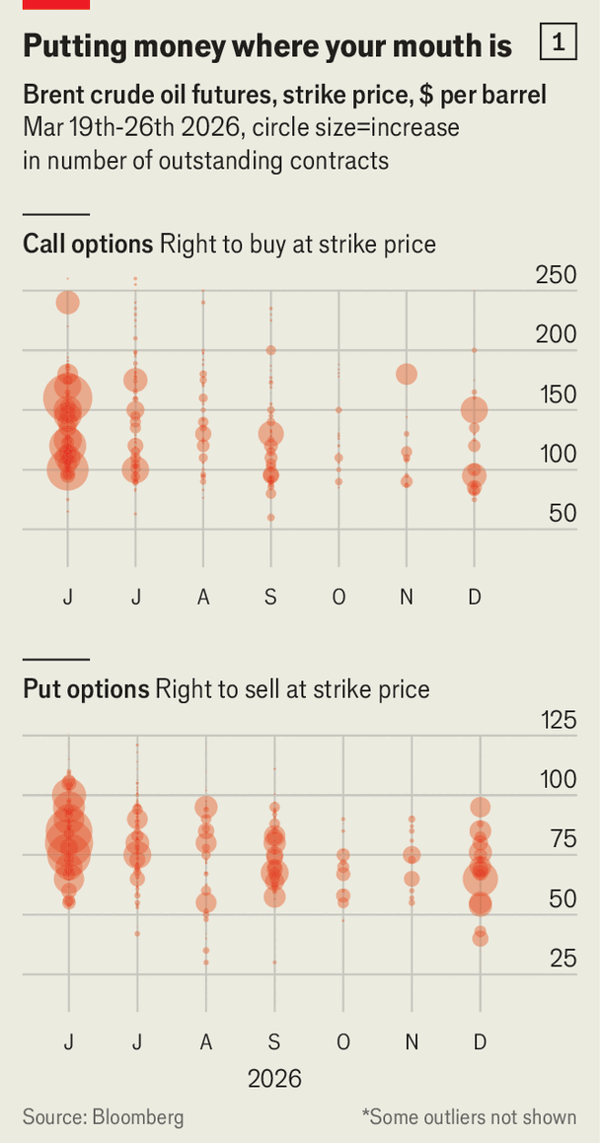

该更新版说明特朗普推迟了对伊朗基础设施的威胁性打击,文章刊出时第三次海湾战争已近第五周:霍尔木兹海峡每关闭一天,全球约五分之一的石油和液化天然气仍被困,布伦特油价升至每桶105美元,较开战前高45%,欧洲天然气价格高出65%。尽管如此,市场期权显示仍寄希望于短期修复,7月看跌期权在80美元附近集中,看涨期权分布更分散,意味着在计入运输滞后后,投资者预计到五月供应可回归正常。

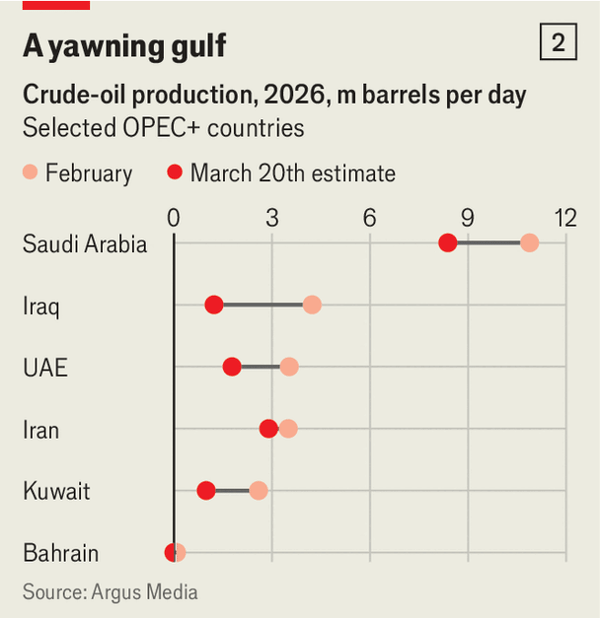

即便战争即刻结束,复苏仍缓慢,因为恢复需要三条链路同步:海湾产量、运输以及下游加工。海湾国家已减产1000万桶/日,约占全球产量的10%、其战前水平的40%,业内预计重启油井与初始处理设施需2到4周;卡塔尔鲁斯拉凡液化天然气基地自3月2日被迫停工,约2座14座装置受损,导致17%产能和全球供应的3%受影响,全面修复需3到5年,而短期复产需数周,并且设备脱水去湿与降温到-160°C等操作又可能再耗时最多7周。

