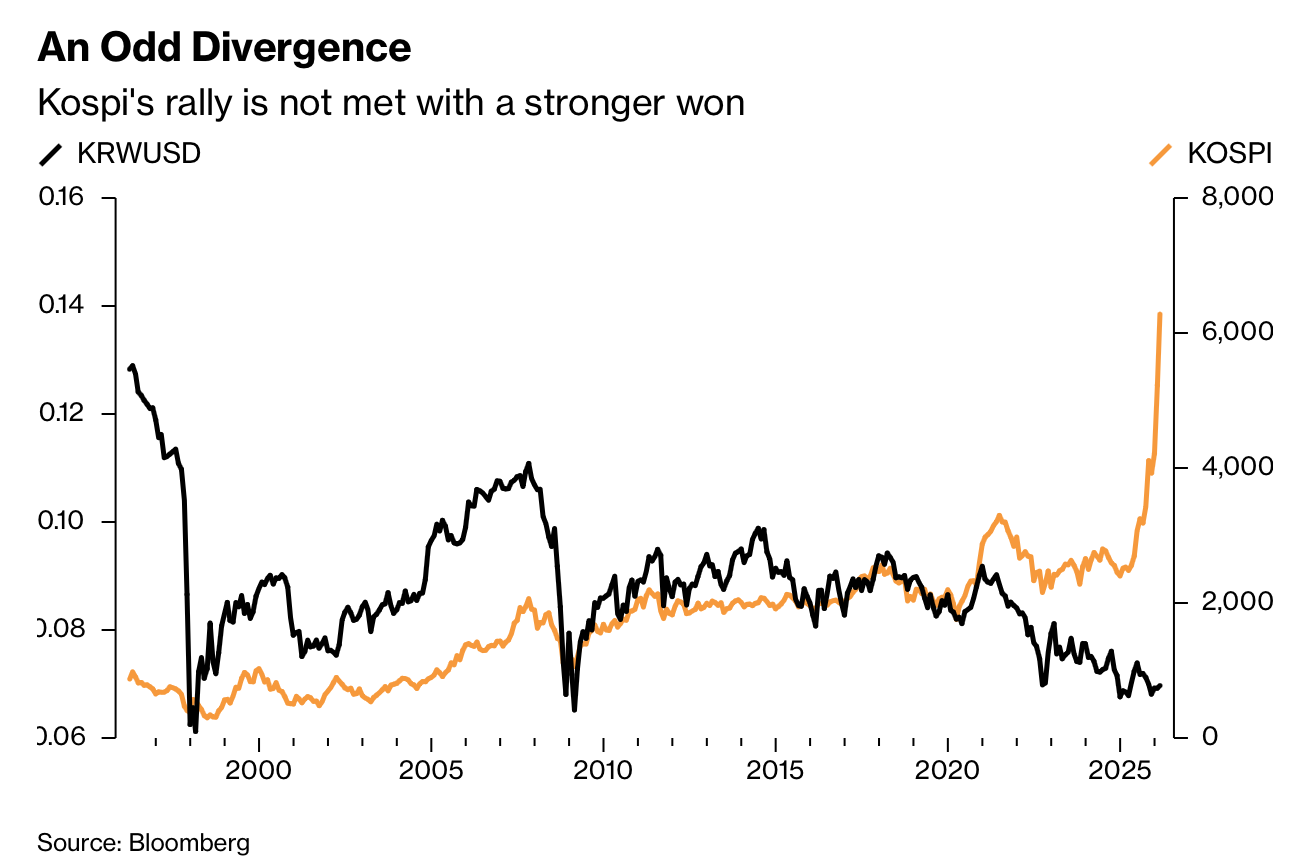

南韩的情况最能体现这种脱钩:KOSPI指数大幅上涨,同时韩元仍在贬值,破坏了过去危机时期股指与汇率同时下跌的历史联动。核心推手之一是南韩散户长期偏好美国资产;2025年其净买入美国股票达到32十亿美元(3.2×10^10美元),再创历史高。若这些资金转回国内投资,特别是投入本土科技企业,韩元将面临快速升值的风险。

