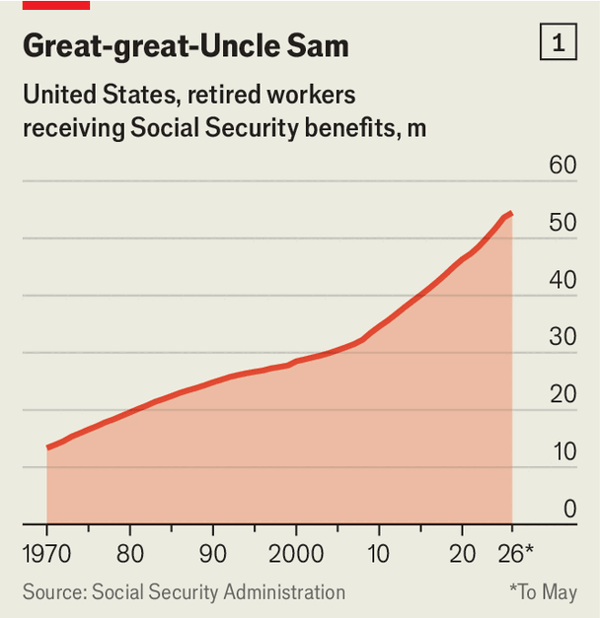

尽管美国的个人消费在过去一年增长了2%,但4月份的个人储蓄率降至2.6%,为2008年金融危机以来的最低点。随着年度通胀率三年来首次超过工资增长速度,且每户家庭350美元的一次性退税提振已基本耗尽,批评人士认为消费者正在耗尽现金。然而,这一低储蓄率的主要结构性驱动因素是人口结构:5月份领取社会保障金的美国人达到了5450万,这些退休人员自然会动用他们积累的储蓄来支付其支出。

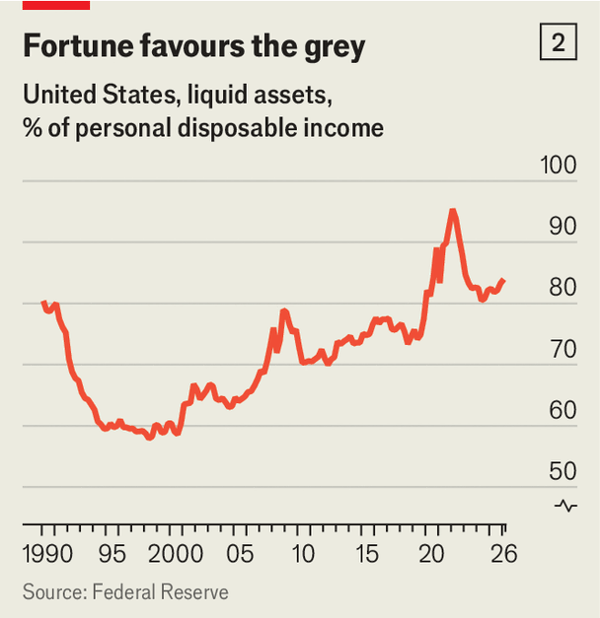

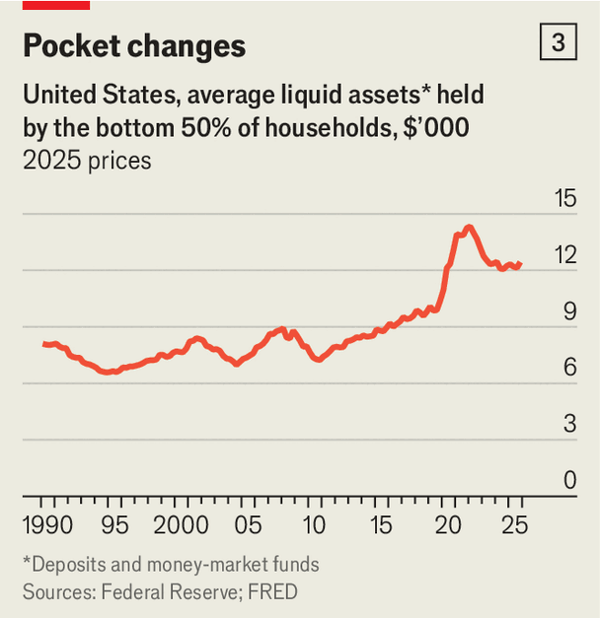

美联储的研究估计,典型的退休人员每年的支出比其年收入多出15000至22000美元,这种“负储蓄”趋势将全国总体储蓄率拉低了略多于五个百分点。与此同时,家庭资产负债表依然强劲;现金和银行存款等流动资产占年可支配收入的84%,而大流行前的三十年里这一比例低于70%。这一财务缓冲也延伸到了较不富裕的人群,财富最后50%的家庭平均持有12800美元的流动余额,扣除通胀因素后高于大流行前的任何时期。

私营部门的数据证实了具有韧性的消费活动,5月份银行卡支出同比增长近5%,沃尔玛报告了自2024年以来最快的交易增长。尽管目前表现强劲,但消费者仍暴露在外部经济冲击之下。风险包括可能影响退休人员财富的股市调整、居高不下的石油价格,以及来自预期关税和美墨加协定(USMCA)重新谈判的贸易干扰。

Although America's personal consumption has grown by 2% over the past year, the personal savings rate fell to 2.6% in April, its lowest point since the 2008 financial crisis. With annual inflation outpacing wage growth for the first time in three years and one-time tax refund boosts of $350 per household largely depleted, critics argue that consumers are running out of cash. However, a major structural driver of this low rate is demographic: the number of Americans collecting Social Security reached 54.5 million in May, and these retirees naturally draw down their accumulated savings to fund their spending.

Federal Reserve research estimates that a typical pensioner spends $15,000 to $22,000 more than their annual income, a trend of "dissaving" that reduces the national headline saving rate by just over five percentage points. Meanwhile, household balance sheets remain robust; liquid assets like cash and bank deposits represent 84% of annual disposable income, compared to under 70% in the three decades preceding the pandemic. This financial cushion extends to the less wealthy, with the bottom 50% of households holding average liquid balances of $12,800, which is higher in real terms than any pre-pandemic period.

Private sector data confirms resilient consumer activity, with card spending rising nearly 5% year-on-year in May and Walmart reporting its fastest transaction growth since 2024. Despite this current strength, consumers remain exposed to external economic shocks. Risks include a potential stock market correction that would impact retiree wealth, elevated oil prices, and trade disruptions from prospective tariffs and renegotiations of the USMCA.

Source: How stretched is the American consumer?

Subtitle: The household saving rate has plunged—but don’t panic

Dateline: 6月 25, 2026 03:28 上午