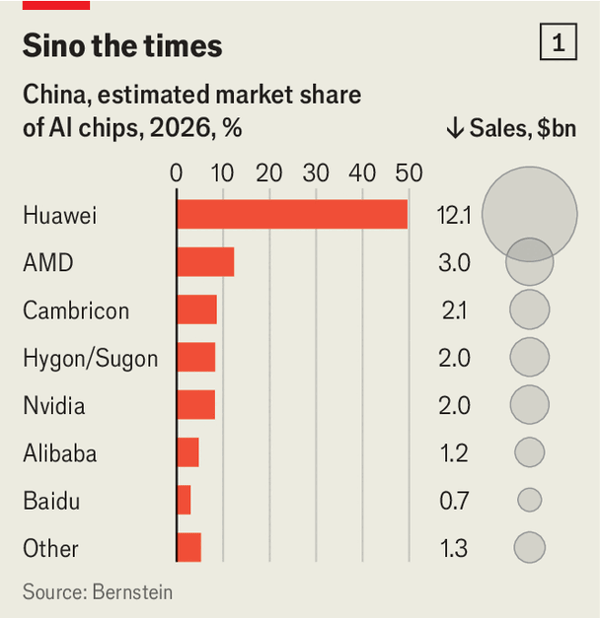

随着人工智能使半导体变得极具利润,中国实现芯片自给自足的努力也在加剧。尽管截至2025年底,中国的计算能力仅为美国的七分之一,但投资者信心正在飙升;港股上市的芯片股票在过去一年中上涨了140%。监管机构正引导国内企业远离外国芯片,导致本土设计商预计将占领今年中国AI芯片支出的五分之四。阿里巴巴和百度正在内部设计芯片,而寒武纪等初创企业在受保护的市场中蓬勃发展。这一扩张得到了庞大预期支出的支持:本土云巨头计划在三年内向AI基础设施投入超过4000亿美元,而政府计划在五年内向数据中心投入2950亿美元。

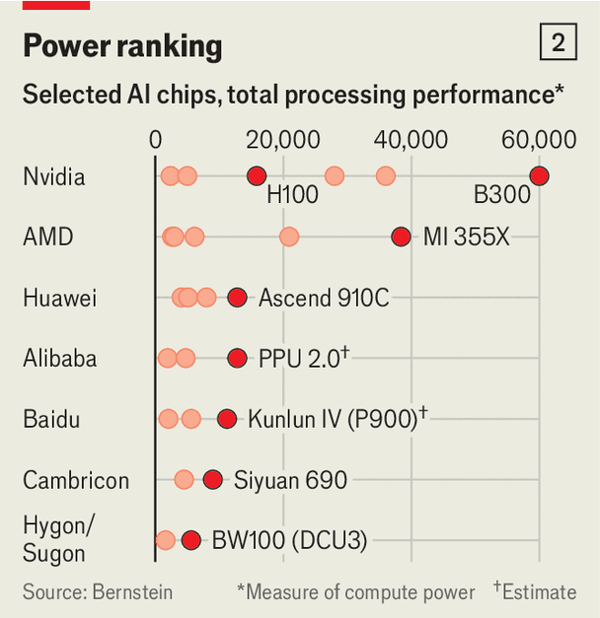

中国拥有深厚的人才储备,许多设计师曾在英伟达和超微半导体接受培训。中国开发人员正利用软硬件集成和变通方法(例如将384个升腾处理器连接起来以挑战英伟达系统的华为CloudMatrix系统,尽管其消耗的电量高出四倍)来挑战英伟达的系统。他们还在通过华为的CANN平台缩小软件差距,并使模型适应本土芯片,如DeepSeek的语言模型。然而,巨大的性能差距依然存在:华为的升腾910C仅提供英伟达H100(发布于四年前)性能的五分之四。国产芯片在基础推理任务之外的竞争中十分吃力,且由于美国的制裁和阿斯麦光刻机出口禁令,它们基本上被禁止使用7纳米以下的高级制造工艺。

为了在制造业赶超,自2019年以来,中国芯片制造设备的年进口额已翻了三倍,达到390亿美元,占全球需求的40%。北方华创和中微半导体等本土工具制造商正在提供具有竞争力的工具,长鑫存储预计到2028年将占据全球高带宽内存产量的12%。尽管如此,由于极紫外光刻技术距离国内复制估计还有十年的时间,中国芯片制造商依靠使用较旧的深紫外机器,采用成本更高的“多重曝光”和先进封装变通方法。与此同时,全球需求依然强劲;苹果甚至正寻求美国批准购买长鑫存储的旧代内存芯片,凸显了遏制中国不断崛起的半导体行业的难度。

As artificial intelligence makes semiconductors highly lucrative, China's drive for chip self-sufficiency has intensified. Although China's compute capacity was only one-seventh of America’s at the end of 2025, investor confidence is surging; Hong Kong-listed chip stocks rose 140% over the past year. Regulators are steering domestic firms away from foreign chips, leading local designers to capture an estimated four-fifths of AI chip spending in China this year. Alibaba and Baidu are designing chips in-house, while startups like Cambricon thrive in a protected market. This expansion is supported by massive projected spending: local cloud giants plan to spend over $400 billion on AI infrastructure over three years, while the government plans $295 billion for data centres over five years.

China boasts a deep talent pool, with many designers trained at Nvidia and AMD. Chinese developers are using software-hardware integration and workarounds, such as Huawei's CloudMatrix which links 384 Ascend processors, to challenge Nvidia's systems, despite using four times more power. They are also closing the software gap with Huawei's CANN platform and tuning models to local silicon, like DeepSeek's LLM. However, a significant performance gap remains: Huawei’s Ascend 910C delivers only four-fifths of the performance of Nvidia’s H100, which was released four years ago. Homegrown chips struggle to compete outside of basic inference tasks, and they are largely barred from using advanced manufacturing processes under 7 nanometres due to U.S. sanctions and ASML lithography export bans.

To catch up in manufacturing, China has tripled its annual imports of chipmaking equipment since 2019 to $39 billion, representing 40% of global demand. Local toolmakers like Naura and AMEC are offering competitive tools, and CXMT is projected to capture 12% of global high-bandwidth memory production by 2028. Nonetheless, without extreme-ultraviolet lithography, which is estimated to be ten years away from domestic replication, Chinese chipmakers rely on costlier "multi-patterning" and advanced packaging workarounds using older deep-ultraviolet machines. Meanwhile, global demand remains strong; Apple is even seeking U.S. permission to purchase older memory chips from CXMT, highlighting the difficulty of containing China's rising semiconductor industry.

Source: China’s semiconductor industry is racing to catch the West’s

Subtitle: But it is proving easier to design chips than to make them

Dateline: Jul 09, 2026 05:22 AM | TAIPEI