巴西10月大选的走向将取决于犯罪与选民的钱包:在连续三年约3%的年增长、4.3%的年通胀与创纪录低失业率的背景下,反对派仍以“财政危机”和衰退风险为主轴。IMF预计总公共债务将从2010年的GDP占比62%升至2030年的99%,当前债务比新兴市场与拉美同侪的中位数高30个百分点,而8.1%的名义赤字几乎全部由利息支付构成。

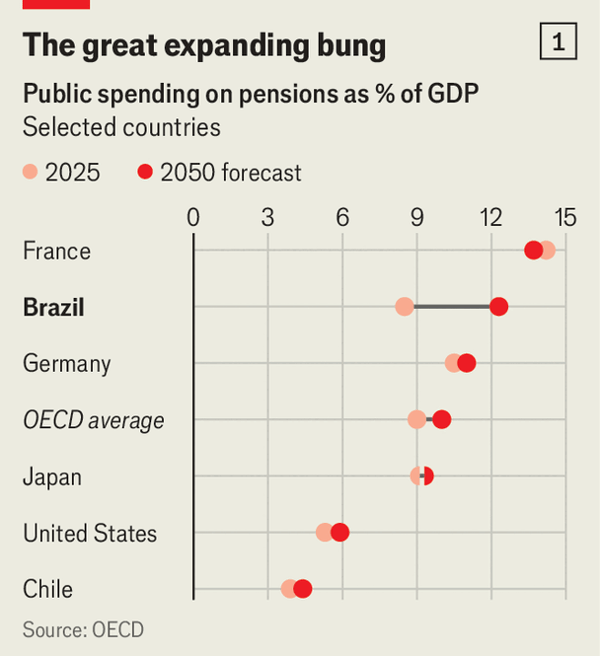

自2023年1月上任时继承相当于GDP 1.4%的初级盈余与约4.5%的总赤字,到2025年12月已变为GDP 0.4%的初级赤字,市场信心下滑迫使央行将实际利率维持在接近10%(全球最高之一),并在17%GDP的投资率(约为印度的一半)下挤出私营投资。被指责的福利支出为每年830亿美元、占GDP 3.7%,公共卫生与教育支出各约占GDP 4%与同侪相当;更大的拖累来自养老金与制度性约束:养老金成本达GDP 10%,社保缺口预计将从当前GDP 2%升至2060年超过16%,法院每年还会因判令高额养老金与福利支付而让联邦政府损失相当于GDP 2.5%。

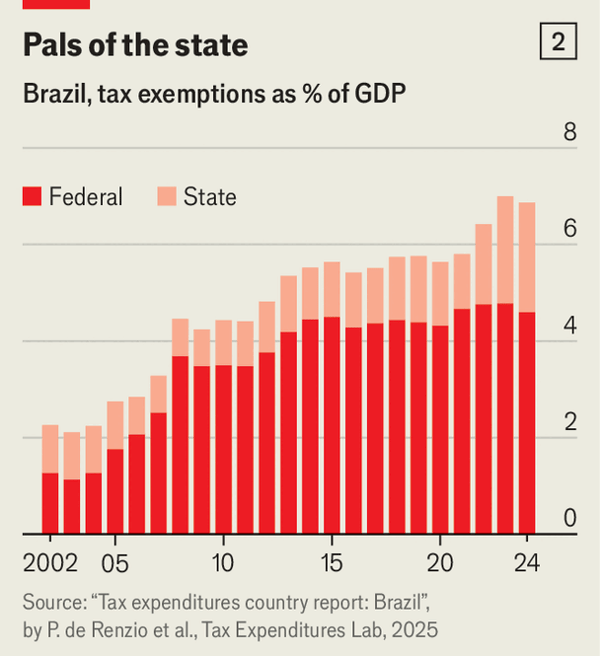

税制同样以复杂性与偏袒性压低增长:税收收入约占GDP 34%,但合规成本极高,德勤调查显示年营业额不超过9500万美元的企业平均每年花16,200小时报税,而销售额超过15亿美元的最大企业花63,000小时。公司税名义税率为34%,但有效税率仅16–18%;在1,650万家企业中只有22万家缴纳全额公司所得税,同时税收减免支出已从2003年的GDP 2%升至7%,128项减免制度中有95项将持续到2073;尽管自2019年起新减免需在5年内到期、2021年设定2029年将减免成本降至GDP 2%的上限、2023年以双重增值税简化消费税并可能在2033年全面实施时将GDP提高至多4.5%,但大量“例外条款”仍使经济面临停滞并走向危机的风险。

Brazil’s October general election will hinge on crime and voters’ finances: despite roughly 3% annual growth for three straight years, 4.3% annual inflation, and record-low unemployment, the opposition frames the outlook as a “fiscal crisis” with recession risk. The IMF projects gross public debt rising from 62% of GDP in 2010 to 99% in 2030, with today’s debt 30 percentage points above the emerging-market and Latin American median, alongside an 8.1% nominal deficit made up almost entirely of interest payments.

From inheriting a primary surplus of 1.4% of GDP and a total deficit around 4.5% in January 2023 to running a primary deficit of 0.4% of GDP by December 2025, deteriorating confidence has helped keep real interest rates near 10% (among the world’s highest) and, with investment at just 17% of GDP (about half India’s rate), has crowded out private investment. Welfare “handouts” cost $83bn a year or 3.7% of GDP, and public health and education each run near 4% of GDP, but the heavier drag is pensions and constitutional constraints: pensions cost 10% of GDP, the social-security shortfall is set to rise from 2% of GDP today to over 16% by 2060, and court rulings annually cost the federal government the equivalent of 2.5% of GDP in mandated pension and welfare payments.

The tax system also suppresses growth through complexity and preferential treatment: Brazil collects about 34% of GDP in tax revenue, yet Deloitte found firms up to $95m turnover spend 16,200 hours a year filing taxes while the largest firms (over $1.5bn sales) spend 63,000 hours. The corporate headline rate is 34% but the effective rate is only 16–18%, just 220,000 of 16.5m companies pay the full corporate rate, and tax breaks cost a staggering 7% of GDP (up from 2% in 2003) with 95 of 128 regimes lasting until 2073; reforms since 2019 (5-year expiries), 2021 (a 2% of GDP cap by 2029), and 2023 (dual VAT simplification potentially lifting GDP up to 4.5% by full implementation in 2033) still leave enough carve-outs to risk stagnation sliding into crisis.

Source: Brazil’s economy is being throttled by entrenched interests

Subtitle: The country should be faring much better

Dateline: 2月 12, 2026 06:38 上午 | Rio de Janeiro