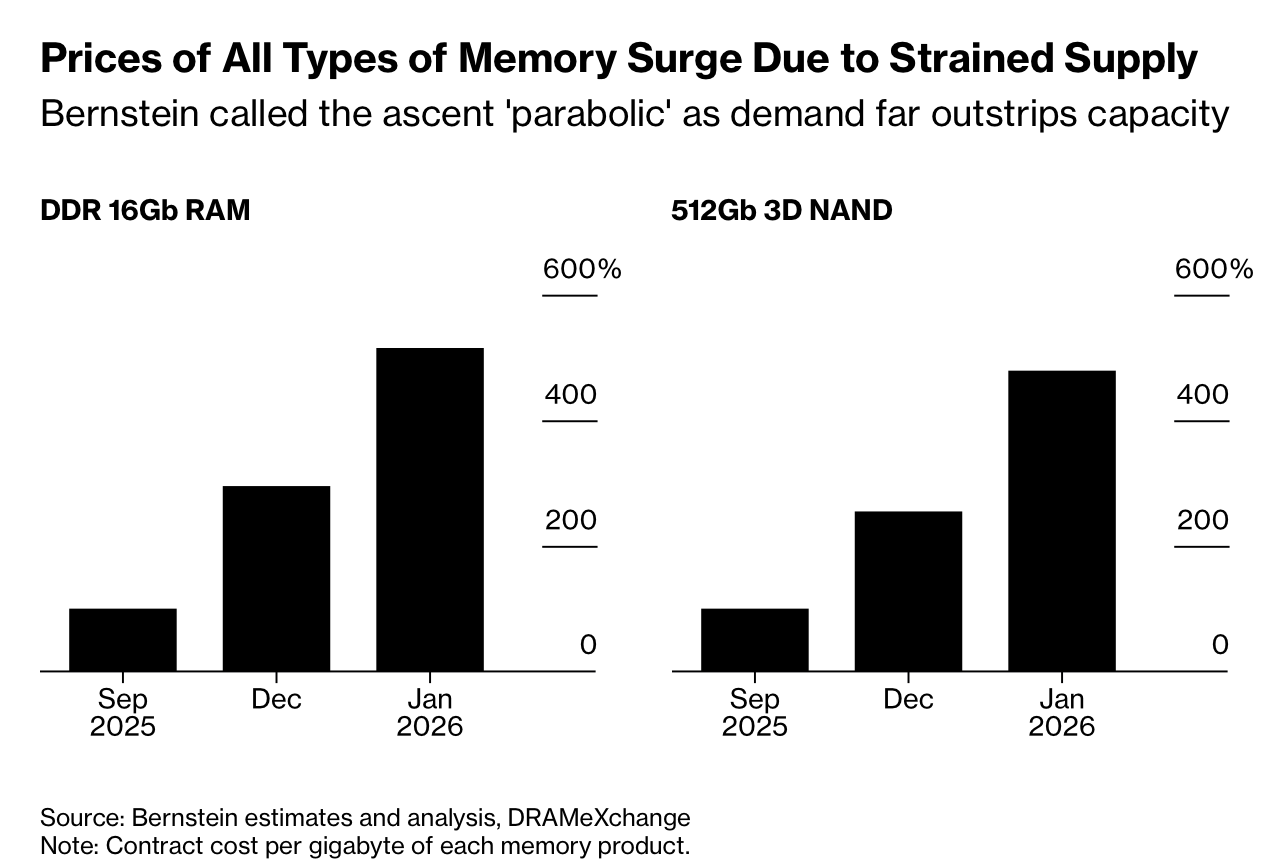

文中证据显示价格与需求正在快速加速:某一类 DRAM 在 December 到 January 上涨 75%,合约行为由年度转为约每季度检视,下游公司正在削减或重订价格方案。据报导,Oppo 将其 2026 出货预测下调最多 20%;Sony 正考虑把下一代 PlayStation 上市延后至 2028 或 2029;客制化 PC 厂商 Falcon Northwest 表示其 2025 平均售价上升 $1,500 至约 $8,000。AI 硬体的高记忆体强度是核心驱动:Nvidia Blackwell 配备 192 GB RAM(约为高阶 PC 的 6x),NVL72 配置将 72 颗晶片与 13.4 TB RAM 结合,而一套 NVL72 系统被描述为消耗约等同 1000 部高阶智慧型手机的记忆体。

