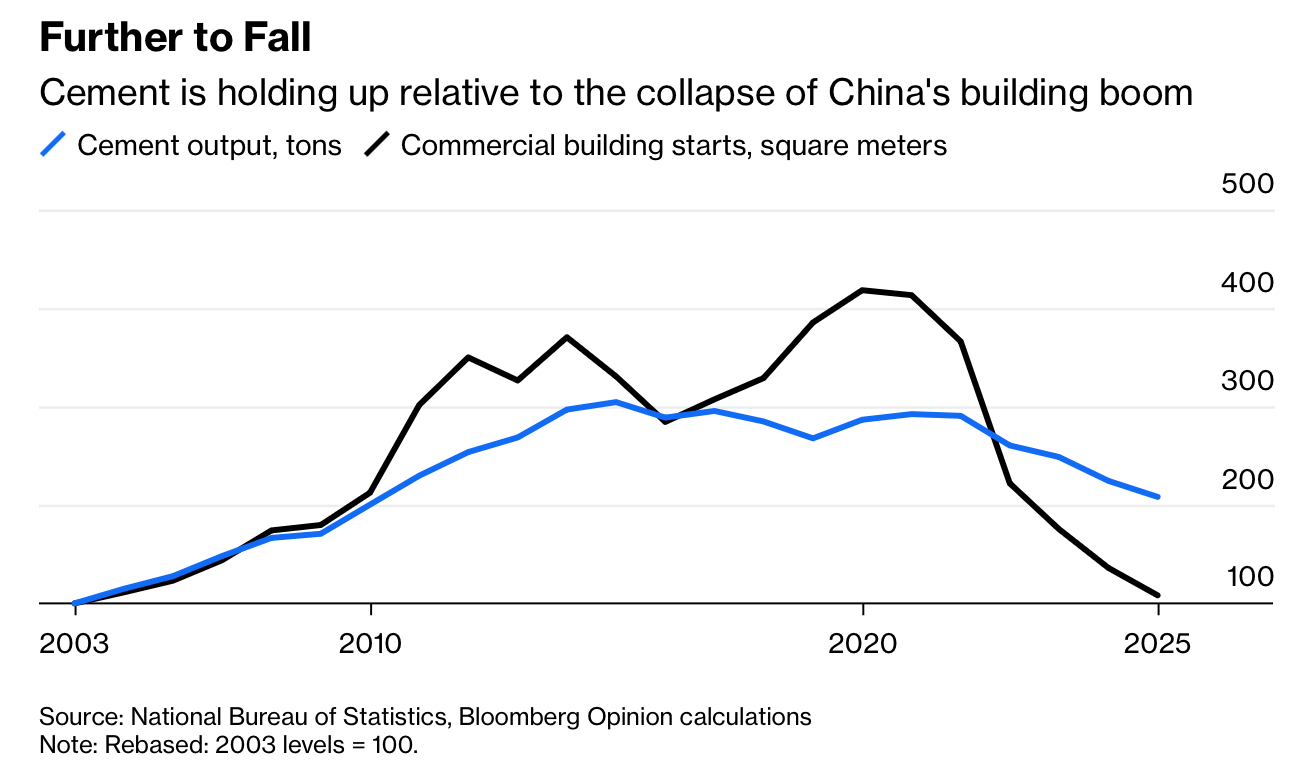

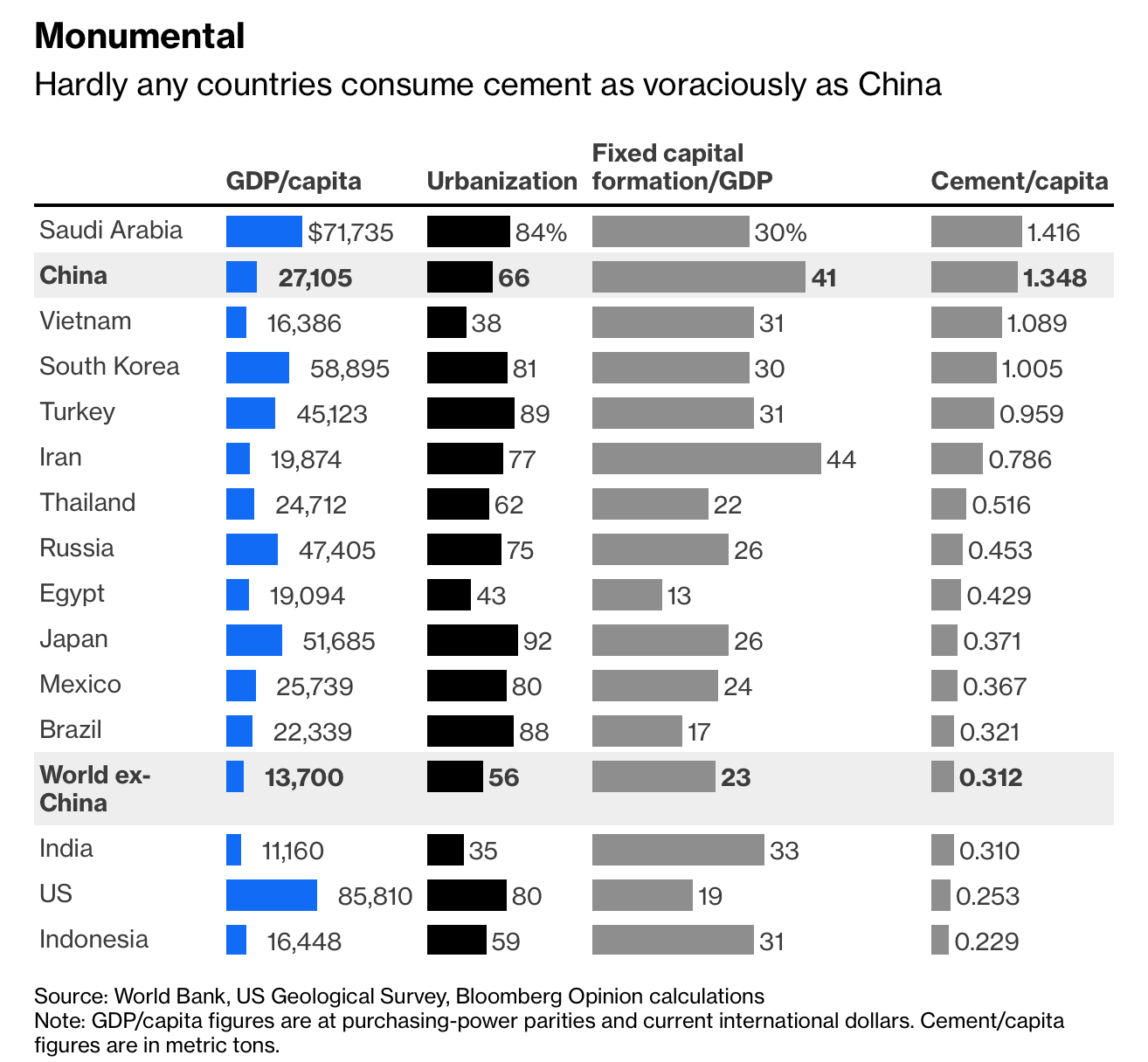

中国水泥产量自2020年以来已下滑近30%,预计2026年将连续第六年下降。价格处于近十年低位,产能超过实际需求的两倍,而新开工商业建筑面积这一先行指标已降至2003年以来最低,但当前产量仍是当年的近两倍。水泥需求在国家完成工业化后会快速下坠:高收入国家的人均水泥排放量与低收入国家相近。中国在2014年峰值时人均消费达1.8吨,美国仅0.25吨;当前中国仍约1.2吨,是全球平均的四倍,仅低于沙特等少数国家。