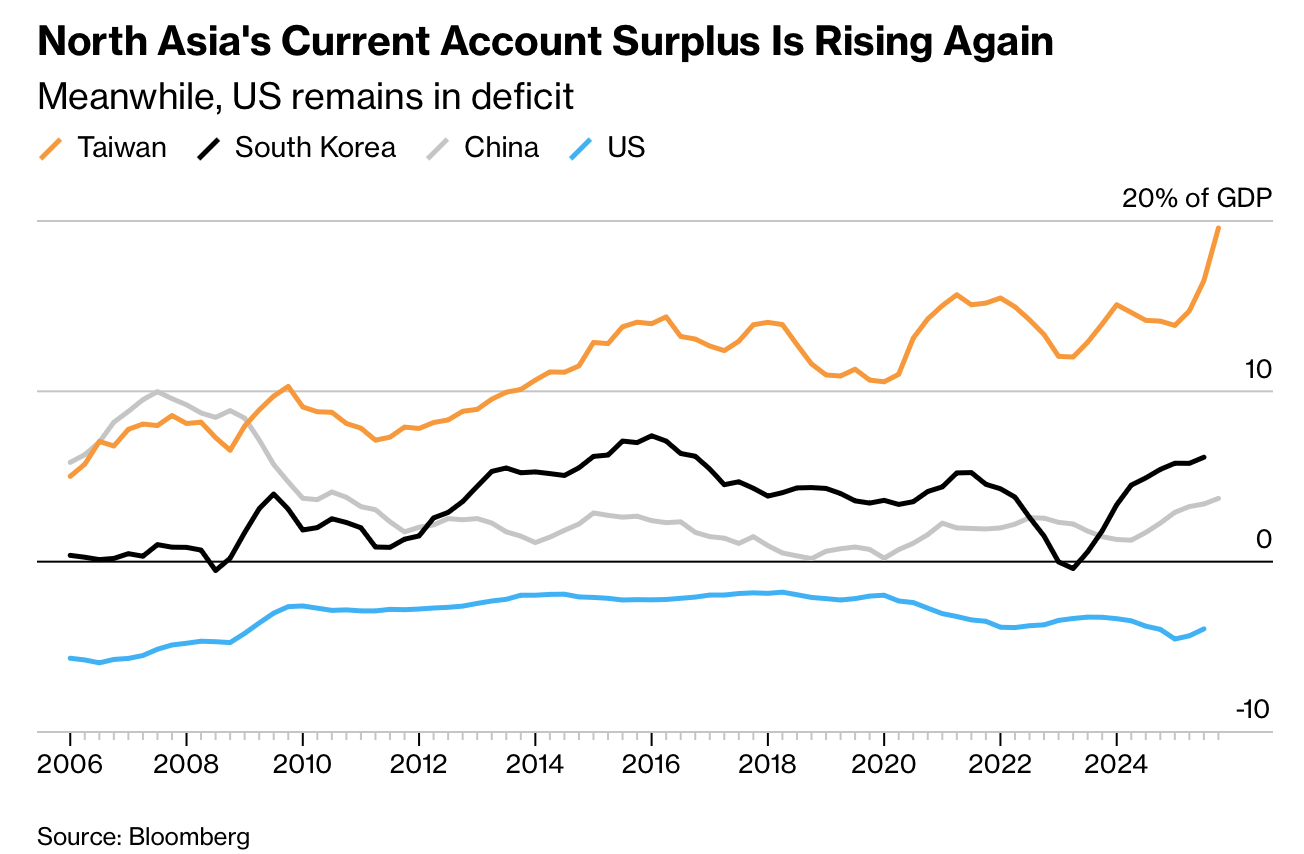

区域层面上,扩大的贸易顺差和资产配置转移正共同放大这一现象。据报导,中国贸易顺差从2023年的约8200亿美元(8.2×10^11美元)上升到去年约1.2兆美元(1.2×10^12美元);其出口企业此前将盈余大量停放在香港,美元存款规模增加约3,200亿美元(3.2×10^11美元)。当S&P 500回报放缓、美元走弱时,财务管理者开始将美元换成本币;人民币对美元连续上涨的纪录已延续自2010年以来最长。Goldman Sachs认为,美国目前已成为逆差方,为稳定净国际投资头寸,可能需将经常帐逆差降到GDP的2%。因此,「Sell America」式回流可能成为未来汇率市场新的关键扰动来源,并可能引发急剧调整。

In the March 2, 2026 Bloomberg Opinion piece, Shuli Ren argues that capital flows in North Asia may be reversing: money is returning home instead of moving out, a mirror image of the late-1990s pattern. In May 2025, the Taiwan dollar surged on speculation that Donald Trump would ask export-dependent economies to let their currencies appreciate in U.S. trade deals. The move looked crisis-like, but in 2025 the one-way pressure was aimed at the U.S. dollar itself, which faced heavy selling. Even after the U.S. Supreme Court limited Donald Trump’s ability to use tariffs as bargaining chips, dollar weakness has not disappeared, suggesting that repatriation flows may intensify as market positioning and regional risk appetite are repriced.

South Korea illustrates this decoupling. The Kospi index rallied sharply while the won weakened, breaking the historical pattern in which stocks and currency usually fell together in stress periods. A major driver has been strong domestic appetite for U.S. equities: in 2025, South Korean retail investors made net purchases of US$32 billion (US$3.2×10^10) in U.S. stocks, another historical peak. If these funds shift back to domestic investments, especially local technology firms, the won could revalue quickly upward.

Across the region, widening trade surpluses and asset-allocation shifts are reinforcing this trend. China’s trade surplus reportedly rose from about US$820 billion (8.2×10^11) in 2023 to roughly US$1.2 trillion (1.2×10^12) last year, and dollar placements in Hong Kong reportedly rose by around US$320 billion (3.2×10^11) as exporters parked earnings for higher dollar returns. As S&P 500 returns cooled and the dollar weakened, treasurers began converting dollars into local currencies; the yuan then posted its longest winning streak against the greenback since 2010. Goldman Sachs says the United States, now the deficit side, may need to cut its current account deficit to 2% of GDP to stabilize its net international investment position, making Sell America-style repatriation a potential trigger for another abrupt repricing of currencies.