文中证据显示,亚马逊的领先在实质上是由云端运算规模带动,而非纯粹来自零售主导。亚马逊扣除云端后的营收为 5880 亿美元,虽仍极为庞大,但比沃尔玛总营收低逾 1000 亿美元,这意味著云端及其相邻服务对整体排名具有决定性。同时,商务领域的竞争态势仍然活跃:沃尔玛持续将数千家门市最佳化为在地化履约节点,而亚马逊则进一步扩张至美国乡村市场。根据 EMarketer,沃尔玛今年在美国的电商销售预计成长速度将近亚马逊的 3 倍,显示即使亚马逊整体营收较高,沃尔玛仍可能取得市占增益。

核心含意是,股权市场关注重点集中在人工智慧资本支出的效率,而非营收规模领先;分析师优先检视的是基础设施支出增速是否超过云端营收增速。这与亚马逊 2007 到 2015 年较早的一轮周期相呼应,当时 Jeff Bezos 在全国仓储扩建期间,因重投资策略与微薄利润率而遭受批评。在 CEO Andy Jassy 领导下,同样的资本配置争论已由仓储转向资料中心:投资人依然对回报时点、回收风险与利润率压力高度敏感,因此亚马逊在营收上加冕超越沃尔玛,除非支出能转化为可持续的现金流扩张,否则对估值影响有限。

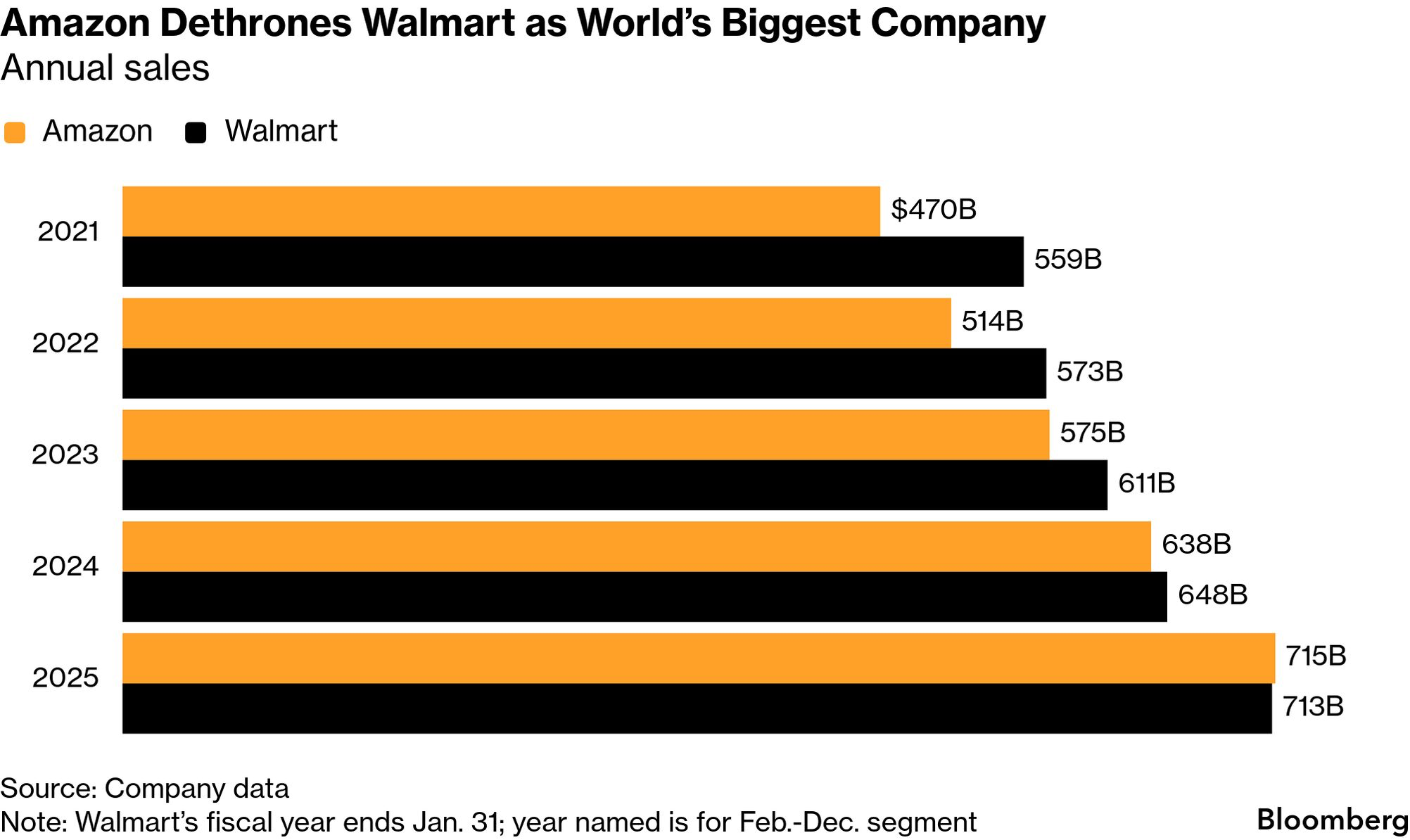

Amazon.com Inc. unsettled investors by announcing plans to spend $200 billion in 2026 on data centers, chips, and related AI infrastructure, extending a broader capital-spending wave that also includes Alphabet, Meta Platforms, and Microsoft. Against that backdrop, a major operating milestone received less attention: Amazon overtook Walmart Inc. as the world’s largest company by revenue, with $717 billion in calendar-year 2025 sales versus Walmart’s $713 billion in its fiscal year ended January 31. The gap is narrow at $4 billion, but symbolically significant after Walmart held the top revenue position for more than 10 years.

The evidence in the article shows that Amazon’s lead is driven materially by cloud computing scale rather than pure retail dominance. Amazon’s revenue excluding cloud was $588 billion, which is still enormous but more than $100 billion below Walmart’s total, implying cloud and adjacent services are decisive in the overall ranking. At the same time, competitive dynamics in commerce remain active: Walmart continues optimizing thousands of stores as localized fulfillment nodes, while Amazon is expanding further into rural U.S. markets. According to EMarketer, Walmart’s U.S. e-commerce sales are expected to grow nearly 3 times as fast as Amazon’s this year, indicating potential share gains despite Amazon’s higher consolidated revenue.

The core implication is that equity attention is concentrated on AI capex efficiency rather than top-line leadership, with analysts prioritizing whether infrastructure spending growth outpaces cloud revenue growth. This mirrors an earlier Amazon cycle from 2007 to 2015, when Jeff Bezos faced criticism for reinvestment-heavy strategy and thin margins during national warehouse build-out. Under CEO Andy Jassy, the same capital-allocation debate has shifted from warehouses to data centers: investors remain sensitive to return timing, payback risk, and margin pressure, so Amazon’s revenue crown over Walmart carries limited valuation impact unless spending translates into durable cash-flow expansion.