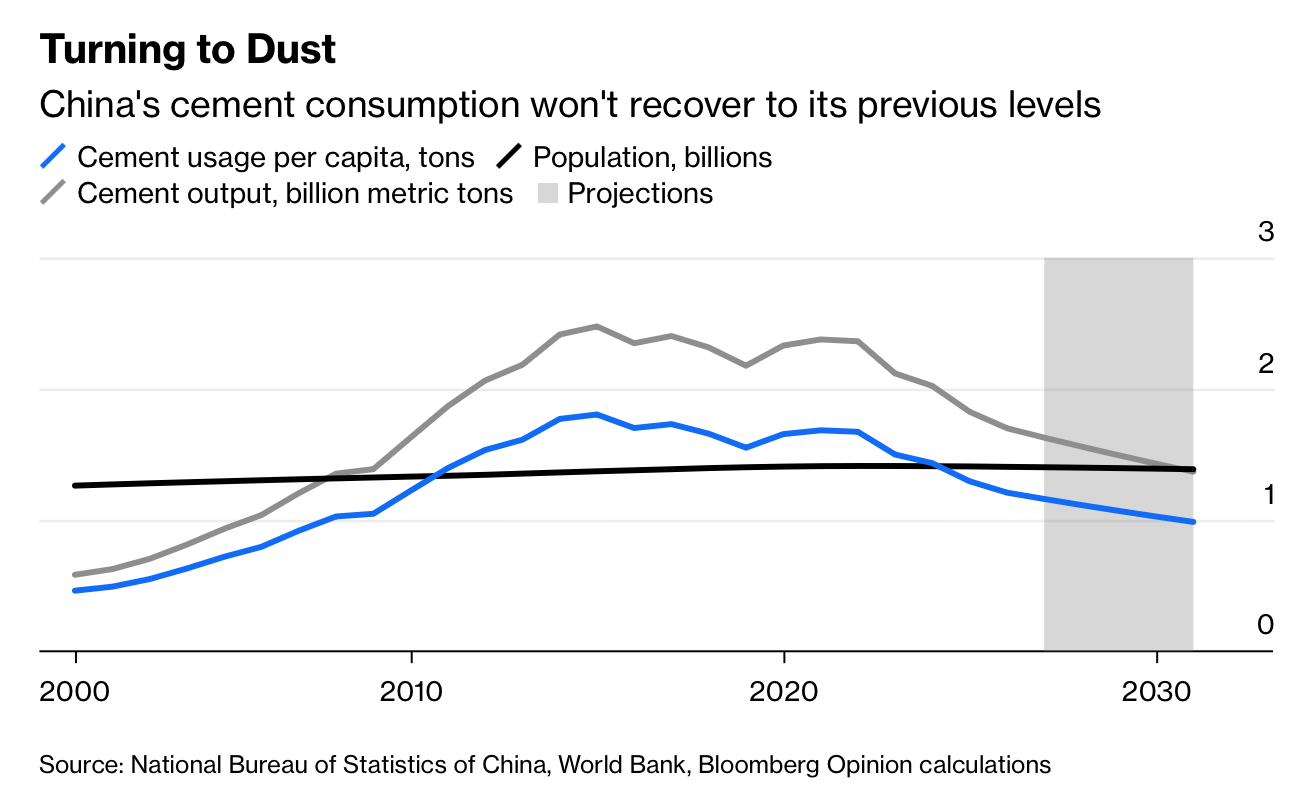

即便温和回落也将产生巨大影响。若到2030年人均消费年降幅从过去五年的6%放缓至4%,中国总产量仍将减少约20%,即3.5亿吨,其他国家难以弥补这一缺口。水泥每吨排放约0.8吨二氧化碳,技术改造仅能减排5%至10%,碳捕集难以规模化。因而,需求下行成为最现实的减排路径。随着经济结构演进,水泥的高峰已过,其长期收缩几乎不可逆。

Concrete is the most widely used material after water, with roughly 25 to 30 billion metric tons poured each year—about three times global coal output—and cement alone accounts for around 8% of annual global emissions. After decades of growth, global cement consumption has now hit a ceiling. Production peaked at 4.4 billion tons in 2021, and current trends suggest it may never return to that level, even as India, Southeast Asia, and Africa continue to industrialize. China still produces nearly half of global cement, but its long boom is definitively over.

China’s output has already fallen almost 30% since 2020 and is expected to decline for a sixth consecutive year in 2026. Prices are near decade lows, capacity exceeds demand by more than twofold, and newly started commercial floor space—a key leading indicator—has dropped to its lowest level since 2003, despite production being nearly double that year’s level. Cement demand collapses after industrialization: per-capita use in rich countries mirrors that in poorer ones. China consumed 1.8 tons per person at its 2014 peak versus 0.25 tons in the US; today it remains around 1.2 tons, four times the global average.

Even modest declines will have outsized effects. If per-capita use falls 4% annually through 2030, output would still drop about 20%, or 350 million tons, a shortfall other countries cannot offset. Each ton of cement emits about 0.8 tons of CO₂, while technical fixes offer only 5% to 10% reductions and carbon capture remains marginal. Falling demand is therefore the most viable path to decarbonization. As economies mature, cement’s best years are behind it, with a long-term contraction now unavoidable.