这种挤压被集中供应格局放大。Nvidia、AMD及其他主要供应商形成高进入门槛,台积电今年计划投入约560亿美元(约56十亿美元)仍不足以满足先进产能需求;因此Elon Musk考虑建造自有晶圆厂,估算低至550亿美元,高至1,190亿美元。美国与全球巨型买方对价格敏感度较低,但受冲击明显:Microsoft表示零组件成本新增250亿美元,全年资本支出提高至约1,900亿美元;Meta则把预测资本支出中位值上修100亿美元。记忆体供应链回报更高,SK Hynix、Samsung Electronics与Micron合计市值已超过2.8兆美元,SK Hynix最新季度营业利润率达72%,Samsung三个月内DRAM平均售价较前一季上涨超过90%。

半导体需求正重新塑造上游与下游决策。Hyperscaler与neocloud加码签订长期晶片合约,致使记忆体支出预计到2026年占其资本支出比重达30%,而2024年仅为8%;同时云端GPU租赁价格持续上涨。各公司因此加速多元化硬体:Alphabet TPU、Amazon Trainium、Microsoft Maia 200,以及Google TurboQuant与Arm节能架构,后者声称每吉瓦资料中心容量成本可降低约100亿美元。由于晶圆厂建置周期长且产业高度循环,消费电子供应仍吃紧:全球智慧手机销售今年预估下降约13%;再加上高耗电资料中心带动电价与贸易逆差压力,AI可能对通膨造成持续推升。

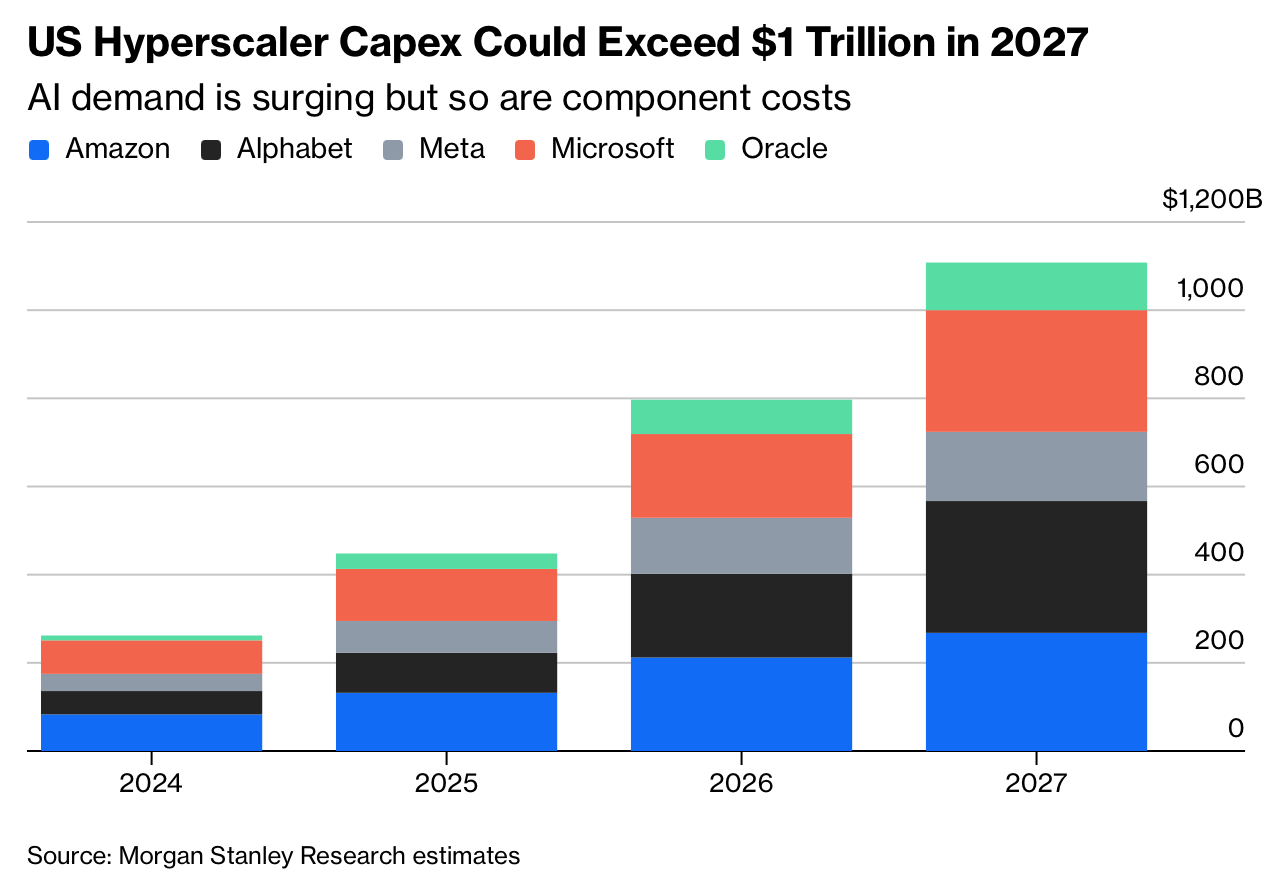

AI infrastructure costs keep climbing, with Morgan Stanley Research estimating U.S. hyperscaler capex could exceed US$1 trillion in 2027. Demand for ChatGPT, Claude, and related services is driving huge spending, while the component side has also become inflationary (“chipflation”), so prices for chips, memory, and related hardware are rising together. This has not only expanded datacenter builds but also strained supplies for conventional devices, pushing consumer hardware prices higher and making AI-related bottlenecks harder to ignore.

