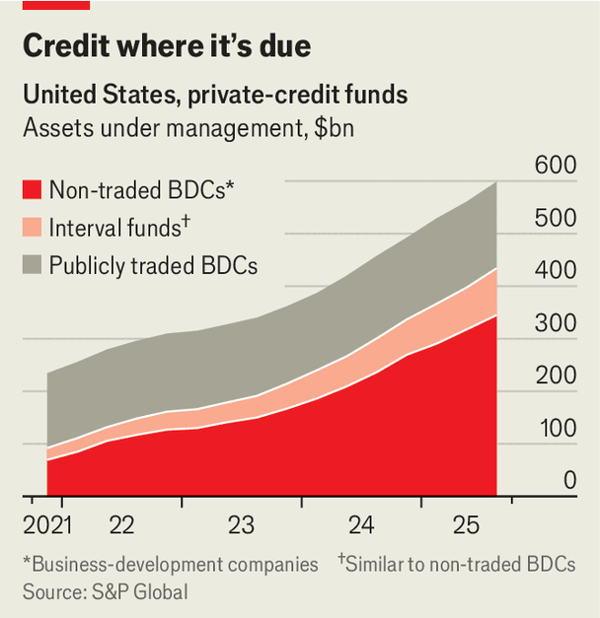

Buttonwood 以 10 亿美元收购 Main Road 的交易展现了当前杠杆收购范式:约 5 亿美元来自其最新私募基金、已被投资者锁定十年的资金,约 5 亿美元来自借来的杠杆。金融危机后银行风险约束收紧后,风险偏好转向私募信贷,相关市场规模已接近杠杆贷款(1.4 万亿美元)和垃圾债(1.5 万亿美元)的规模,BDC 等相关载体资产也从 2021 年底的 2300 亿美元增长到近 6000 亿美元。

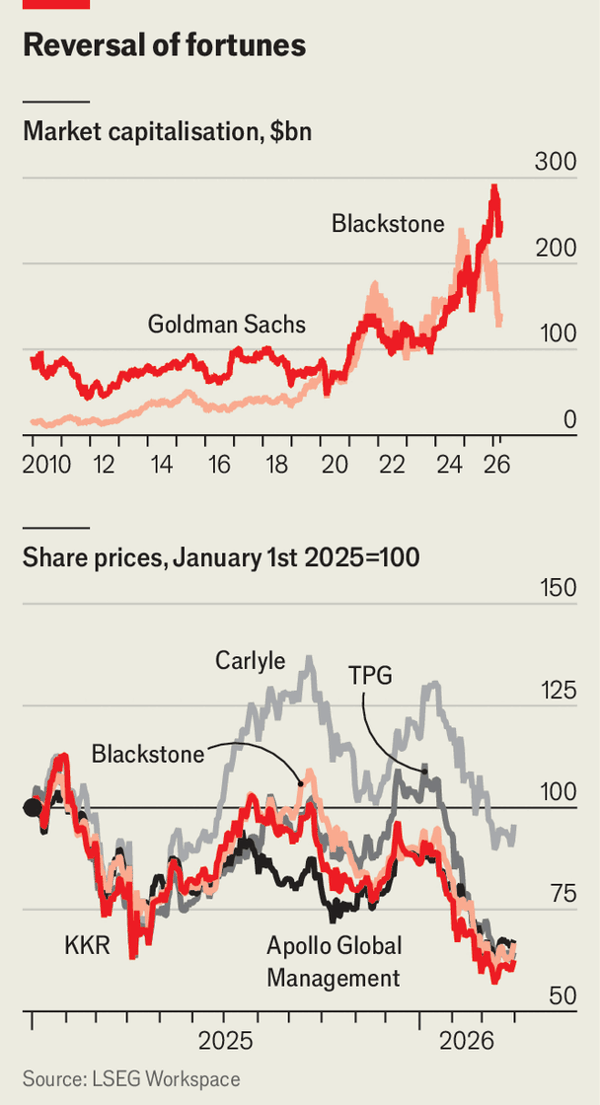

公共与私营 BDC 同时面临赎回压力,公共 BDC 的中位折价从年初的 16% 扩大到目前 25%,而一年前几乎无折价。私募 BDC 更受到季度 5% 赎回上限的挤压,Ares、Apollo 和 BlackRock 分别遭遇 11.6%、11.2% 和 9.3% 的赎回请求,Blackstone 旗下管理 830 亿美元资产的基金本季以注入 1.5 亿美元后仍赎回 7.9%,Blue Owl 在一月允许逾 15% 赎回后,4 月 2 日又对两只基金将上限降为 5%,因为请求分别达 40.7% 与 21.9%,其股价自去年高点下跌三分之二。

软件并购链上压力也在上升:2019—2022 年并购规模最大的 25 起上市软件交易平均为目标公司营收的 9 倍,但当下美国上市软件公司的中位估值仅为营收的 3 倍。被私募信贷持有的此类软件公司平均负债约为年收益的 8 倍,且一半现金流为负,叠加银行与保险渠道传导使风险上行;联邦储备估计截至 2024 年底银行对 BDC 的承诺贷款为 870 亿美元,寿险端通过担保贷款相关资产占比为 4%(某机构高达 18%),且去年新增评级票据与基金债务证券分别超过 170 亿和 260 亿美元,同时开曼群岛再保险资产从 2020 年的 230 亿美元升至 1010 亿美元。

Buttonwood’s $1 billion purchase of Main Road is the current leveraged-buyout model: about $500 million in private-fund capital locked up for ten years, and about $500 million in borrowed private credit. As post-crisis bank risk limits tightened, private credit has moved closer to the core of buyout finance, reaching near the scale of leveraged loans ($1.4 trillion) and high-yield bonds ($1.5 trillion), while BDC and related vehicles have expanded from $230 billion at the end of 2021 to nearly $600 billion.

Both public and private BDCs are under redemption pressure, with public BDCs now trading at a median 25% discount to NAV versus 16% at the start of the year and near zero a year ago. Private BDCs face redemption requests well above a 5% quarterly cap—Ares, Apollo and BlackRock reported 11.6%, 11.2% and 9.3%; Blackstone’s $83 billion BDC redeemed 7.9% after injecting $150 million, while Blue Owl allowed over 15% redemption in January and then capped two funds at 5% after requests of 40.7% and 21.9%, during which its shares fell by two-thirds from last year’s peak.

Credit stress now appears deeper in the buyout pipeline: the 25 largest public software buyouts from 2019 to 2022 were priced at nine times target revenue, while the current median listed software valuation is three times revenue. Software borrowers held by private-credit funds now carry debt around eight times annual earnings, with half in negative cash flow, and the transmission chain is amplified through banks and insurers; the Federal Reserve estimated banks had committed $87 billion in lending to BDCs by end-2024, insurers show private-loan exposures via CLOs at 4% of life-insurer assets (18% at one firm), with new rated-note and collateralized-fund obligations above $17 billion and $26 billion, while Cayman reinsurance assets rose from $23 billion in 2020 to $101 billion.

Source: A guide to the private-credit crisis

Subtitle: Why some panicky investors are running for the exit

Dateline: 4月 02, 2026 05:02 上午 | New York