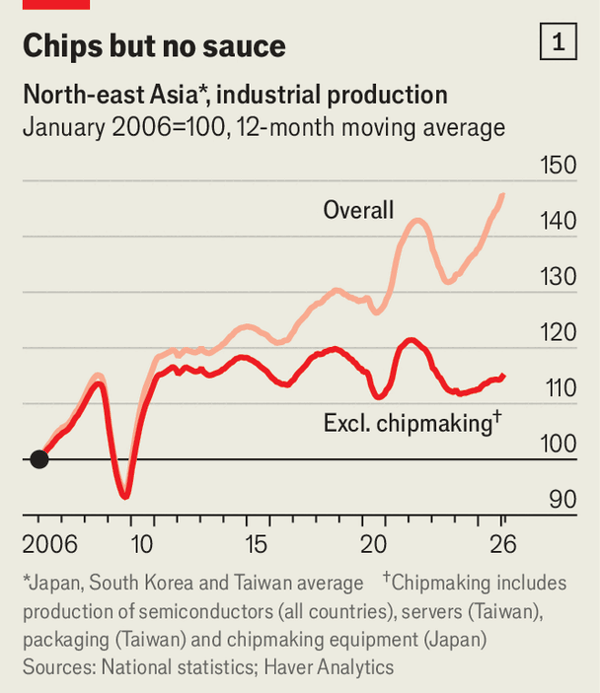

东北亚表面上处于出口热潮:台湾经济增长14%,远高于通常良年3-4%的预期,实际出口去年增长逾40%;韩国大企业营业利润增长159%,日本疫情以来出口增速为其经济增速的四倍。 但热潮高度集中于AI和半导体:剔除半导体和AI服务器后,台湾出口自2022年以来实际下降40%,韩国非AI出口停滞,日本非AI工厂产出萎缩,同时中国在汽车、化工和电池等领域施压,日本化工产出自2019年以来收缩四分之一,韩国自2022年以来收缩五分之一。

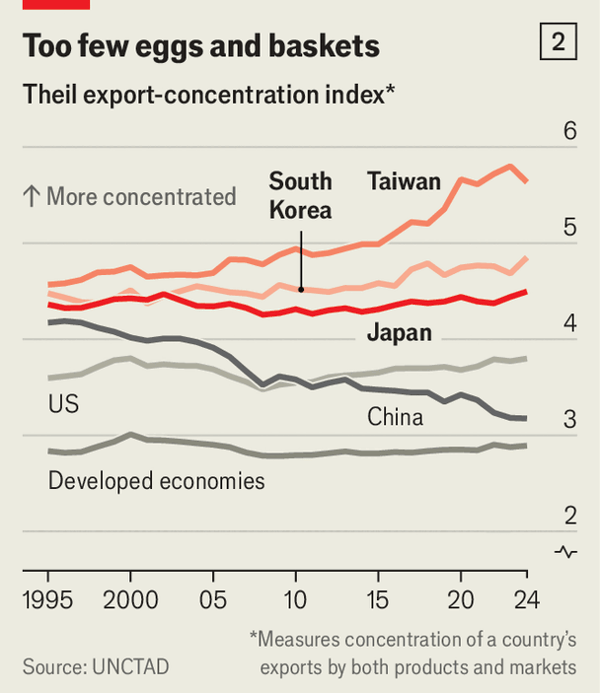

这种狭窄化正在加深:芯片和其他AI相关设备占韩国出口逾40%,为两年前的两倍多;在台湾占80%,高于疫情前约一半,而《经济学人》估算,自2019年以来该地区工业产出15%的全部增长都来自AI。 对出口和少数买家的依赖也在上升:自2019年以来三国出口占GDP比率平均提高9个百分点,台湾达73%、韩国46%、日本2024年达创纪录的22%;2025年AI相关科技出口贡献台湾和韩国总体增长约四分之三,该地区出口集中度比富裕国家平均水平高73%,台湾三分之二以芯片为主的海外销售流向美国和中国。

内部缓冲很弱,因为家庭消费偏低且收入分化严重:私人消费占日本产出的53%,韩国和台湾接近40%,低于富国60%的平均水平,日本过去十年消费仅贡献增长的3%,而政府支出贡献58%。 小企业雇用韩国60%、日本70%、台湾80%的劳动力,非正规工人在韩国收入仅为正规工人的一半、在日本低40%;养老金支出在台湾和韩国仅占GDP的5%和4%,约为经合组织平均的一半,老年相对贫困率在日本、韩国和台湾约为20%、40%和30%,使该地区对AI出口、半导体周期以及美国和中国需求的押注风险很高。

North-east Asia appears to be in an export boom: Taiwan is growing at 14%, far above the 3-4% expected in a normal good year, with real exports up over 40% last year; South Korea’s big-firm operating profits rose 159%, and Japan’s exports have grown four times as fast as its economy since the pandemic. But the boom is highly concentrated in AI and semiconductors: excluding semiconductors and AI servers, Taiwan’s exports have actually fallen 40% since 2022, South Korea’s non-AI exports have stagnated, and Japan’s non-AI factory output has shrunk, while China is pressuring cars, chemicals, and batteries, with chemical output down by a quarter in Japan since 2019 and by a fifth in South Korea since 2022.

This narrowing is intensifying: chips and other AI-related gear make up over 40% of South Korean exports, more than double their share two years ago, and 80% of Taiwan’s, up from about half before the pandemic, while The Economist estimates that all of the region’s 15% rise in industrial output since 2019 came from AI. Dependence on exports and on a few buyers is also rising: since 2019 the export-to-GDP ratio has increased by an average of nine percentage points across the three countries, reaching 73% in Taiwan, 46% in South Korea, and a record 22% in Japan in 2024; AI-related tech exports supplied about three-quarters of overall growth in Taiwan and South Korea in 2025, the region’s exports are 73% more concentrated than the rich-world average, and two-thirds of Taiwan’s chip-heavy foreign sales go to America and China.

The internal buffer is weak because household consumption is low and income is sharply divided: private consumption is 53% of output in Japan and closer to 40% in South Korea and Taiwan, below the rich-country average of 60%, while consumption provided only 3% of Japan’s growth over the past decade, versus 58% from government spending. Small firms employ 60% of workers in South Korea, 70% in Japan, and 80% in Taiwan, irregular workers earn only half as much as regular workers in South Korea and 40% less in Japan, pension spending is just 5% and 4% of GDP in Taiwan and South Korea, about half the OECD average, and relative elderly poverty is about 20%, 40%, and 30% in Japan, South Korea, and Taiwan, leaving the region’s bet on AI exports, semiconductor cycles, and American and Chinese demand highly risky.

Source: Japan, South Korea and Taiwan are suffering industrial rot

Subtitle: Artificial intelligence is concealing a China shock

Dateline: 5月 28, 2026 03:25 上午 | SEOUL, TAIPEI and TOKYO