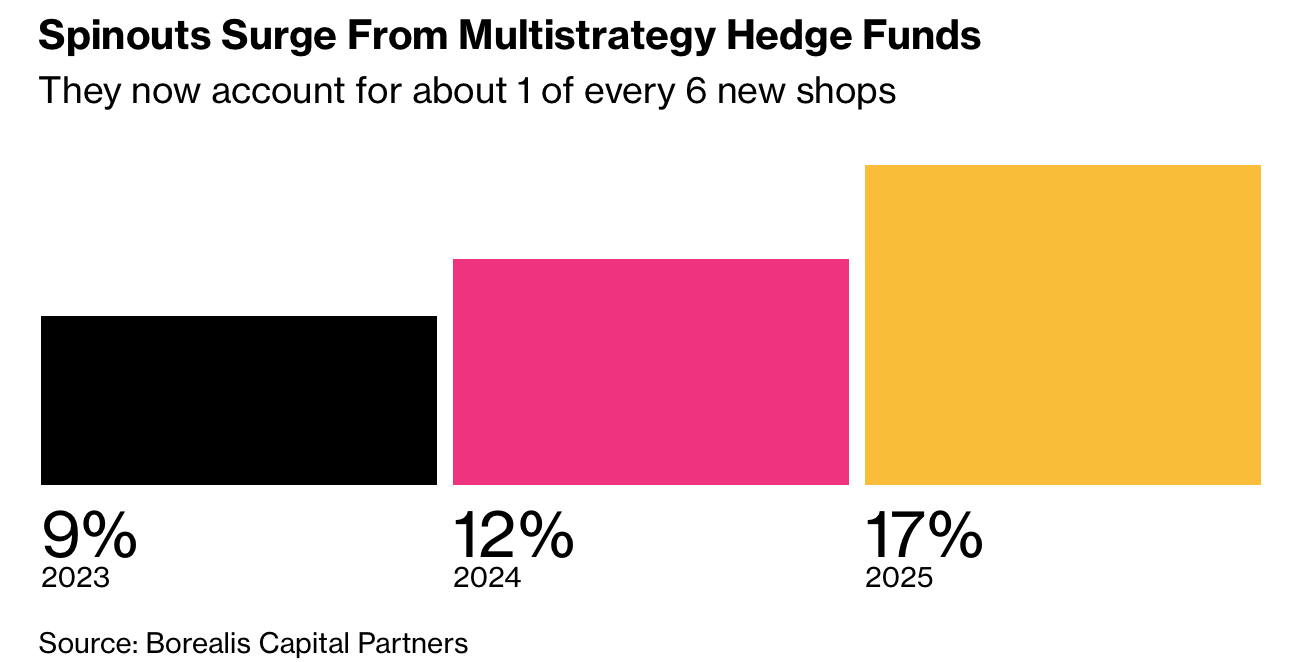

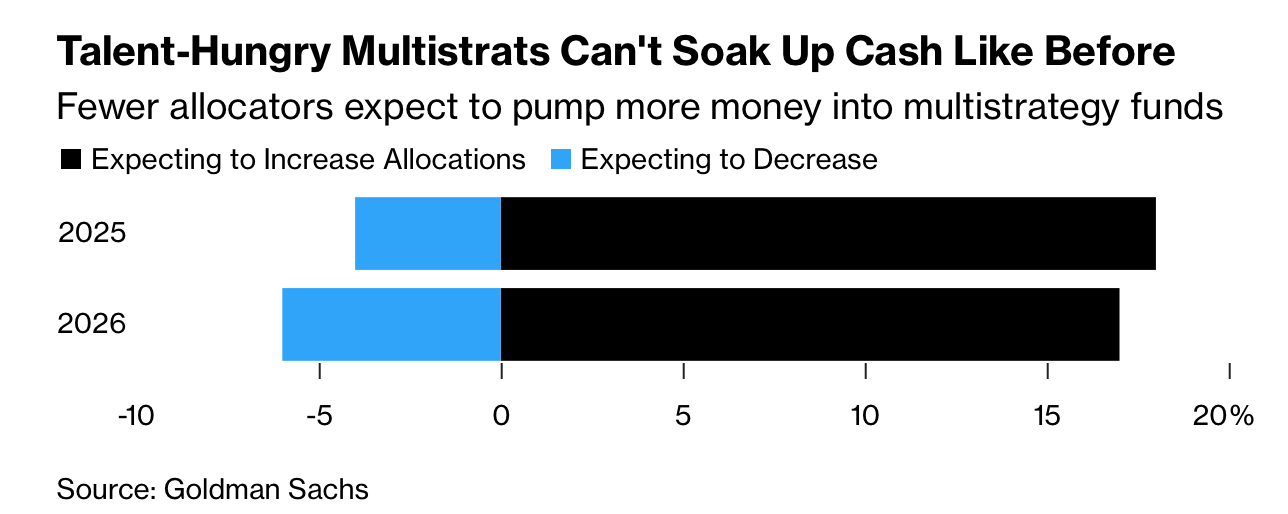

对冲基金行业出现结构性迁移:来自多策略平台的离职者占新基金创立的17%,较两年前几乎翻倍;行业经历16年来最佳收益与自2007年以来最大资金流入后,更多交易员选择独立。大型平台(合计管理超2300亿美元)因规模与人才约束放缓扩张,部分甚至停止募资并累计向投资者返还320亿美元利润,资金配置意愿也下降。

薪酬与绩效分布呈高度不均:顶级组合经理年收入可达5000万美元以上,而中位数约为200万美元;约10%的经理贡献大部分利润,约30%几乎不盈利或亏损,底部15%面临淘汰。尽管平台提供高达1.2亿美元的保留或挖角保障及百万美元签约奖金,但高压“pod”模式、短期止损约束与激烈内部竞争促使人才外流。

独立化路径依赖资本与风险权衡:新基金规模常见在2.45亿至2.5亿美元区间,也有300万美元级启动资金案例。多策略资金可快速放大规模(如3亿美元配置),但集中于少数出资方带来脆弱性,并可能涉及策略复制风险。结果是行业从集中化向分散化演变,交易员以放弃“数十亿美元火力”换取策略自主权与更长投资周期。

The hedge fund industry shows structural migration: departures from multistrategy platforms accounted for 17% of new fund launches, nearly double two years earlier; following the best returns in 16 years and the largest inflows since 2007, more traders are going independent. Large platforms (managing over $230 billion combined) face scale and talent constraints, slowing growth, with some halting fundraising and returning $32 billion to investors, while allocator appetite is declining.

Compensation and performance are highly skewed: top portfolio managers can earn $50 million+ annually, while the median is about $2 million; roughly 10% of managers generate most profits, about 30% produce little or negative returns, and the bottom 15% face termination. Despite offers including guarantees up to $120 million and multimillion-dollar signing bonuses, the high-pressure pod model, tight stop-loss rules, and intense internal competition drive talent exits.

Independence involves capital–risk trade-offs: new funds often launch with about $245 million to $250 million, though some start far smaller. Multistrategy allocations (e.g., $300 million) can rapidly scale firms but create fragility due to concentration among a few investors and potential strategy replication risks. The result is a shift from concentration toward fragmentation, as traders forgo access to billions in capital for autonomy and longer investment horizons.