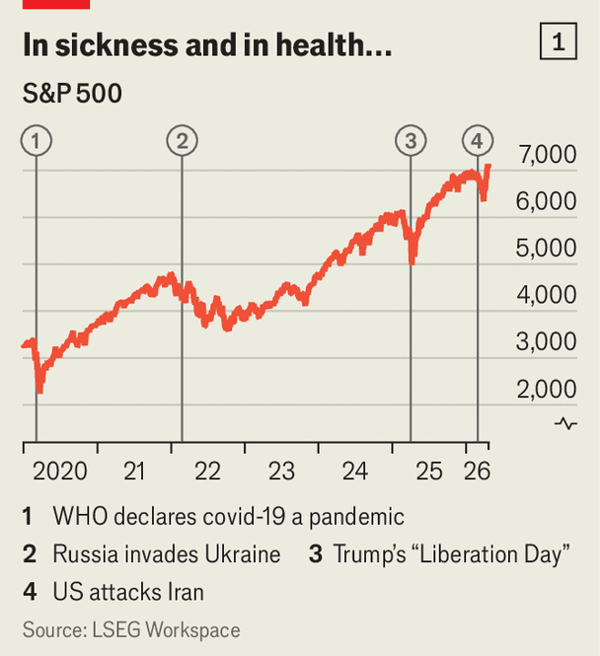

过去七周,美国市场波动主要受伊朗战争叙事及特朗普社交媒体言论驱动:标普500在4月17日因美国与伊朗同意重启霍尔木兹海峡通航而创新高,4月20日协议破裂后回落。 但企业盈利数据表现强劲:FactSet估计标普500第一季度总体盈利同比增长19%,分析师预计未来12个月盈利同比将高出24%,这一水平在近20年只在2007-09衰退后复苏与2020年疫情复苏后出现,并高于2017年末特朗普首次政府下税改法案后那轮盈利高峰。

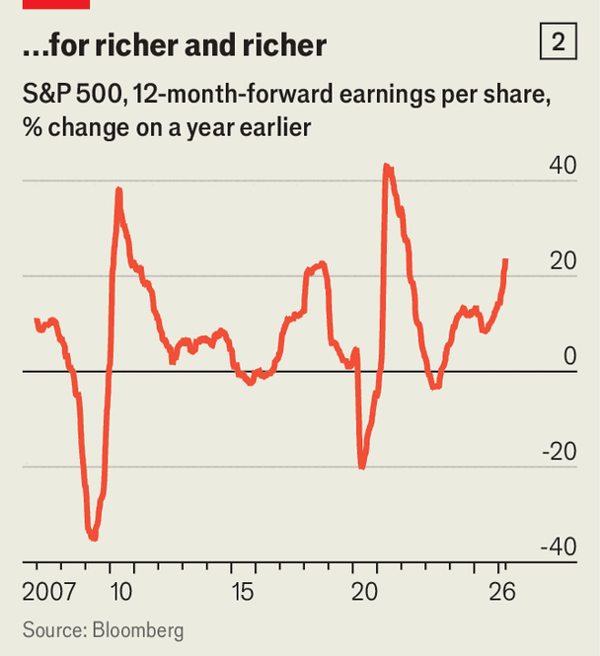

Q1盈利增量最大的五家公司中有四家来自AI受益板块:Nvidia预计2026年盈利再增长近80%,Broadcom也几乎同样强;Micron与SanDisk分别有望增长约7倍与16倍。 剔除“七大科技巨头”后,剩余493家公司2026年盈利预期仍上涨16%;即便剔除全部信息技术股,指数利润预期仍有17%,约与含科技股的日本TOPIX持平,约为欧洲STOXX 600的两倍、香港恒生指数的五倍。

第一季度前3个月,金融业收入同比增速超过10%,利润同比接近20%,材料行业为5%和逾20%;采掘和冶金行业利润更预计接近90%,消费品与医疗保健也普遍超预期,预计4月30日披露财报的Eli Lilly将成为除Nvidia和Micron之外的第三大单项盈利贡献者。 但若海湾战争延长并推高能源价格、特朗普再发动关税攻势、再次威胁罢免联储主席或干预11月中期选举,市场信心可能受损;但当前仍是美国企业韧性与创新驱动超过衰退叙事占优。

Over the past seven weeks, U.S. market moves were driven more by narratives—particularly the Iran war story and Trump’s social-media signals—than hard policy change: the S&P 500 hit an all-time high on April 17 after a deal to reopen the Strait of Hormuz, then fell on April 20 when that deal collapsed. Yet the hard data is unusually supportive, with FactSet estimating S&P 500 aggregate earnings up 19% year-on-year in Q1 and analysts projecting 24% higher earnings over the next 12 months than a year ago, a level last seen in only two prior 20-year episodes (the 2007-09 and 2020 recoveries) and stronger than the post-2017 Tax Cuts and Jobs Act surge.

AI is now the central driver: four of the top five contributors to Q1 earnings growth are AI beneficiaries, with Nvidia forecast to rise nearly 80% in 2026, Broadcom nearly as strong, and Micron and Sandisk expected to jump about seven-fold and 16-fold. Even excluding the “Magnificent Seven,” FactSet expects the remaining 493 S&P 500 firms to grow earnings 16% in 2026, and excluding all information-technology companies still leaves index-wide profit growth at 17%, roughly equal to TOPIX including tech leaders, about twice STOXX 600, and about five times the Hang Seng.

Sector trends remain broad: in Q1, financials grew revenue by more than 10% and profits by nearly 20%, materials posted 5% and over 20%, while mining and metals were nearly 90% on profits, and even consumer goods and healthcare names exceeded expectations. Risk remains policy-dependent—if the Gulf war drags on with higher energy prices, if tariff escalation, a Powell dismissal bid, or election interference increases, confidence could weaken—but at present businesses and investors still see U.S. dynamism as outweighing decline narratives.

Source: American corporate profits keep shrugging off global tumult

Subtitle: Earnings expectations are through the roof

Dateline: 4月 23, 2026 03:39 上午 | New York