能源冲击的核心风险在于政策误判与全球再分配。若美国禁止原油出口,将困住每日 400 万桶原油,相当于全球海运流量的 9%,并可能把美国汽油价格从 2 月 27 日的每加仑 2.90 美元推高到接近 4 美元,若 Brent 在 3 月底升至 120 美元则可能到 4.50 美元。仅禁止成品油出口也会冲击美国每日 270 万桶燃料出口所服务的拉丁美洲与欧洲。短期内,中西部和墨西哥湾沿岸可能受益,但东海岸与太平洋沿岸因依赖外来供应,价格仍会扭曲性高企。

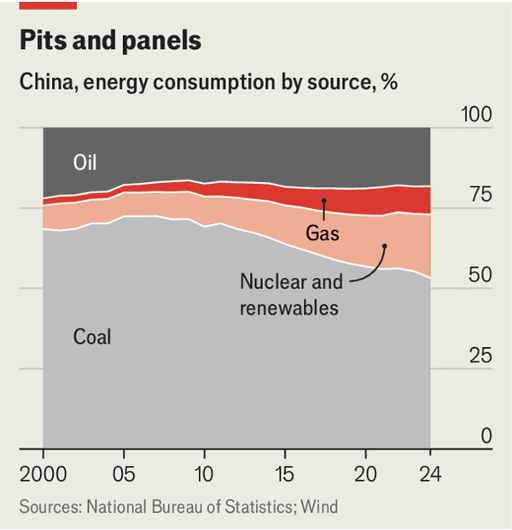

中国虽有缓冲,但无法免疫。石油仍提供其总能源的 18% 以上,而进口油满足其约 13% 至 14% 的能源需求,其中超过一半来自中东。霍尔木兹海峡战前每天承载约 1500 万桶原油,如今大幅受阻;不过本月仍有约每日 130 万至 140 万桶伊朗原油通过,约为战前的 90%,大多流向中国。中国还拥有约可覆盖 120 天进口需求的库存,并按 2016 年公式缓慢传导国际油价;3 月 9 日汽油价格上限上调每吨 695 元,在广东对应上涨 7.8%,而香港价格仍高出近 50%。

但缓冲只能减震,不能消除损失。若油价今年平均仅为每桶 85 美元,Shenwan Hongyuan 估计中国工业生产增速也会被削去 0.3 个百分点;Goldman Sachs 已把中国 GDP 增长预测下调 0.1 个百分点至 4.7%。比较之下,印度、东南亚和日本分别被下调 0.5、0.4 和 0.3 个百分点。整体趋势是,出口禁令会在美国内外制造更大价格错配,而中国的储备、管制和炼油灵活性只能把全球能源冲击从剧痛降为持续钝痛。

The core risk in the energy shock is policy miscalculation and global redistribution. If America banned crude exports, it would trap 4m barrels a day, equal to 9% of global seaborne flows, and could push American petrol from $2.90 a gallon on February 27th to nearly $4, and toward $4.50 if Brent reaches $120 by end-March. A product-export ban alone would also hit Latin America and Europe, which depend on America’s 2.7m b/d of fuel exports. In the short run, the Midwest and Gulf coast might benefit, but the east and Pacific coasts, which rely on outside supply, would still face distorted high prices.

China has buffers, but not immunity. Oil still provides more than 18% of its total energy, and imported crude covers about 13%-14% of its energy needs, with more than half coming from the Middle East. Before the war, roughly 15m barrels a day passed through Hormuz; now flows are badly snarled. Even so, about 1.3m-1.4m b/d of Iranian crude has still passed this month, around 90% of the pre-war level, mostly to China. China also has stocks covering about 120 days of import demand and uses a 2016 pricing formula to pass through global oil rises gradually; on March 9th petrol caps were raised by 695 yuan per tonne, implying a 7.8% rise in Guangdong, while Hong Kong prices remain almost 50% higher.

But buffers can only dampen, not erase, the damage. If oil averages only $85 a barrel this year, Shenwan Hongyuan estimates China’s industrial-production growth would still be cut by 0.3 percentage points; Goldman Sachs has already lowered China’s GDP-growth forecast by 0.1 points to 4.7%. By comparison, India, South-East Asia and Japan were cut by 0.5, 0.4 and 0.3 points. The broader pattern is that export bans would create larger price distortions at home and abroad, while China’s reserves, controls and refining flexibility can only turn a global energy shock from acute pain into prolonged dull pain.