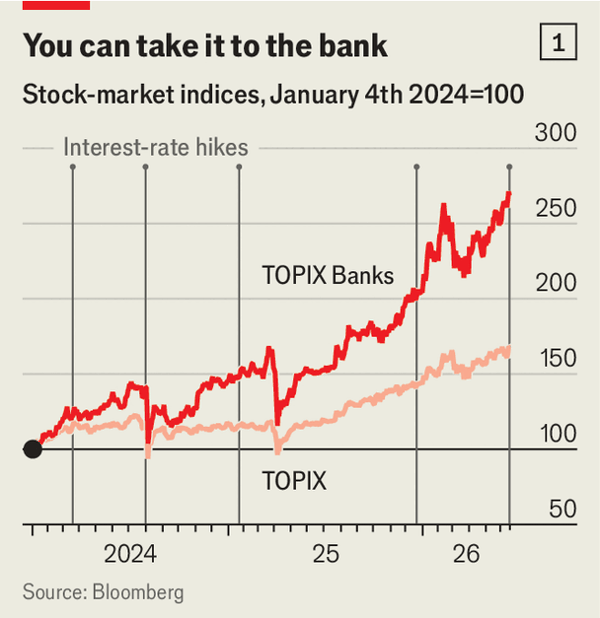

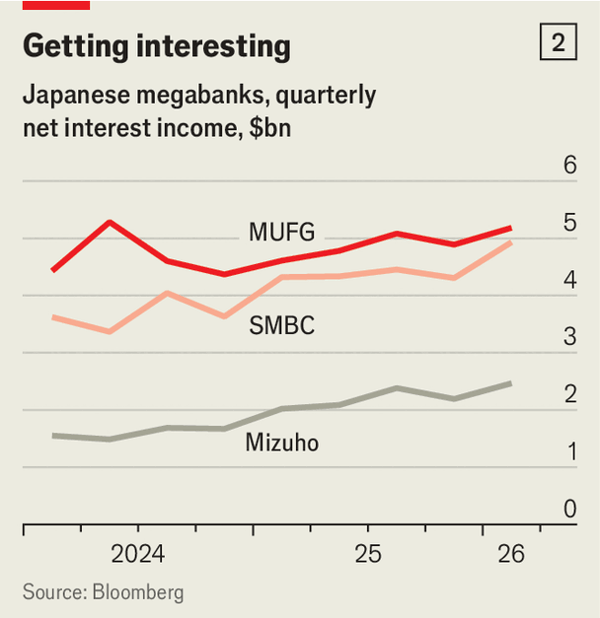

日本银行将基准利率上调至1%的决定标志着零利率时代的结束,自2024年3月以来推动日本银行股指翻了一番以上。这一变化使短期和长期利率之间的差距扩大到1.6个百分点,从而使大型贷款机构的净息差受益。

然而,小银行难以跟上步伐,自2022年以来区域性银行的存款增长率仅为6%,而大型竞争对手的增长率则为17%。较小的金融机构面临着巨大的财务压力,因为日元债券损失在区域性银行约占风险加权资产的2%,在约250家信用金库中占4%。

为了掩盖这些脆弱性,记为持有至到期的长期政府债券比例从2019年的零上升到2025年的近一半。尽管这些区域性贷款机构目前持有充足的资本缓冲,但持续的人口减少可能会加速它们的合并。

The Bank of Japan's decision to raise its benchmark interest rate to 1% marks the end of zero rates, boosting the share index of Japanese banks by over 100% since March 2024. This change has widened the gap between short-term and long-term rates to 1.6 percentage points, benefiting the net interest margins of large lenders.

However, small banks struggle to keep pace, with regional banks seeing deposit growth of just 6% since 2022 compared to 17% for mega-banks. Smaller institutions face significant financial pressure, as yen bond losses account for about 2% of risk-weighted assets at regional banks and 4% at the 250 shinkin community banks.

To obscure these vulnerabilities, the share of long-dated government bonds marked as held-to-maturity rose from zero in 2019 to nearly half in 2025. Although these regional lenders currently hold sufficient capital buffers, the ongoing population decline will likely accelerate their consolidation.

Source: A new golden age for Japanese banks comes with a catch

Subtitle: Smaller lenders are saddled with low-return bonds they cannot sell

Dateline: 6月 18, 2026 03:16 上午 | Singapore