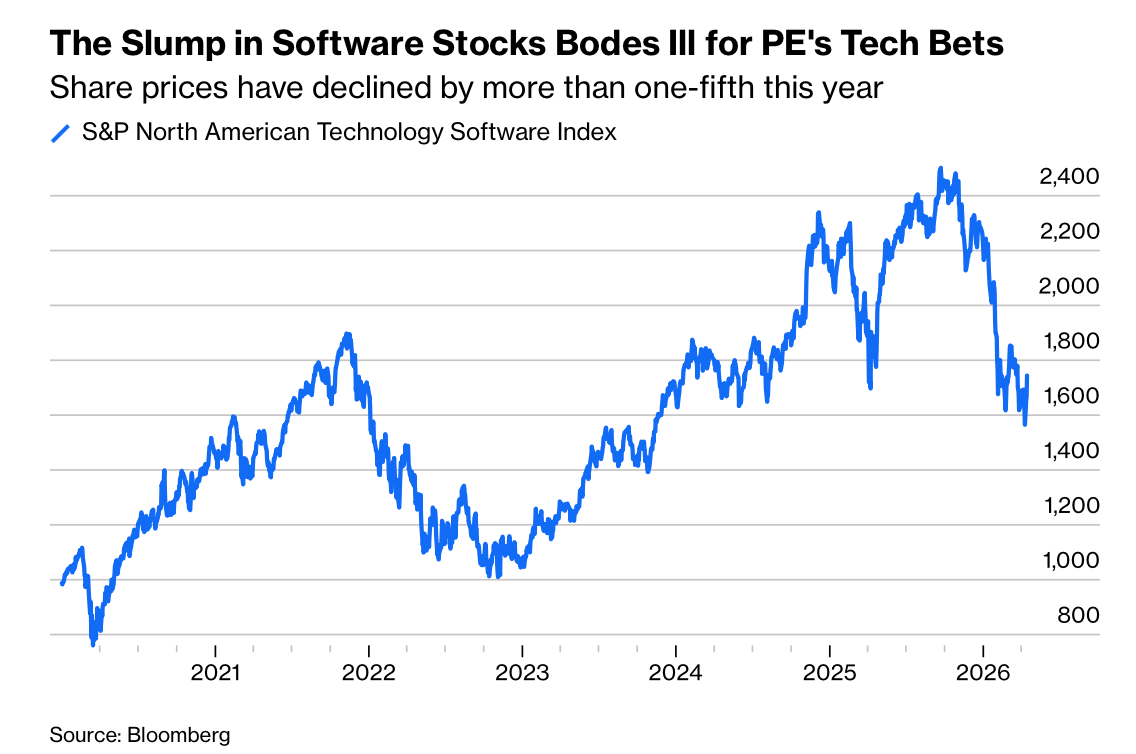

这种脆弱性在 2020–2021 年就已形成。软件在 buyout 交易中的占比接近三分之一,许多基金在约一年内就投出大部分现金。其背景是多年低利率和居家办公繁荣。2022 年 11 月,OpenAI 推出 ChatGPT 后加上加息,浮动利率债务对利润薄的 PE 所有企业成本明显上升。即使在 AI 冲击前,退出节奏也已放缓:Bain 显示平均持有期已由约五年延长至约七年,导致投资期限约十年的 LP 可利用的短期退出通道更少。

PE 越来越多地转向以举债支付分红和 continuation structure 延迟现金分配,但这提高了杠杆风险。若企业无法出售,就需要再融资;贷款人可能收紧条款,管理人不得不再注入资本,否则可能失去控制权。Medallia 是典型案例:该公司于 2021 年被 Thoma Bravo 以 64 亿美元收购,如果贷款人接管,Thoma Bravo 与共同投资者可能承受约 50 亿美元的 equity 损失。关联的 178 亿美元基金净 IRR 仅 6.2%,位列 2020 年这一 vintage 的最低四分位;即便该集团去年又募集 344 亿美元,若退出价格持续偏弱,其募资吸引力仍可能下滑。

Private credit is not as safe as its legal protections imply for the 2020–2021 software buyout vintage. In a typical deal, PE contributes over half the purchase price as equity and private credit provides debt, so lenders are usually hit only after value falls about 60%–70%. AI disruption led by Anthropic and peers is now weakening software pricing power, so that equity cushion may fail. Doug Ostrover of Blue Owl said that if direct lending is worrying, PE is even more so. Even with stronger covenants, fewer lenders, and generally better enforceability than broadly syndicated loans, private credit can still be harmed when valuation repricing is abrupt.

