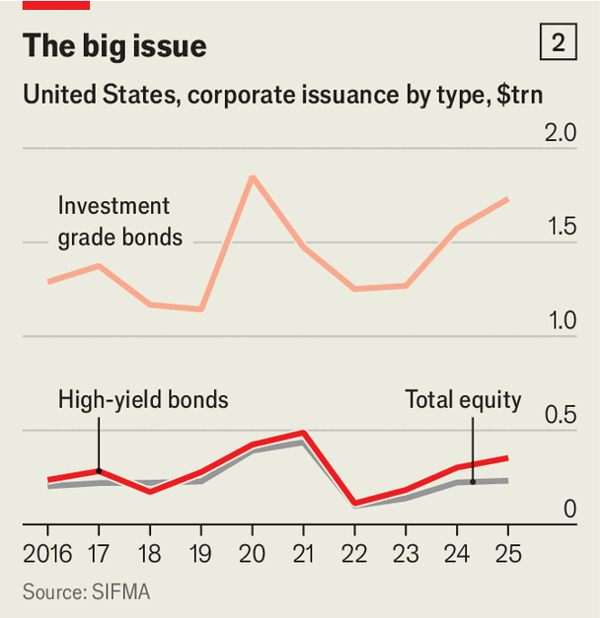

从历史上看,重大的技术推广(如19世纪的铁路繁荣)催化了公司债券市场的扩张。如今,人工智能的狂热正在推动类似的繁荣。自1月以来,Meta、英伟达和甲骨文各发行了价值250亿美元的债券,而SpaceX筹集了同等金额,亚马逊则售出了370亿美元的债券。Alphabet在英国发行了10亿英镑(14亿美元)的100年期债券,作为其55亿英镑债务发售的一部分,此外还在国内筹集了200亿美元。因此,美国公司债券发行量可能会在2026年打破2020年的记录。摩根士丹利预测,今年与AI相关的投资级债券发行量将达到3500亿至4000亿美元,占预测的2.3万亿美元高质量美元债券市场总额的近五分之一。与AI项目挂钩的垃圾债券可能会在4400亿美元的高收益总额中贡献另外的50亿美元。

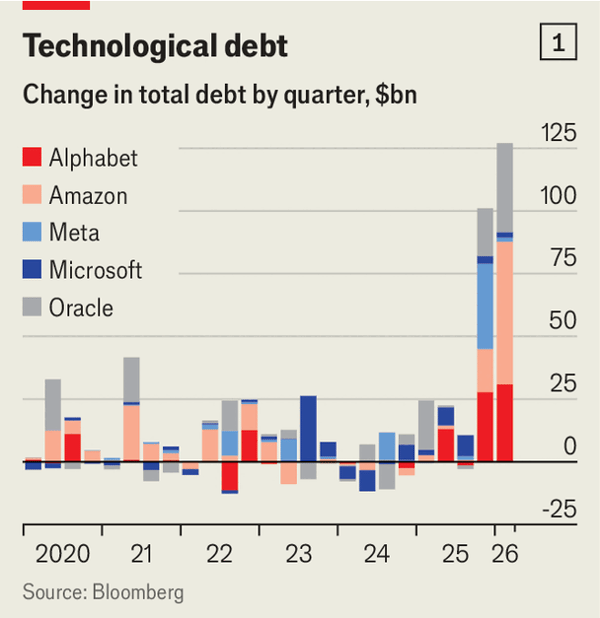

这种快速的债务积累引发了国际清算银行关于AI项目是否有能力产生足够收入来偿还债务的警告。尽管如此,超大规模云服务商的信誉使市场显得更加安全。在截至3月的六个月中,美国五大云巨头——Alphabet、亚马逊、Meta、微软和甲骨文——的债务总额增加了2280亿美元,创下了记录积累速度。这五家巨头中有四家保持着一流的信用评级,微软的债务被评为比美国国债更安全,只有甲骨文获得中等的“B”评级。反映出这种高信用质量,尽管发行量激增,但公司债券的平均利差仍保持在约0.8个百分点的极窄水平。