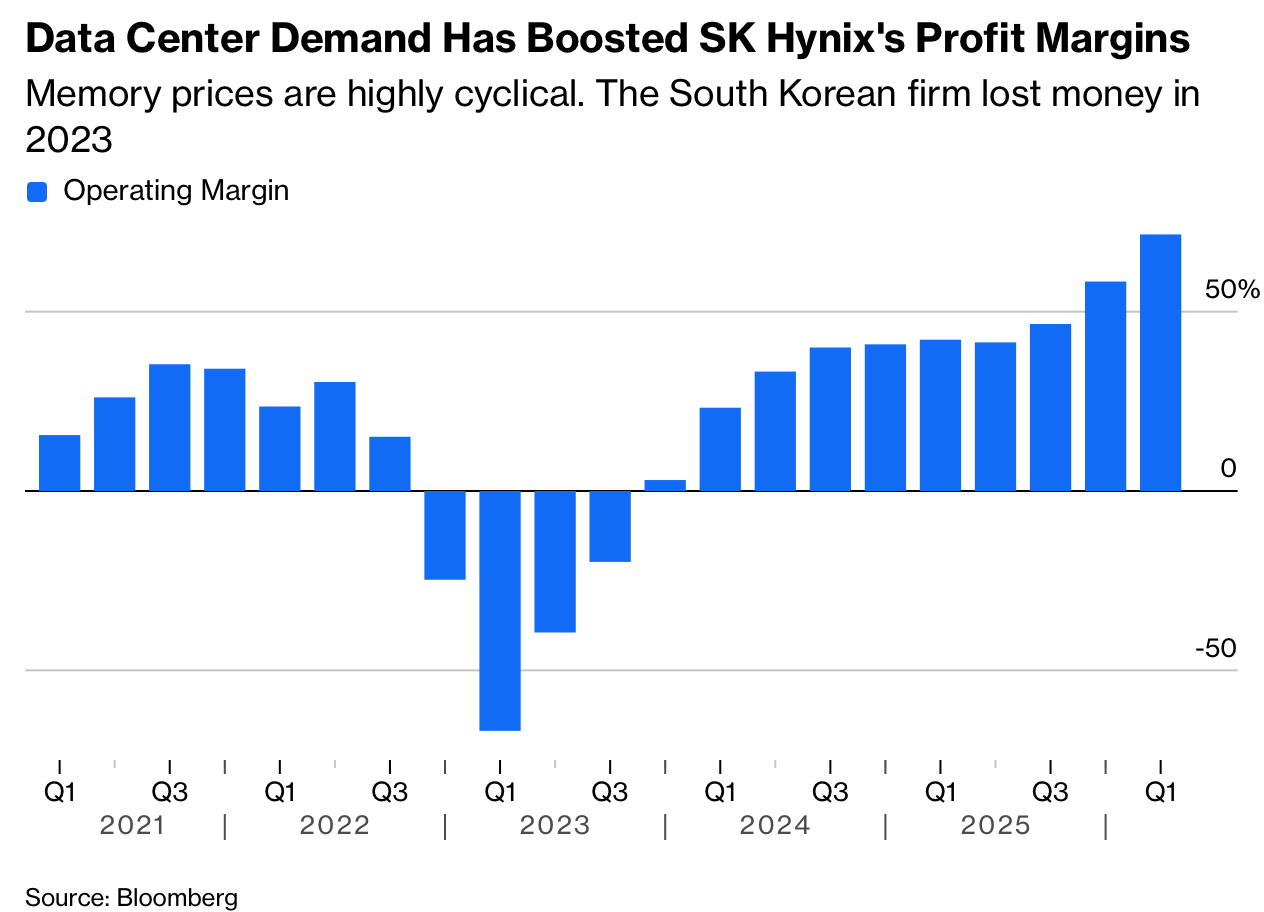

The squeeze is amplified by concentrated supply. Nvidia, AMD, and other leading suppliers hold high barriers to entry, and TSMC’s record US$56 billion annual capex is seen as insufficient for cutting-edge output, with Elon Musk considering a new in-house fab estimated at US$55 billion to US$119 billion. Hyperscaler buyers are price-insensitive but increasingly exposed: Microsoft said higher component costs add US$25 billion, raising full-year capex to about US$190 billion; Meta raised its forecast midpoint by US$10 billion. Memory suppliers benefit even more—SK Hynix, Samsung Electronics, and Micron are now worth over US$2.8 trillion combined, with SK Hynix operating margins at 72% and Samsung DRAM prices up over 90% quarter-over-quarter.

Semiconductor demand is still forcing a behavioral shift across the stack. Hyperscalers and neoclouds are locking into longer-term chip contracts and pushing memory spending to about 30% of capex in 2026 (from 8% in 2024), while rental rates for GPU capacity rise. Firms are responding by investing in alternatives—Alphabet TPUs, Amazon Trainium, Microsoft Maia 200, and newer compression/CPU designs—such as Google’s TurboQuant and Arm’s projected US$10 billion per gigawatt datacenter cost reduction. Yet slower supply-response cycles mean consumer-tech shortages persist; global smartphone sales are projected to drop around 13% this year, and electricity intensity plus trade imbalances could keep AI structurally inflationary if demand, and possibly interest-rate policy, fail to cool.