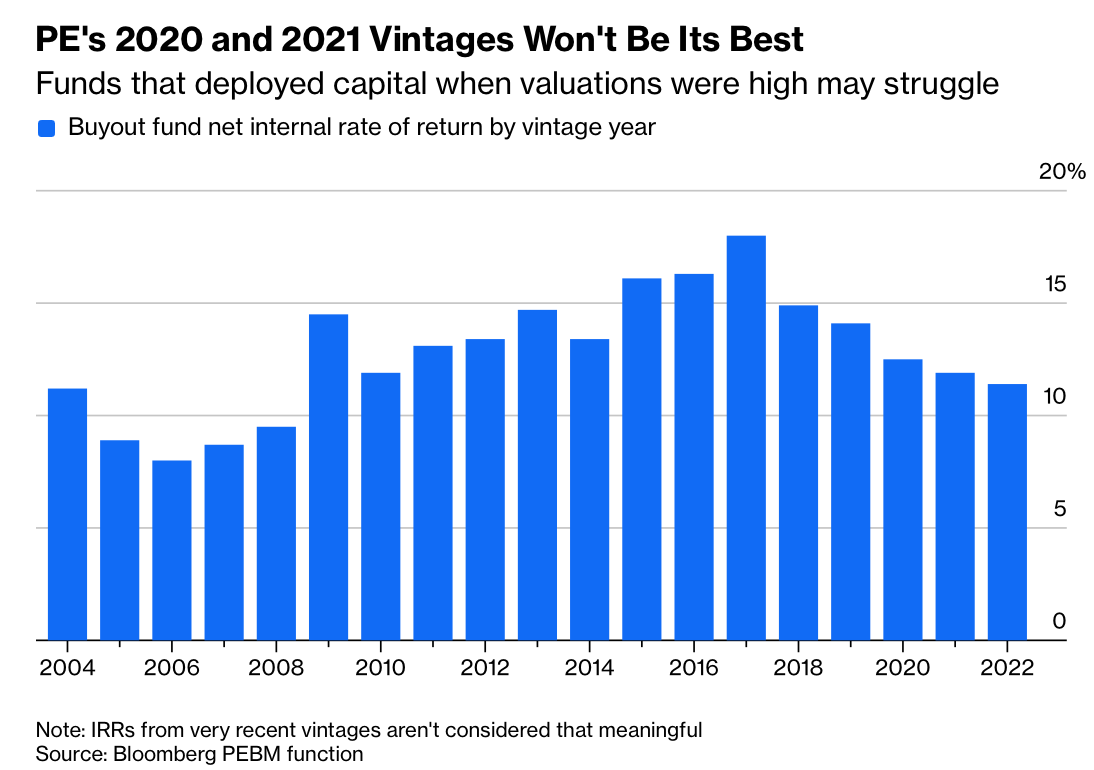

The vulnerability was seeded in 2020–2021. Software reached nearly one-third of buyout deals, and many funds deployed most of their cash in about one year. The backdrop was years of low rates and the work-from-home boom. In November 2022, OpenAI launched ChatGPT, and rate hikes followed, making floating-rate debt much more expensive for PE-owned firms with narrow margins. Even before the AI shock, exit timing had already slowed: Bain shows average holding periods rising from about five years to around seven, reducing near-term exit routes for LPs committed for roughly ten years.

PE has increasingly used debt-funded dividends and continuation structures to delay cash distributions, which raises leverage risk. If a company cannot be sold, refinancing becomes necessary; lenders may tighten terms, and sponsors may need to inject capital or lose control. Medallia shows the downside: it was bought by Thoma Bravo for $6.4 billion in 2021, and if lenders take over, Thoma Bravo and co-investors could face roughly $5 billion of equity impairment. A linked $17.8 billion fund has a 6.2% net IRR, in the lowest quartile for the 2020 vintage; even though the group raised $34.4 billion last year, fundraising strength may weaken if exit values stay depressed.