中国领导层正大力推进人工智能、机器人技术和核聚变发电等前沿技术,这需要庞大的资金。仅人工智能数据中心估计在五年内就需要2万亿元人民币(2750亿美元)的资金,而机器人技术在十年内也需要类似的金额。为了给这些雄心壮志融资,习近平放宽了对科技行业的监管打压。因此,2026年前五个月有超过9,500只新股票基金成立,比前一年增加了50%。截至2025年底,国家引导的科技投资基金募集了2,300亿元新资金,高于一年前的110亿元。初创企业蓬勃发展;DeepSeek正以600亿美元的估值募集资金,估值超过10亿美元的初创企业数量从2025年的22家上升到今年上半年的80家。

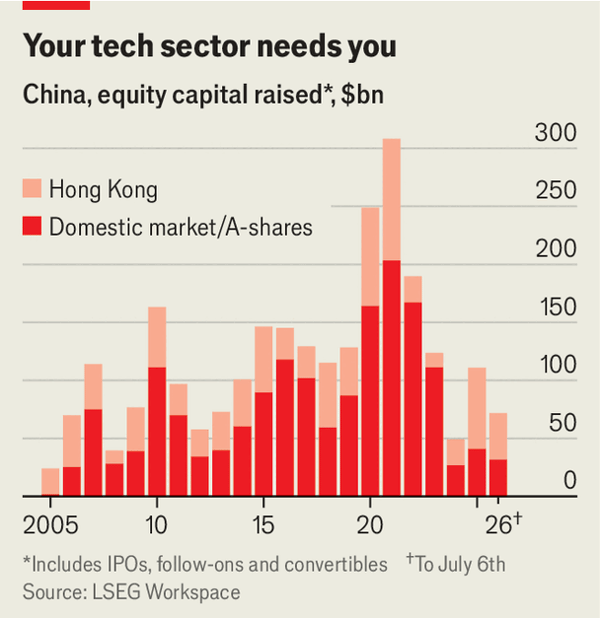

公共市场也在复苏,今年中国企业通过IPO筹集了320亿美元,是2025年水平的两倍,也是2024年的三倍。芯片制造商长鑫存储等科技公司正计划上市,其中长鑫存储的目标是筹集43亿美元。上海证券交易所的科创板已允许无利润的初创企业重新上市,使机器人公司宇树科技能够在100天内获批上市,而不是过去的一年或更长时间。然而,国家参与度很高。现在的模式不是私营企业资助国有企业,而是国有企业资助初创企业。中芯国际的基金持有400多家半导体公司的股份,并已将其中48家公司上市,另有50家计划上市。私营科技巨头也与政府机构合作;电动汽车制造商小米与湖北省政府共同创建了一只基金,进行了100多次投资。

这种国家主导的融资模式伴随着严格的条件。资金被引导至符合政府科技目标的公司,这有时会资助那些正在解决其他国家多年前已解决问题的公司。专业和私募投资者对国家干预以及证监会旨在将资金引导至习近平的目标同时维持“慢牛”市场的指令越来越感到担忧。散户投资者也相应地转移了资金,将资金从消费必需品(今年下跌15%)撤出,转入科技行业(创业板指上涨20%)。最终,这些僵化的政策指令可能会吓跑专业资本,使国有银行留下低效的资金配置,这可能会阻碍中国实现其科技雄心的能力。

China’s leadership is aggressively promoting frontier technologies like artificial intelligence, robotics, and fusion power, requiring massive capital. AI data centres alone are estimated to cost 2 trillion yuan ($275 billion) over five years, with robotics requiring a similar amount over a decade. To fund these ambitions, Xi Jinping has eased regulatory crackdowns on tech. Consequently, the first five months of 2026 saw over 9,500 new equity funds launched, a 50% increase from the prior year. State-directed tech-investment funds raised 230 billion yuan at the end of 2025, up from 11 billion yuan a year earlier. Startups are surging; DeepSeek is raising capital at a $60 billion valuation, and the number of startups valued over $1 billion rose to 80 in the first half of the year from 22 in 2025.

Public markets are also reviving, with Chinese firms raising $32 billion through IPOs this year—double the 2025 level and triple that of 2024. Tech firms like chipmaker CXMT are planning listings, with CXMT targeting a $4.3 billion float. Shanghai's STAR market has allowed profitless startups back, enabling robotics firm Unitree to list in 100 days instead of a year or more. However, state involvement is heavy. Rather than private firms funding state enterprises, state firms now back startups. SMIC's fund holds stakes in over 400 semiconductor firms and has listed 48 of them, with another 50 planned. Private tech giants also partner with government bodies; electric vehicle maker Xiaomi created a fund with the Hubei provincial government, making over 100 investments.

This state-led funding model comes with stringent conditions. Capital is directed to companies aligned with government tech goals, which sometimes fund firms working on problems solved years ago elsewhere. Professional and private investors are growing cautious about state intervention and the CSRC's mandate to direct capital to Xi's goals while maintaining a "slow bull" market. Retail investors are shifting capital accordingly, pulling money out of consumer staples (down 15% this year) and into tech (up 20% on the ChiNext index). Ultimately, these rigid policy mandates risk deterring professional capital and leaving state banks with inefficient allocations, which could hinder China's ability to achieve its technology ambitions.

Source: China may struggle to fund Xi Jinping’s tech dreams

Subtitle: Even though capital markets are staging a comeback

Dateline: Jul 09, 2026 08:40 AM | Shanghai