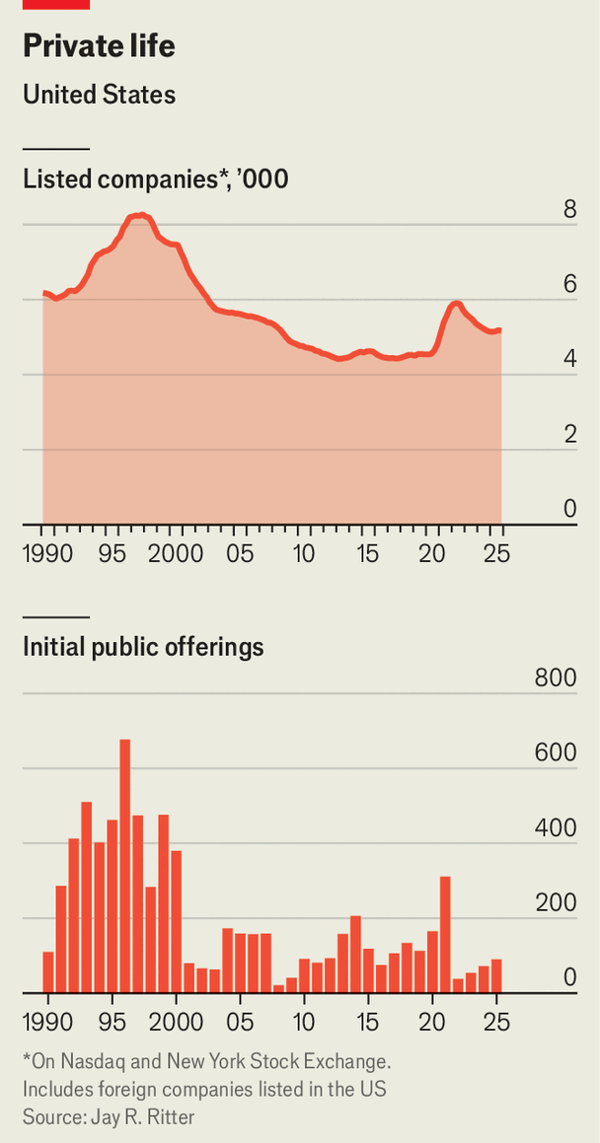

任何曾经“未经历过上市公司阶段”的公司,如今都可能在重新考虑,SpaceX据报道计划在IPO中筹集750亿美元($75bn),市值约1.75万亿美元($1.75trn),其规模超过2019年沙特阿美(Saudi Aramco)当时的最高记录一倍多,有望成为有史以来最大的IPO,而且OpenAI和Anthropic也可能同场上市。 在美国上市公司数量自1990年代中期以来已下降了三分之一以上,买断者和初创公司留在风险投资方名下或并入大公司逐渐占主导,监管者、交易所与指数机构正推动扭转企业向私有化偏离的趋势。

美国证券交易委员会(SEC)正在提出减轻监管负担的方案,包括将上市公司报表改为每年两次而非季度报送、削减气候等披露要求,并削弱代理顾问与集体诉讼原告等外部力量对管理层的影响。 指数编制方也在加速入选条件调整,纳斯达克把某些公司入指数的“成熟期”从3个月到一年缩短为15个交易日,LSEG对罗素指数建议5个交易日,并考虑降低最低流通股门槛,这会增加被动基金的提前买入压力。

这些改革可能吸引AI时代资本流入,但也可能造成失真:缩短成熟期可能让被动基金在价格未充分发现前买入,而降低自由流通股比例会在需求上升时压缩可交易供给。 根据University of Florida的Jay Ritter数据显示,自1980年以来,最初仅发行不足5%股份的大型公司中,仅有一家在后三年内跑赢市场,因此这次变动的市场定价与股东分配后果值得警惕。 如果三大超级IPO实现,上市市场将重新增强其规模竞争力,但私有部门的议价能力仍然强,SpaceX在“到火星”愿景下对公众融资的依赖使其成为核心试金石。

Any company with no public-company experience may now be reconsidering, as SpaceX is reported to seek $75bn in its IPO at about a $1.75tn valuation, more than double Saudi Aramco’s 2019 record, positioning it as the largest IPO ever and with OpenAI and Anthropic also reportedly in line. U.S. public listings have fallen by more than one-third since the mid-1990s, with buyouts and private ownership routes becoming dominant, so regulators, exchanges, and index firms are now trying to reverse the drift away from public markets.

The SEC is proposing lighter rules, including replacing quarterly reporting with semi-annual filings, cutting disclosure requirements such as climate reporting, and reducing outside influence from proxy advisers and class-action plaintiffs. Index providers are also changing inclusion rules, with Nasdaq cutting the post-IPO seasoning period from three months to one year down to 15 trading days, LSEG proposing five days for Russell indices, and lower float thresholds under consideration, all of which can force earlier passive-fund buying.

These reforms may attract AI-era capital, but they could also create distortions: a shorter seasoning period can make passive funds buy before true price discovery, and lower free-float can raise demand while constraining supply; since 1980, all but one large company that initially floated under 5% of shares underperformed the market over the next three years. If the mega-IPOs materialize, public markets may regain scale and depth, but private-sector bargaining power remains strong, and SpaceX becomes a key test because its ambitions still require access to public capital.

Source: The plan to make IPOs great agai

Subtitle: America’s regulators and market operators are teaming up to rekindle public listings

Dateline: 4月 01, 2026 03:22 上午