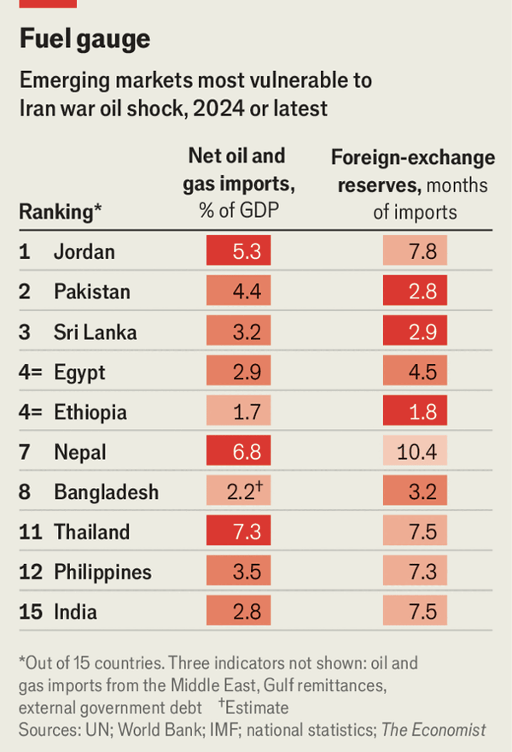

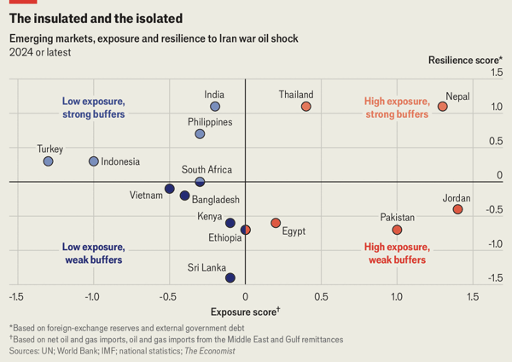

在新一轮能源冲击中,最脆弱的不是单纯高进口国,而是“高暴露、低缓冲”国家。文章用两个维度排序:对进口能源和海湾资金流的依赖,以及吸收冲击的金融缓冲。结果显示,Jordan、Pakistan 和 Egypt 风险最高。Pakistan 的油气进口支出约占 GDP 的 4%,近 90% 来自中东;Egypt 约占 3%,近一半来自该地区。两国还高度依赖海湾汇款,规模约占 GDP 的 5% 至 6%,一旦战争扰乱就业或迫使劳工回流,经常账户将同步恶化。

缓冲能力决定危机是否升级为国际收支危机。Pakistan 的外汇储备不足以覆盖 3 个月进口,低于 IMF 建议下限;Egypt 今年到期外债约 290 亿美元,超过其外汇储备的一半。Bangladesh 和 Sri Lanka 虽暴露度中等,但同样脆弱:Bangladesh 的储备也仅勉强覆盖 3 个月进口,且已在 IMF 项目中;Sri Lanka 则刚从 2022 年因上一轮能源冲击触发的违约中走出,缓冲仍薄弱。随着全球资金撤离新兴市场债券基金,更高燃料账单更容易触发融资压力。

也有高暴露但更能承压的国家。Thailand 的油气进口支出约占 GDP 的 7%,为样本中最高,但拥有接近 100 天战略石油储备和超过 7 个月进口覆盖。Nepal 来自海湾工人的汇款高达 GDP 的 8%,石油库存有限,却持有较多硬通货。India 的进口能源支出约占 GDP 的 3%,约一半来自中东,但其外储可覆盖约 7 个月进口,油储可维持约 70 天,还能转向俄罗斯低品质原油并更多依赖本地煤电。即使避免宏观危机,食品与化肥成本上升仍可能把 2026 年急性饥饿人数推至纪录高位。

The countries most at risk from the new energy shock are not simply the biggest importers, but those with both high exposure and weak buffers. The article ranks countries on two dimensions: dependence on imported energy and Gulf-linked inflows, and financial capacity to absorb the hit. Jordan, Pakistan and Egypt emerge as the most vulnerable. Pakistan spends about 4% of GDP on oil and gas imports, with nearly 90% sourced from the Middle East; Egypt spends about 3%, with nearly half from the region. Both also rely heavily on Gulf remittances worth around 5% to 6% of GDP, so war can worsen their current accounts from both sides.

Buffers determine whether stress becomes a balance-of-payments crisis. Pakistan’s reserves cover less than 3 months of imports, below the IMF’s recommended minimum; Egypt faces about $29bn in external debt due this year, more than half its foreign-exchange reserves. Bangladesh and Sri Lanka, though only moderately exposed, are also fragile: Bangladesh’s reserves barely cover 3 months of imports and it is already in an IMF programme; Sri Lanka has only recently emerged from its 2022 default, itself partly triggered by the last energy shock. As capital leaves emerging-market debt funds, higher fuel bills can more easily trigger financing stress.

Some highly exposed countries are better placed. Thailand spends about 7% of GDP on oil and gas imports, the highest in the sample, but has nearly 100 days of strategic oil reserves and more than 7 months of import cover. Nepal gets a striking 8% of GDP in remittances from Gulf workers and has little oil stored, yet holds substantial hard currency. India spends about 3% of GDP on imported energy, roughly half from the Middle East, but has reserves covering about 7 months of imports and oil stocks lasting around 70 days; it can also switch toward Russian crude and rely more on domestic coal. Even where macro crisis is avoided, rising food and fertiliser costs could still push acute hunger to record levels in 2026.