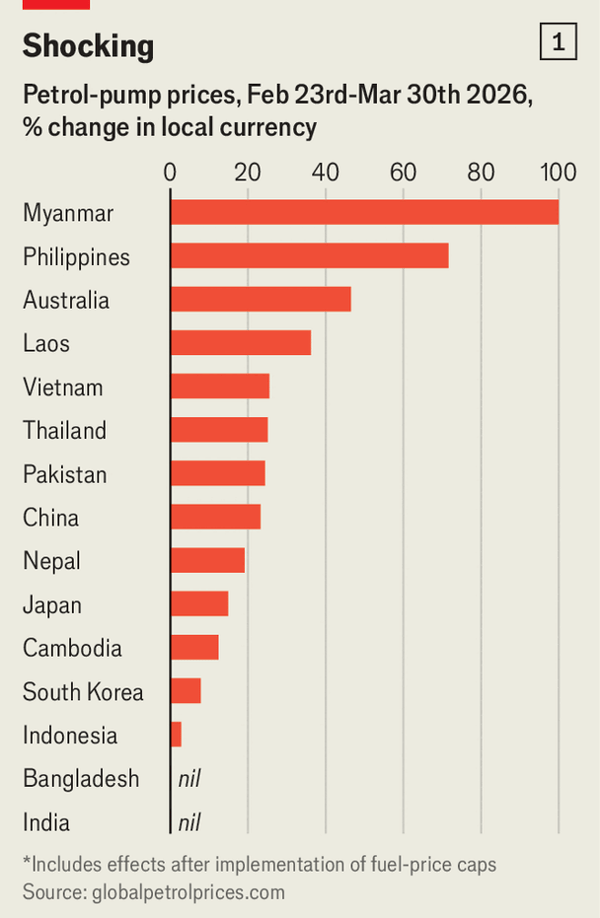

这场战争对亚洲的冲击可量化为“输油与输气依赖风险”:霍尔木兹海峡约80%的油和90%的天然气通常流向亚洲;菲律宾超过90%的能源进口来自中东,孟加拉国、印度和巴基斯坦的液化天然气供应中接近三分之二也依赖该航道。全球汽油价格自战争爆发后上升14%,东南亚高达42%,菲律宾和缅甸超过70%,在此背景下印尼可能因燃油补贴使财政赤字超出GDP的3%上限,巴基斯坦已上调油价20%,印度、孟加拉国、越南、澳大利亚和韩国通过减税或设定上限吸收成本,脆弱货币经济体则面临投机压力上升。

通胀压力几乎无法避免:未能由政府吸收的高能耗会直接推高总通胀,且即便有油价上限的国家也会因化工、物流等供应链成本上升而被传导。战争已卷入约三分之一的全球海运化肥贸易,导致亚洲发展银行将原本预计2026年只升2.1%的通胀修订为可能超过5%,若冲突持续,东南亚增速下滑风险为2.3个百分点,南亚为0.8个百分点。

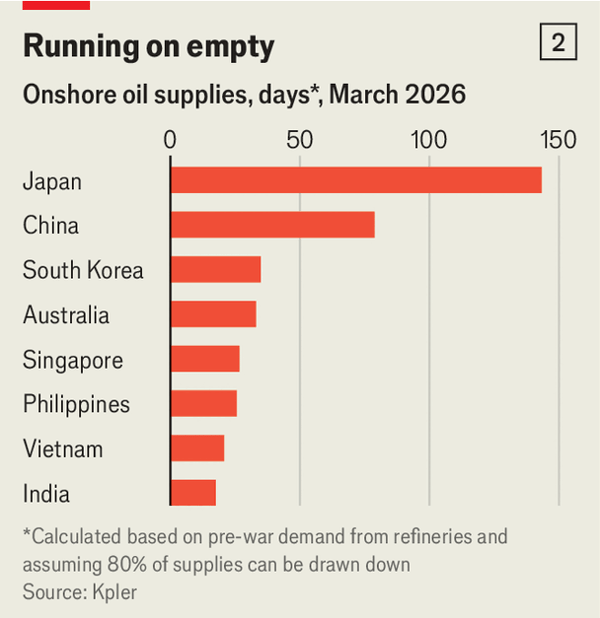

燃油储备与供应能力差异进一步放大风险:日本有254天、 中国有100天的油储,但菲律宾、越南、泰国仅约能覆盖三周正常需求,航空业已出现半数全球取消航班源自亚洲机场的局面,纽西兰航空取消1,100次航班,运输和旅游最先承压。各国正在同步推进“低碳+补煤”战略:更多太阳能、更多电动车、越南推进俄建核电站,同时印度重启古吉拉特一座燃煤电厂;能源价格与社会稳定的耦合也在加强,菲律宾已有交通部门示威,研究显示食品与能源相关抗议在南亚约占历史样本的四分之一,斯里兰卡2022年的“油价驱动”动荡提示能源冲击可能演化为政治冲击。

The article treats the war as an Asian energy shock: about 80% of oil and 90% of gas passing through the Strait of Hormuz typically head to Asia, with the Philippines receiving over 90% of energy imports from the Middle East and Bangladesh, India, and Pakistan getting around two-thirds of LNG via the strait. Petrol prices have risen 14% globally since the war, 42% in Southeast Asia, and over 70% in the Philippines and Myanmar, while India, Bangladesh, Vietnam, Australia, and South Korea are using tax cuts or price caps to absorb costs; Indonesia faces a possible breach of its 3% of GDP fiscal-deficit cap, Pakistan has already raised fuel prices by 20%, and fragile-currency economies are more exposed to speculative pressure.

Inflation is largely unavoidable: where governments do not absorb higher crude costs, headline inflation rises, and even in capped markets, pass-through occurs through chemicals, logistics, and other supply-chain costs. The war now envelops roughly one-third of global seaborne fertilizer trade, prompting the ADB to revise its Asia inflation outlook for 2026 from 2.1% to potentially above 5%, and prolonged conflict could trim growth by up to 2.3 percentage points in Southeast Asia and 0.8 points in South Asia.

Reserve depth and sectoral exposure then become the next layer of risk: Japan holds 254 days of oil reserves and China 100 days, while the Philippines, Vietnam, and Thailand have onshore supplies for only about three weeks of normal demand, and aviation has already been hit with about half of global flight cancellations originating in Asia plus 1,100 Air New Zealand cancellations. Governments are pursuing both clean-energy acceleration and a coal fallback—more solar, more EVs, Vietnam’s nuclear plan with Russia, and India’s restart of a Gujarat coal plant—while social-political risk rises as transport protests spread in the Philippines and historical evidence links fuel-price hikes to unrest, with a cited quarter-share of recent South Asian protests and Sri Lanka’s 2022 turmoil as a warning that this energy shock can become a political one.

Source: How the Gulf’s war is becoming Asia’s crisis too

Subtitle: Prices, debt, and scarcity will strike a blow against the world’s workshop

Dateline: 4月 01, 2026 06:04 上午 | DELHI, MELBOURNE, SINGAPORE AND TOKYO