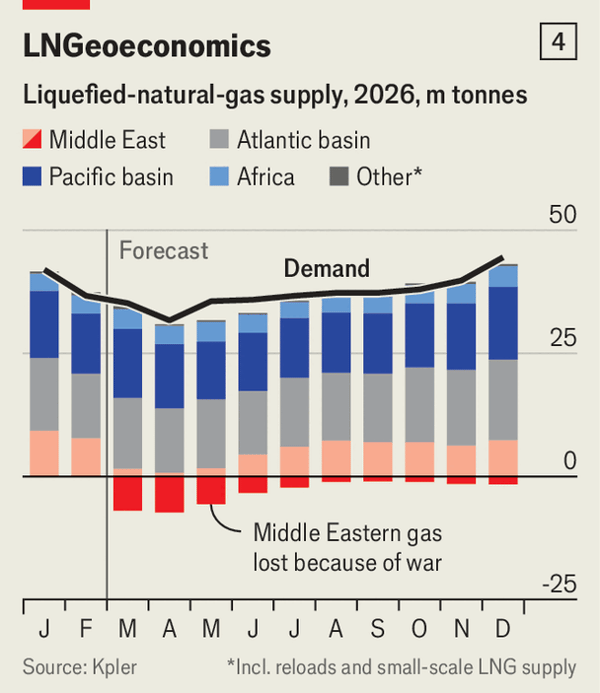

运输端的延迟仍在放大缺口:约有480艘油船滞留,许多船舶在海湾完成反向航行后仍需约90天才到位;许多已装载船舶可在约两周内清空等待,但由于战争险费率已从0.2%–0.4%上升到1%以上(最危险航线高达10%)、红海航线仅剩往年一半运输能力、以及港口与安全问题未完全消除,供给仍会继续错位。即便立即停火,市场也需约4个月才有“某种正常”迹象,预计全年计划油量被削减约3%,鲁斯拉凡每关闭一月全球天然气年供应几乎减少2%,即使卡塔尔立刻全量恢复,产量仍低于当年需求约4%;全球库存已接近历史下三分之一,且仍会下滑,可能引发抢购、LNG竞价争夺,并威胁冬季储备补充。

The updated version notes Trump’s delay of threatened strikes on Iran’s infrastructure as the third Gulf war enters its fifth week, and each day the Strait of Hormuz remains shut leaves around one-fifth of global oil and LNG stranded; Brent is at $105 per barrel, 45% above pre-conflict levels, while European gas prices are up 65%. Yet options positioning still signals a temporary view: July puts cluster near $80 a barrel and calls are more dispersed, implying markets expect normalization by May after transport lags are absorbed.

Even with an immediate ceasefire, normalization is not quick because recovery depends on three linked chains—Gulf production, shipping, and downstream processing. Gulf producers have already cut 10 million barrels a day (10% of global output and 40% of their pre-war level), with 2–4 weeks expected to restart wells and initial treatment, while Qatar’s Ras Laffan LNG complex, shut since March 2, lost 2 of 14 liquefaction trains (17% capacity, 3% global LNG), with full repair said to take 3–5 years and limited reactivation taking weeks plus up to 7 more weeks for purging and thermal cooldown work.

Shipping bottlenecks then add further delay: about 480 vessels are stranded, many need around 90 days to be in position, and even though loaded tankers may clear backlog in roughly two weeks, insurers have lifted war-risk rates from 0.2–0.4% to 1% or higher (10% on riskiest voyages), Red Sea tanker traffic is about half 2023 levels, and port/security frictions persist. The result is still roughly 4 months before markets show “some semblance of normality,” implying about a 3% cut to planned global oil output, nearly 2% of annual gas supply lost for each month Ras Laffan stays shut, and a 4% gap versus demand even with a full Qatar restart; stocks are already in the bottom third and could continue falling, raising the risk of panic buying, LNG bidding wars, and weak winter restocking.

Source: Even the best-case scenario for energy markets is disastrous

Subtitle: Whatever happens, high prices will outlive the Iran war

Dateline: 3月 26, 2026 04:46 上午