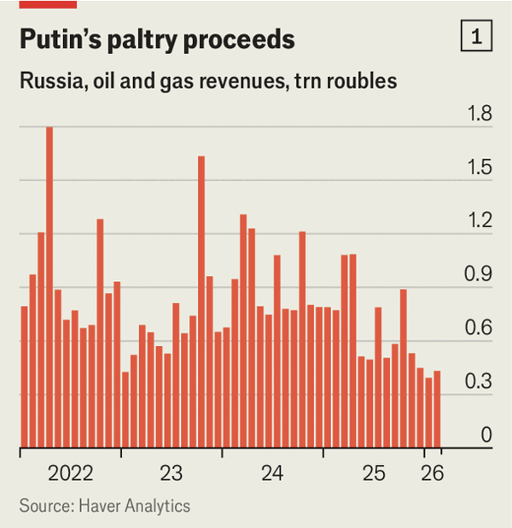

伊朗战争给俄罗斯能源部门带来了急剧的短期逆转。霍尔木兹海峡事实性关闭困住了全球约 15% 的石油供应,使布伦特原油价格从 12 月触及的 5 年低点每桶 59 美元升至如今约 100 美元。此前到 2 月,俄罗斯出口量已下降五分之一,油气收入同比下跌 44%,而仅前 2 个月预算赤字就达到 3.4 万亿卢布,相当于 2026 年全年目标的十分之九。如今高油价和美国豁免正在迅速改善这一局面。

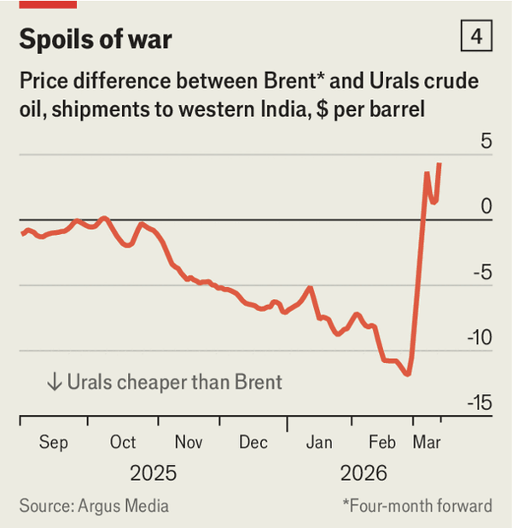

最直接的收益来自积压库存的释放和定价权改善。印度已将俄罗斯原油购买量提高约一半,帮助把俄罗斯海上库存削减逾 10%,至 1.22 亿桶;中国进口也在上升。俄罗斯原油因与中东原油品质相近而更受亚洲炼厂欢迎,如今运抵印度的 Urals 甚至相对布伦特出现溢价。按估算,布伦特价格若在一个月内每上涨 10 美元,俄罗斯能源出口将增加 28 亿美元,其中约 16 亿美元流入克里姆林宫。中国还可能因天然气安全焦虑而更认真考虑 2600 公里的 Power of Siberia 2 管道项目。

但这更像“糖分刺激”而非结构性逆转。分析师认为,俄罗斯仅有每日 30 万桶闲置产能,不足以替代海湾缺失的每日 1000 万至 1500 万桶供应;其石油企业还面临乌克兰打击、制裁和投资不足。即使高油价持续,若布伦特升破每桶 150 美元,需求破坏和能源转型可能反噬收益。最终,高油价和更宽松制裁最多只能修复自 2022 年以来损害的约 20%,却无法阻止俄罗斯石油产量以每年 3% 的速度下滑。

The Iran war has delivered a sharp short-term reversal for Russia’s energy sector. The de facto closure of the Strait of Hormuz has trapped about 15% of global oil supply, lifting Brent from its December five-year low of $59 a barrel to around $100 now. Before that, by February, Russian export volumes had fallen by one-fifth, oil-and-gas revenues were down 44% year on year, and in just the first 2 months the budget deficit reached 3.4trn roubles, nine-tenths of the full-year 2026 target. High prices and American waivers are now rapidly improving that picture.

The most immediate gain comes from clearing backlogged cargoes and improving pricing power. India has raised purchases of Russian crude by roughly one-half, helping cut Russia’s oil on water by over 10%, to 122m barrels; Chinese imports are also rising. Russian crude is attractive to Asian refiners because it resembles Middle Eastern grades, and Urals delivered to India now trades at a premium to Brent. Estimates suggest that every $10 rise in Brent sustained for a month adds $2.8bn to Russia’s energy exports, of which about $1.6bn reaches the Kremlin. China may also take gas security more seriously and reconsider the 2,600km Power of Siberia 2 pipeline.

But this looks more like a sugar high than a structural turnaround. Analysts reckon Russia has only 300,000 barrels a day of spare capacity, far too little to replace the Gulf’s missing 10m-15m b/d, while its oil firms still face Ukrainian strikes, sanctions and underinvestment. Even if high prices persist, Brent above $150 could trigger demand destruction and accelerate the shift away from petroleum. In the end, higher prices and softer sanctions may undo only about 20% of the damage since 2022, while failing to stop Russian oil output from shrinking by 3% a year.