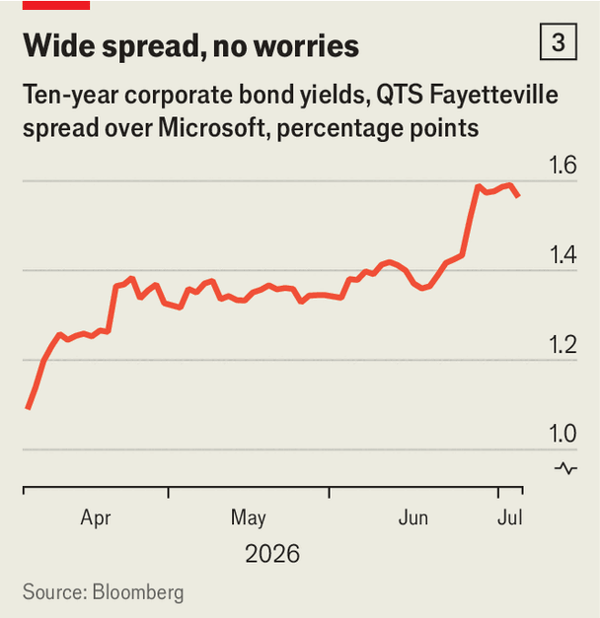

然而,投资者开始区分风险特征。例如,QTS数据中心为租给微软的佐治亚州服务器集群发行了46亿美元的债券,其相对于微软债务的收益率利差从1.1个百分点扩大到了1.6个百分点。由CoreWeave和其他“新云”发行可转换债券引领的垃圾债券市场也在扩张。虽然像1873年铁路违约等历史先例导致了全球萧条,但目前预计不会发生迫在眉睫的灾难。然而,随着快速发展的人工智能革命迅速改变市场领导者,债券投资者必须极具眼光,以避免在可能长达100年的漫长到期期限内发生违约。

Historically, major technology rollouts, such as the railway boom in the 19th century, have catalyzed corporate bond market expansions. Today, the artificial intelligence frenzy is driving a similar boom. Since January, Meta, Nvidia, and Oracle have each launched bond offerings worth $25 billion, while SpaceX raised an equivalent sum, and Amazon sold $37 billion in bonds. Alphabet issued a £1 billion ($1.4 billion) 100-year bond in Britain as part of a £5.5 billion debt sale, alongside a $20 billion domestic offering. Consequently, U.S. corporate bond issuance will likely shatter the 2020 record in 2026. Morgan Stanley forecasts that AI-related investment-grade issuance will reach $350 billion to $400 billion, representing nearly a fifth of the total predicted high-quality dollar bond market of $2.3 trillion. Junk bonds tied to AI could contribute another $50 billion of the $440 billion high-yield total.

This rapid debt accumulation has prompted warnings from the Bank for International Settlements regarding the ability of AI projects to generate enough revenue for repayment. Nevertheless, the creditworthiness of hyperscalers makes the market appear safer. U.S. cloud giants—Alphabet, Amazon, Meta, Microsoft, and Oracle—increased their collective debt by $228 billion in the six months leading to March, a record rate of accumulation. Four of these hyperscalers maintain stellar credit ratings, with Microsoft’s debt rated safer than U.S. Treasuries, while only Oracle receives a middling "B" grade. Reflecting this high credit quality, average corporate bond spreads remain extremely narrow at approximately 0.8 percentage points, despite the surge in issuance.

However, investors are beginning to differentiate risk profiles. For example, QTS Data Centers issued $4.6 billion in bonds for a Georgia server farm leased to Microsoft, with its yield spread over Microsoft's debt widening from 1.1 to 1.6 percentage points. The junk bond market is also expanding, led by CoreWeave and other "neoclouds" issuing convertible bonds. While historical precedents like the 1873 railway defaults resulted in global depressions, no imminent cataclysm is expected. Yet, as the fast-paced AI revolution rapidly alters market leaders, bond investors must be highly discerning to avoid defaults over long maturities, which can span up to 100 years.

Source: AI has taken over the stock market. The bond market is next

Subtitle: Judging credit risk of the AI boom is difficult

Dateline: Jul 09, 2026 06:44 AM | New York