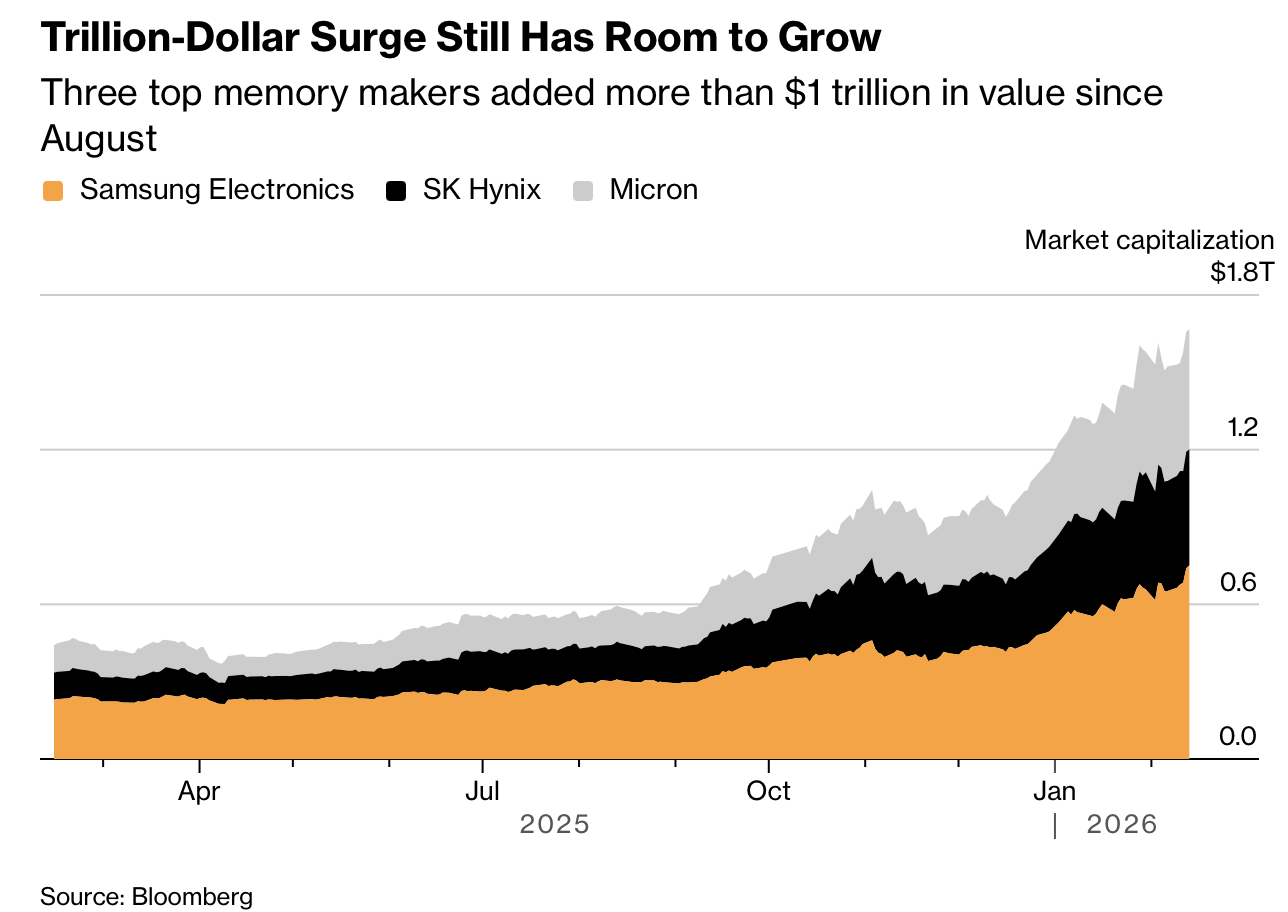

文章认为,这一转变正在把晶圆产能重新分配到 HBM,并远离通用型 DRAM,从而在电子、电信与汽车领域造成持久短缺。TrendForce 估计 2026 年 HBM 需求将年增 70%,且 HBM 将占 DRAM 晶圆总产出的 23%,高于 2025 的 19%;GF Securities 估计 DRAM 与 NAND 的基准供需缺口分别为 4% 与 3%,且因库存偏低,实际情况可能被低估。利润集中现象明显:Micron 在截至 August 的财年营收预计将超过翻倍;SK Hynix 销售额在 2024 已超过翻倍,并在 2026 仍可能再翻倍;对消费端的影响包括低阶智慧型手机物料成本中 DRAM 占比,从 2025 年初的 10% 走向接近 30%,意味著 2026 期间对通膨敏感的装置价格将更高。

