工党在5月7日地方选举中惨败后,触发了两场关键较量:一场是接替基尔·斯塔默出任首相的党内争夺,另一场是领导人候选人与债券市场之间的博弈。10年期英国国债收益率在5月11日至12日单日就上升了近0.2个百分点,显示市场对激进财政言论反应迅速。

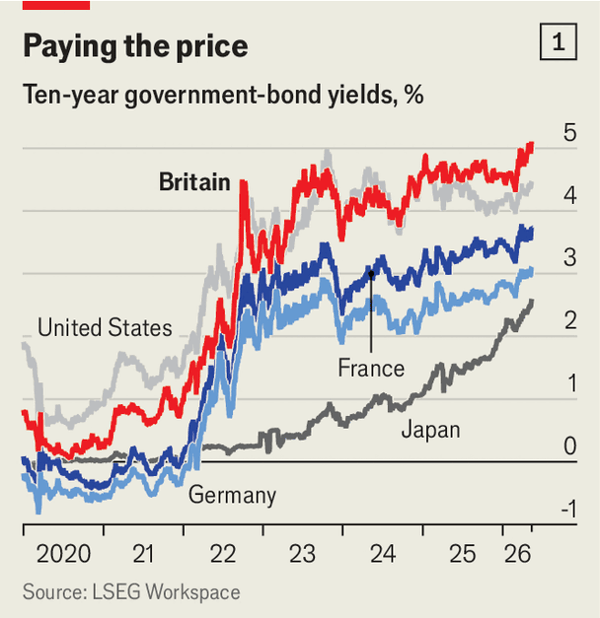

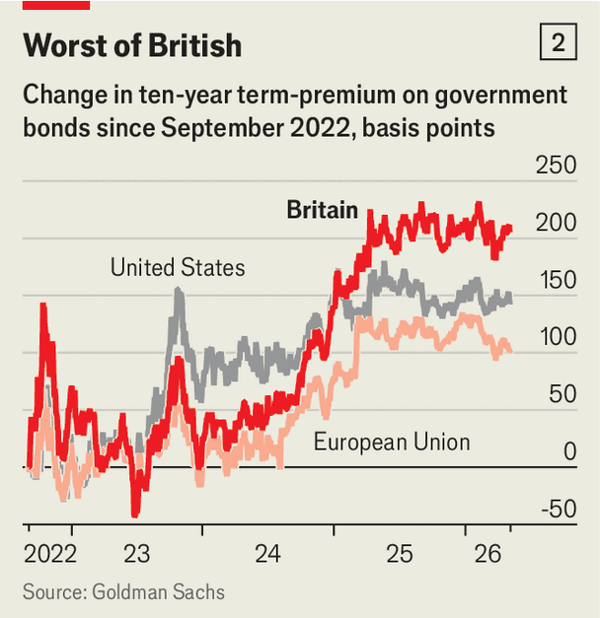

自伊朗战争爆发以来,10年期英债收益率从4.2%飙升至4月下旬的5.2%高点,英国仍是七国集团中借贷成本最高的国家,且涨幅约为德国的两倍。英国通胀在2月仍达3%,高于欧元区的1.9%,高盛估计英国10年期期限国债自2022年以来上升了超过2个百分点,而欧盟仅约1个百分点。

英国债务压力还来自债券市场结构变化:国内养老金买盘减少,海外投资者接盘,而英国央行继续出售量化宽松时期积累的国债,加剧供给压力。英国财政前景也不稳,IFS估计若按当前收益率计入下一次预算,2029-30年债务利息将比3月预估高约70亿英镑,约相当于所得税上调1便士。

Labour’s drubbing in the local elections on May 7th has started two crucial contests: the scramble to replace Sir Keir Starmer as prime minister, and the fight between leadership hopefuls and the bond market. Ten-year gilt yields rose by nearly 0.2 percentage points on May 11th-12th alone, showing how quickly markets react to loose talk.

Since the Iran war began, ten-year gilt yields have jumped from 4.2% to a late-April high of 5.2%, leaving Britain with the highest borrowing costs in the G7 and a rise about twice Germany’s. Inflation was still 3% in February, versus 1.9% in the euro zone, and Goldman Sachs estimates that Britain’s ten-year term premium has risen by more than two percentage points since 2022, compared with about one point in the EU.

Britain’s debt pressure also reflects market structure: domestic pension funds have bought fewer gilts, overseas investors have replaced them, and the Bank of England’s continued sales of QE-era holdings have added supply. The Institute for Fiscal Studies says that if current yields were built into the next budget, debt-servicing costs in 2029-30 would be about £7bn higher than thought in March, roughly equivalent to a 1p rise in income tax.

Source: Bond-market lessons for Labour’s leadership hopefuls

Subtitle: The gilt market cannot be tamed, only respected

Dateline: 5月 14, 2026 11:25 上午