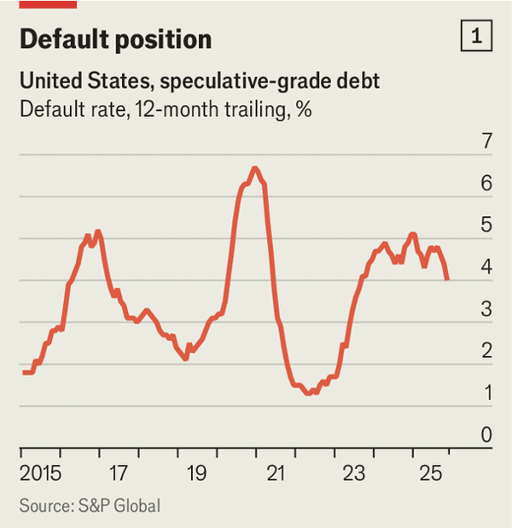

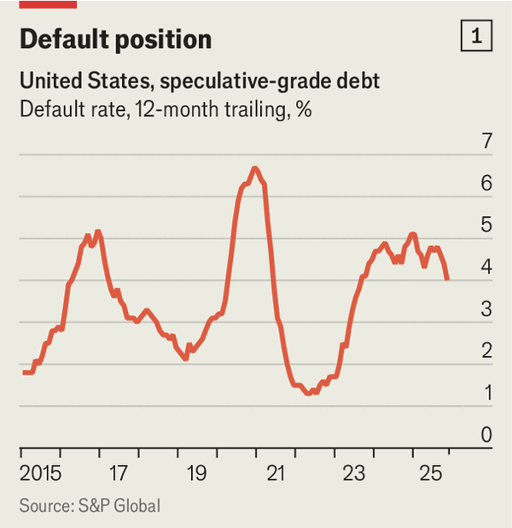

美国企业债务风险曾一度看似受控,但最新数据表明压力重新累积。2024 年美国投机级债务违约率曾升至 5%,到 2025 年有所回落;同期,美国非金融企业债务占 GDP 比例也从 2021 年上半年的 164% 降至 2025 年同期的 141%,显示企业在高利率环境下曾主动去杠杆。然而,2025 年第四季度 GDP 增速在 3 月 13 日被下修至仅 0.7%,低于投资者预期,宏观缓冲正在减弱。

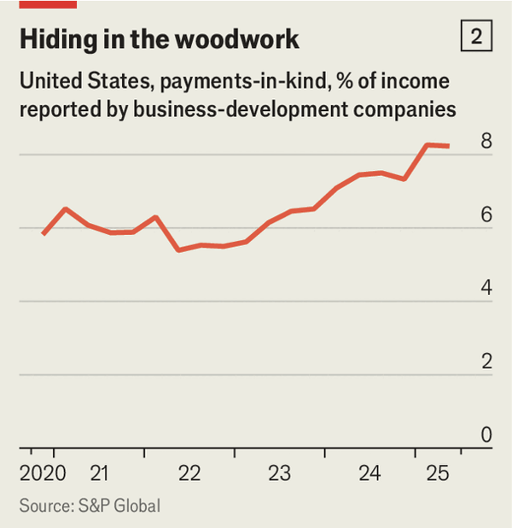

新的脆弱点集中在私人信贷市场及其表外延迟机制。表面上,私人信贷贷款的违约率仍低于 2%,但若把“实物支付利息”和“负债管理”等变相展期工具计入,真实违约率约升至 5%。上市私人信贷基金中,这类实物支付安排占收入的比例已从 5 年前的 5%–6% 升至 8%。这些操作能推迟破产显性化,却也意味着常规违约指标低估了实际恶化程度。

外部冲击正在放大这种隐患。中东战争推高能源成本,可能使美联储更不愿降息,而历史上的能源冲击往往伴随违约潮。与此同时,投资者担心人工智能会使更多企业商业模式过时。债务重组已越来越多地绕开公开破产:Goldman Sachs 研究显示,自 2023 年以来,约有 100 家欧洲私人公司通过债转股被移交给债权人。核心趋势是,企业信用问题正通过更隐蔽、更延后的方式扩散,而不是消失。

America’s corporate-debt risks had seemed briefly contained, but the latest figures suggest pressure is rebuilding. In 2024 the default rate on speculative-grade debt in America reached 5%, then fell in 2025; over roughly the same period, non-financial corporate debt as a share of GDP dropped from 164% in the first half of 2021 to 141% in the first half of 2025, showing deleveraging under higher rates. Yet the macro cushion is weakening: on March 13th, fourth-quarter 2025 GDP growth was revised down to just 0.7%, below investor expectations.

The new fragility is concentrated in private credit and its off-balance-sheet delay mechanisms. Headline default rates on private-credit loans remain below 2%, but once “payment in kind” and other liability-management extensions are counted, the true default rate rises to around 5%. For listed private-credit funds, payment-in-kind arrangements have grown from 5%-6% of income five years ago to 8% now. These manoeuvres can postpone visible bankruptcy, but they also mean standard default indicators understate underlying deterioration.

External shocks are amplifying the risk. The Middle East war has pushed up energy costs, potentially making the Federal Reserve less willing to cut rates, and past energy shocks have often been followed by waves of defaults. At the same time, investors fear artificial intelligence may obsolete more business models. Restructuring is increasingly happening outside public bankruptcy: a Goldman Sachs study says that since 2023 around 100 private European companies have been handed to lenders in debt-for-equity swaps. The core trend is that credit stress is spreading in more hidden and delayed forms, not disappearing.

{kind=link}