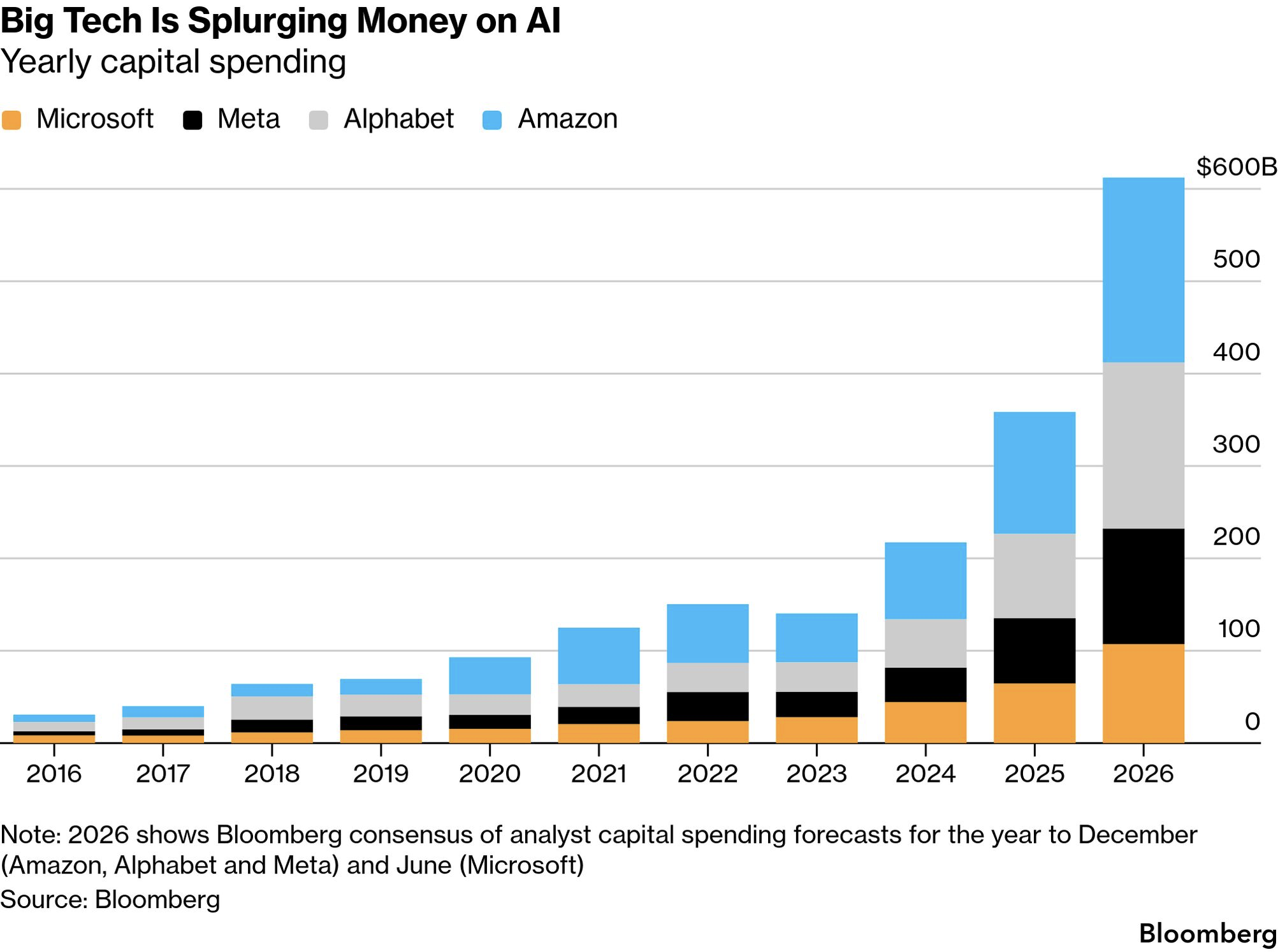

人工智能三年内迅速扩展至编码、法律和营销等高价值领域,但资本投入规模呈指数级膨胀,形成潜在金融风险。大型科技公司与初创企业计划投入数十亿至数万亿美元用于芯片、数据中心、电力和人才,四大科技公司2026年资本支出预计达6500亿美元。OpenAI承诺未来投入超过1.4万亿美元,Anthropic计划投入500亿美元。Bain估计,到2030年行业需约2万亿美元年收入支撑需求,但预测将短缺8000亿美元,显示投入与回报之间存在约40%的缺口。

用户与收入增长显著但仍不足以覆盖成本。ChatGPT周活跃用户超过9亿,Gemini月活跃用户从2025年5月的4亿增至超过7.5亿。OpenAI年化收入从约60亿美元增长至200亿美元以上,Anthropic接近200亿美元规模。然而商业模式仍以订阅为主,价格从每月数百美元向潜在数千美元探索,并尝试广告模式。尽管需求扩张,企业对AI价值转化存在“能力过剩”问题,即技术能力与实际商业价值之间的落差。

系统性风险集中于融资结构与供给约束。超大规模云厂商借贷预计从2025年的1650亿美元增至2026年的4000亿美元,债务依赖显著上升。同时,芯片厂商与AI开发商形成循环交易结构,可能放大亏损。基础设施瓶颈包括电网接入延迟与设备短缺,可能导致硬件折旧与投资回收周期错配。竞争层面,中国开源模型占全球下载约17%,首次超过美国,对定价能力形成压制。生产率提升证据分化:部分研究显示提升约15%,但也有任务耗时增加19%,企业裁员中仅2%直接归因于AI,表明经济回报路径尚未验证。

Artificial intelligence has expanded within three years into high-value domains such as coding, legal work, and marketing, while capital investment has scaled exponentially, creating potential financial risk. Big tech firms and startups plan to spend billions to trillions on chips, data centers, electricity, and talent, with four major tech companies projecting $650 billion in 2026 capex. OpenAI has committed over $1.4 trillion in future spending, and Anthropic plans $50 billion. Bain estimates the industry will require about $2 trillion in annual revenue by 2030, but expects an $800 billion shortfall, indicating a roughly 40% gap between investment and returns.

User and revenue growth are substantial but insufficient to offset costs. ChatGPT exceeds 900 million weekly users, while Gemini grew from 400 million monthly users in May 2025 to over 750 million. OpenAI’s annualized revenue rose from about $6 billion to over $20 billion, with Anthropic approaching a similar scale. Business models remain subscription-based, with pricing from hundreds to potentially thousands of dollars monthly, alongside emerging advertising strategies. Despite demand growth, a “capability overhang” persists, reflecting a gap between technical capability and realized business value.

Systemic risks center on financing structures and supply constraints. Hyperscaler borrowing is projected to rise from $165 billion in 2025 to $400 billion in 2026, signaling increased debt reliance. Circular deals between chipmakers and AI developers may amplify losses. Infrastructure bottlenecks include grid connection delays and equipment shortages, creating mismatches between hardware depreciation and investment recovery timelines. Competitive pressure is rising as Chinese open-source models reach about 17% of global downloads, surpassing US counterparts and constraining pricing power. Productivity evidence is mixed: some studies show ~15% gains, others report 19% slower task completion, and only 2% of layoffs are directly attributed to AI, indicating uncertain economic payoff.