在通胀互换市场,1年期CPI互换的买入(receive)价格也大幅上升:约为2.9%,而一周前约为2.5%。Jon Hill、Gang Hu与Omair Sharif等人认为,油价传导至汽油会抬高短期CPI和短期预期;汽油对公众最具可感知性且在1月占美国CPI的2.9%。美国全国平均汽油零售价在3月5日约为3.32美元(周一3月1日约低于3美元)进一步施压,同时下周公布的2月CPI预期同比增长2.4%,与1月持平;更广泛通胀自2022年9.1%高点后,自2023年中以来一直低于4%。

尽管近期美国联储降息预期下降,交易员仍预期至少一次降息,且明显偏好短期:短期限期TIPS可望获得更高的通胀调整收益,并且市场预计美联储不会因暂时的能源冲击立即加息,短期实际利率可能下行。相比之下,30年期端点支撑较弱,30年期TIPS保值利率约2.22%,接近过去一年低位。Hu指出,油价长期上升可能因消费者对汽油支出增加而挤压其他支出,产生通缩效应;同时增长放缓导致税收下滑与军事支出上升可能扩大财政赤字,拉高长期端名义与实际利率,Phoebe White则称油价路径分布已明显上移。

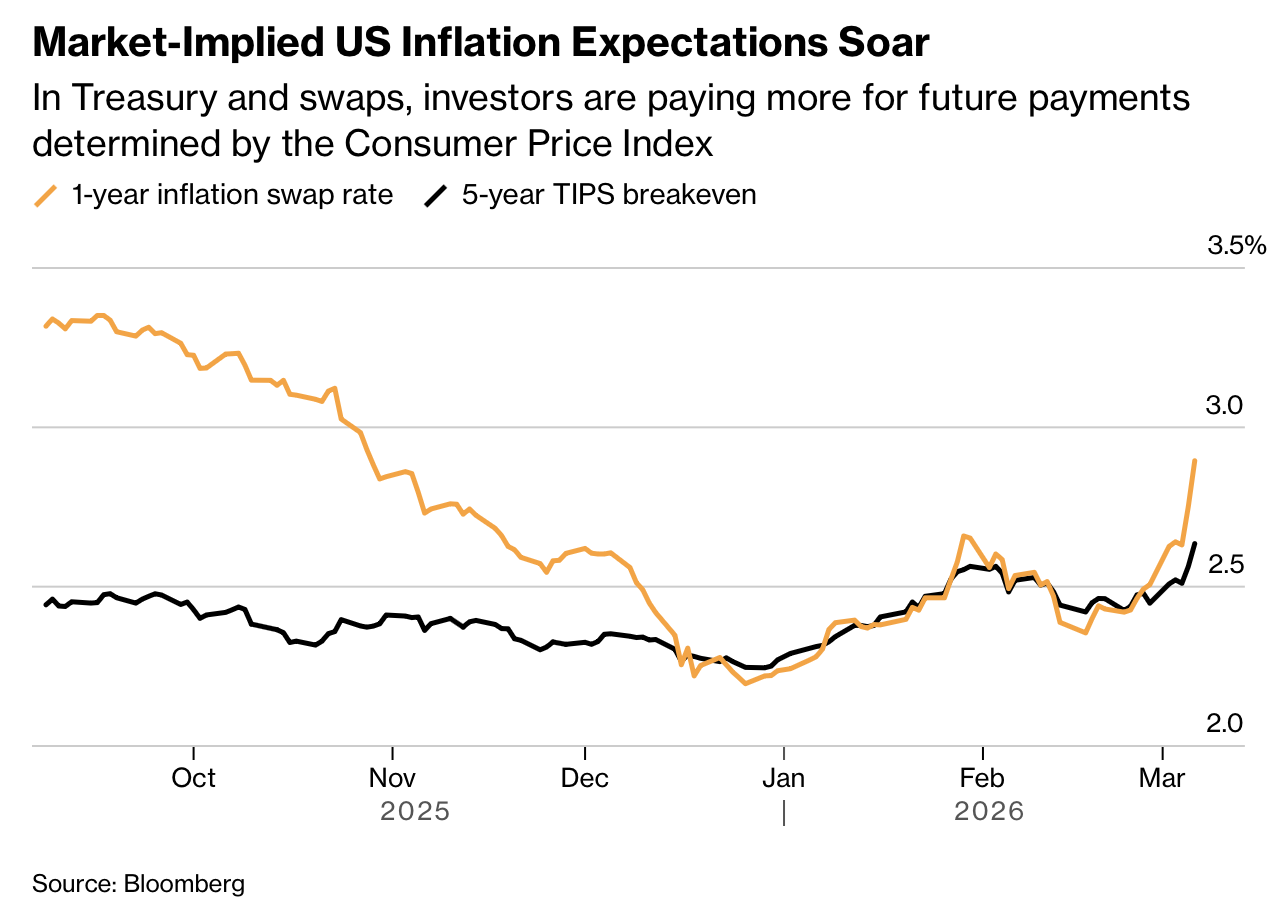

Bond traders moved aggressively into inflation hedges after U.S.–Israel strikes on Iran, followed by Iranian retaliation, pushed oil higher. In Treasury and inflation-swap markets tied to the U.S. Consumer Price Index, investors increased positioning because TIPS are attractive when inflation risk rises; their principal and coupon adjust with CPI. The five-year nominal Treasury yield sits near 3.7% versus 1.05% on five-year TIPS, a roughly 2.65 percentage-point breakeven gap now used as a proxy for expected inflation over the next five years. On Friday, unexpectedly weak February employment data pulled regular Treasury yields down, while benchmark U.S. oil futures reached their highest level since 2023, reinforcing demand for short-dated protection.

Inflation swaps also repriced: the one-year CPI swap receive rate is now around 2.9%, up from about 2.5% a week earlier. Jon Hill, Gang Hu, and Omair Sharif all stress that higher oil usually passes quickly into gasoline, lifting short-term CPI and expectations; gasoline is especially salient to households and contributed 2.9% to U.S. CPI in January. Gasoline prices added pressure as the U.S. national average retail price moved to about US$3.32 (from just under US$3 on March 1), while the February CPI expected next week is forecast at 2.4% year-over-year, unchanged from January. Broader inflation has remained below 4% since mid-2023 after peaking at 9.1% in 2022.

Although expectations for Federal Reserve easing this year have weakened, traders still price at least one cut. They remain concentrated in the front end: short-maturity TIPS can benefit from larger inflation-adjusted coupons, while short-term real rates are expected to decline if the Fed does not hike in response to a temporary oil shock. In contrast, long-end support is thinner: the 30-year breakeven is around 2.22%, near the low end of the past year. Hu notes that sustained high oil can become deflationary over time as higher gasoline spending crowds out other consumption, and Phoebe White adds that the distribution of possible oil paths has shifted materially higher. Weaker growth and increased military spending may also widen fiscal deficits, which should pressure long-end nominal and real yields higher.