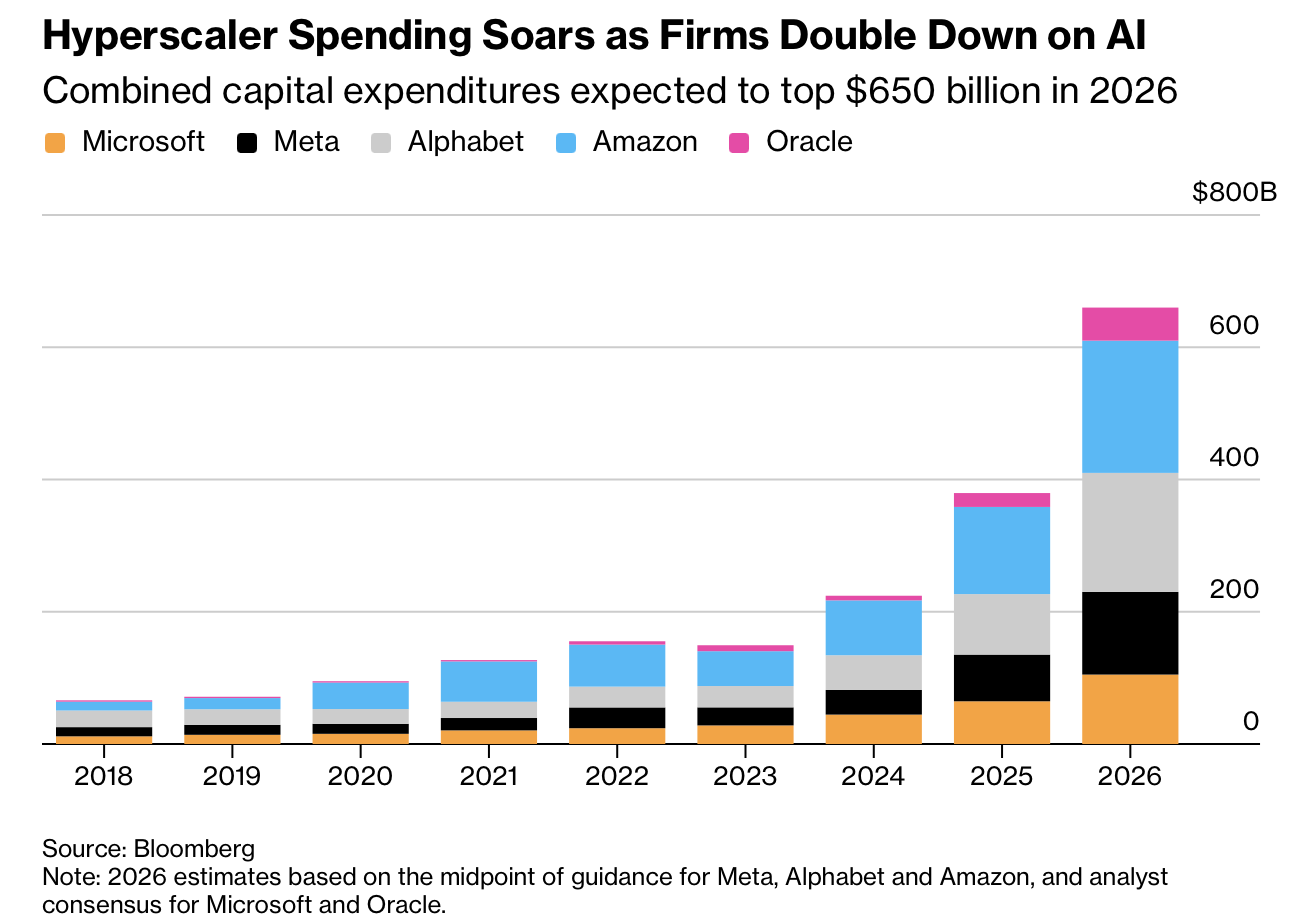

The article describes a fast-intensifying 2026 global memory-chip shortage driven by AI infrastructure, with major companies including Tesla and Apple warning that DRAM constraints are already reducing output and squeezing margins. The stress is appearing before the largest buildouts are complete, as Alphabet and Amazon announced 2026 capex programs that could reach $185 billion and $200 billion, while broader big-tech AI infrastructure spending is projected to jump from $217 billion in 2024 to about $360 billion in 2025 and then to roughly $650 billion in 2026. Executives characterize the imbalance as structural rather than temporary, with industry leaders saying demand through 2030 will exceed any prior cycle.

Evidence in the piece points to rapid price and demand acceleration: one DRAM category rose 75% from December to January, contract behavior shifted from annual to roughly quarterly reviews, and downstream companies are cutting or repricing plans. Oppo reportedly reduced its 2026 shipment forecast by up to 20%, Sony is considering delaying its next PlayStation launch to 2028 or 2029, and custom PC maker Falcon Northwest said its average selling price increased by $1,500 to around $8,000 in 2025. AI hardware intensity is the core driver: Nvidia Blackwell carries 192 GB RAM (about 6x a high-end PC), an NVL72 configuration combines 72 chips with 13.4 TB RAM, and one NVL72 system is described as consuming memory equivalent to about 1000 high-end smartphones.

The article argues this shift is reallocating wafer capacity toward HBM and away from commodity DRAM, creating prolonged shortages across electronics, telecom, and autos. TrendForce estimates HBM demand will rise 70% year over year in 2026, with HBM consuming 23% of total DRAM wafer output versus 19% in 2025; GF Securities estimates baseline supply-demand gaps of 4% for DRAM and 3% for NAND, likely understated due to low inventories. Profit concentration is stark, with Micron revenue expected to more than double in its fiscal year ending August and SK Hynix sales having more than doubled in 2024 with another potential doubling in 2026, while consumer impact includes DRAM share of low-end smartphone bill of materials rising toward 30% from 10% in early 2025, implying higher inflation-sensitive device prices through 2026.