2月8日超级碗播出的Claude广告让人想起2000年互联网狂热:当年多达17家“dotcom”公司为30秒广告位各自支付数百万美元,数周后股价进入残酷熊市。如今AI投资情绪也在摇摆,Alphabet、Amazon、Meta和Microsoft称来年合计将投入6600亿美元用于AI;公布后股价均下跌(Meta起初上涨),其中Microsoft下跌16%。

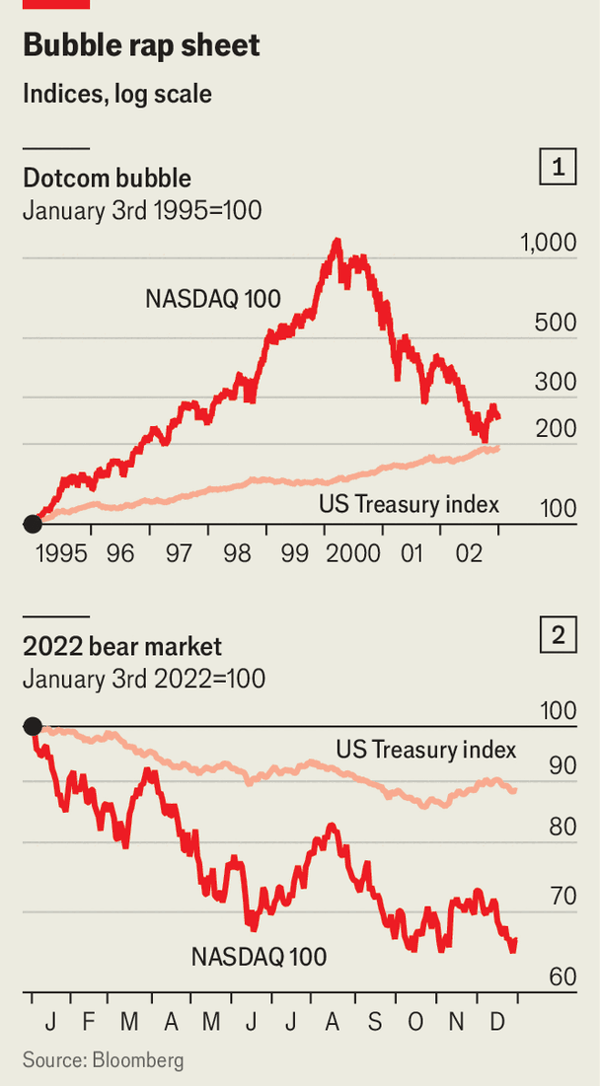

卖出股票虽是最直接的避险,但历史显示“贵”不等于立刻崩盘:纳斯达克在1995年初至2000年3月见顶的5年里至少出现十多次10%或以上的回调,却最终接近上涨12倍,而从1995年初买入并持有到随后暴跌的底部仍可资金翻倍。同期对冲更有效的组合是股票配债券:1995年初到2000年3月,彭博美国国债总回报指数上涨近50%,纳斯达克从峰值跌到谷值时该指数又上涨约30%,但2022年股债同跌与通胀风险使这种对冲在今天更不确定。

期权对冲可用“保护性看跌”把最大跌幅截断:例如把执行价设为现价的90%可将亏损限制在10%,而目前一年期、把标普500未来一年亏损限制在10%的看跌期权成本约为受保护金额的3.6%。高盛比较1996-2002年两种覆盖策略:一年期、限亏10%的序列与一月期、限亏4%的序列,前者年化回报大致与不对冲股票相当(但波动更小),后者因反复付费回报明显更差;在“非债券分散”中,1996-2002年把标普500与“低波动”子指数(主指数中波动最小的100只股票)或“分红贵族”指数(连续25年每年提高分红的公司)各做50/50分配,年化超额回报(相对现金)几乎是单独持有标普500的两倍。

A Claude ad aired during the Super Bowl on February 8 echoes the 2000 internet mania: as many as 17 dotcom firms paid millions of dollars each for 30-second slots, and share prices slid into a brutal bear market weeks later. Today AI confidence is wobbling as Alphabet, Amazon, Meta, and Microsoft plan a combined $660bn of AI spending in the coming year; each stock has fallen after its announcement (Meta jumped at first), and Microsoft is down 16%.

Selling stocks is the cleanest hedge, but “expensive” can persist: in the five years from early 1995 to the NASDAQ’s March 2000 peak it suffered at least a dozen 10%+ corrections yet rose nearly 12-fold, and even holding from early 1995 to the later trough would have doubled money. A stock-and-bond buffer worked then: from early 1995 to March 2000 Bloomberg’s US Treasury total-return index rose nearly 50%, and as the NASDAQ fell peak-to-trough the same index rose about 30%, but 2022’s joint stock-bond drawdown and inflation risk make that hedge less certain now.

Options can cap losses: setting a put strike at 90% of today’s price limits losses to 10%, and a one-year S&P 500 put that limits losses to 10% currently costs about 3.6% of the protected amount. Goldman’s 1996-2002 comparisons found one-year 10% puts delivered roughly the same annualised return as unhedged stocks (with less volatility) while rolling one-month 4% puts was substantially worse due to accumulated costs; among non-bond diversifiers, 50/50 splits with the S&P 500 low-volatility subindex (the 100 least volatile stocks) or the dividend aristocrats index (25 straight years of dividend increases) produced nearly twice the annualised excess returns over cash versus the S&P 500 alone.

Source: How to hedge a bubble, AI editio

Subtitle: Protecting your portfolio from a crash looks harder than ever

Dateline: 2月 12, 2026 09:34 上午