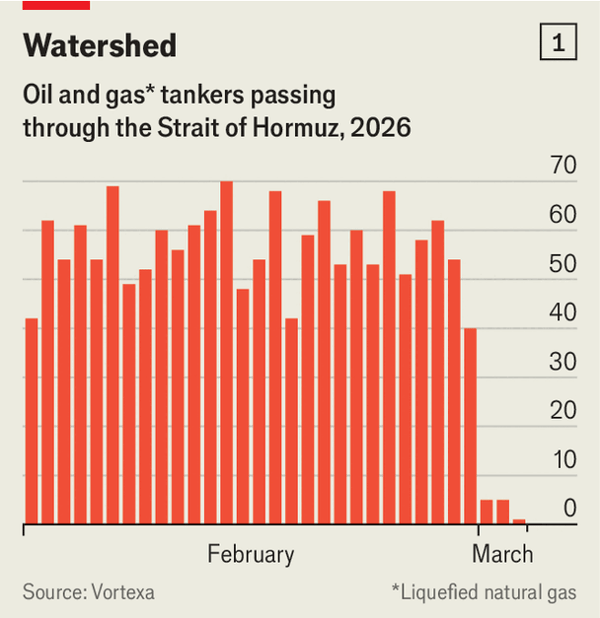

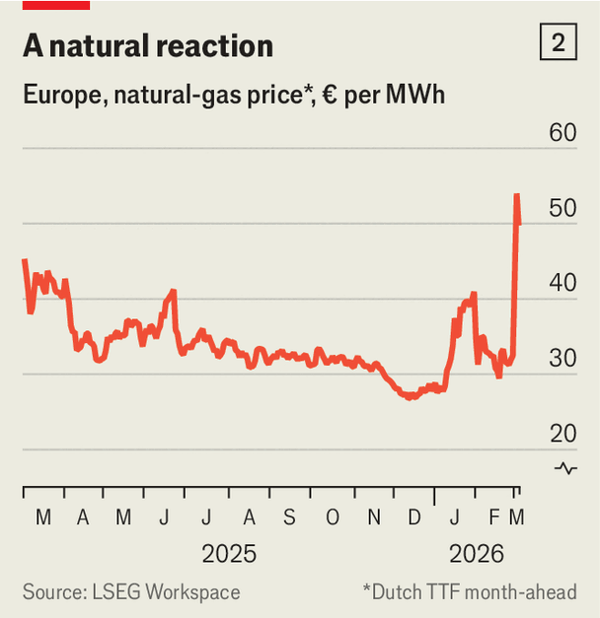

霍尔木兹海峡关闭正在同时冲击石油和天然气:该水道平日承载全球约三分之一的海运原油和五分之一的液化天然气,而3月2日只有5艘油轮通过,远低于2月日均51艘。布伦特原油自2月27日以来上涨15%至每桶84美元,欧洲天然气涨至每兆瓦时50欧元,周涨幅超过55%,而通常经由该海峡运输的原油和成品油合计约为每天1800万桶。

供应缓冲看起来很薄弱。只有约四分之一的原油能通过绕开海峡的沙特和阿联酋管道改道,伊拉克和科威特在分别约3天和14天后就可能触及储存上限,接近每天500万桶的出口风险已占全球产量的5%,而伊拉克已经减产每天160万桶;若中断持续4周,布伦特油价可能接近每桶150美元,而其他地区新增供应即使全部释放也只有每天100万至200万桶,且至少需要6个月。

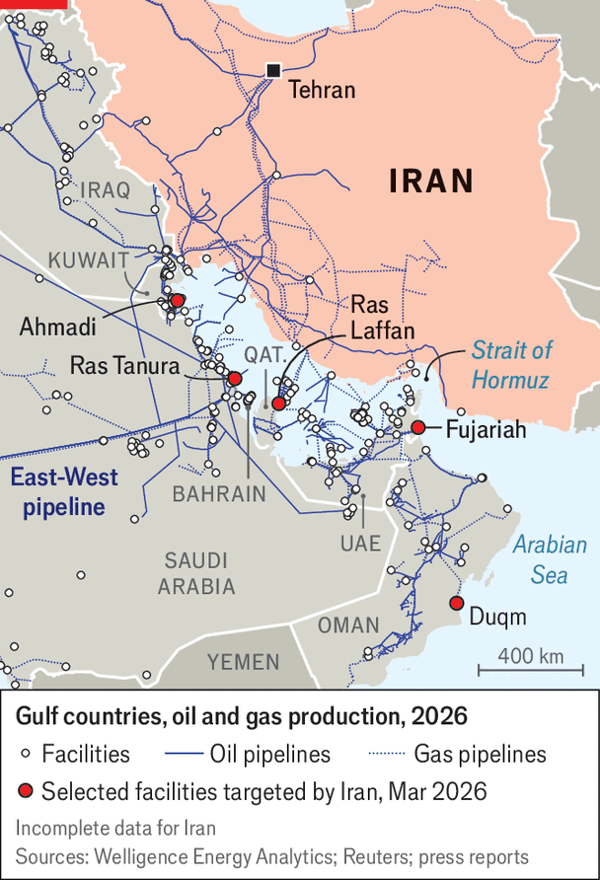

天然气风险甚至更集中。2025年有超过8000万吨液化天然气经过霍尔木兹,已关闭的卡塔尔拉斯拉凡综合设施占全球出口的7500万吨、即17%,且每关闭一周全球供应就减少150万吨;卡塔尔去年分别满足了中国30%、印度45%和巴基斯坦99%的液化天然气进口需求,因此如果出口在3月9日前仍未恢复,欧洲气价可能突破每兆瓦时100欧元。宏观影响也很大:国际货币基金组织估算,油价每上涨10%,次年全球GDP增速下降0.15个百分点、通胀上升0.4个百分点,因此若油价升至每桶100美元,GDP增速约减少0.4个百分点、通胀上升1.2个百分点。

The closure of the Strait of Hormuz is hitting oil and gas simultaneously: the waterway normally carries about one-third of global seaborne crude and one-fifth of LNG, yet only 5 tankers crossed on March 2 versus a February daily average of 51. Brent has risen 15% since February 27 to $84 a barrel, European gas has climbed to EUR50 per MWh, up more than 55% on the week, and the crude plus refined products that usually pass through the strait total about 18m barrels per day.

Supply buffers look thin. Only about a quarter of crude can be rerouted through Saudi and UAE pipelines that bypass the strait, Iraq and Kuwait could hit storage limits in roughly 3 and 14 days respectively, nearly 5m b/d of exports at risk equals 5% of global production, and Iraq has already cut 1.6m b/d; if disruption lasts 4 weeks, Brent could approach $150, while every possible extra source elsewhere would add only 1m-2m b/d and would take at least 6 months.

Gas risk is even more concentrated. More than 80m tonnes of LNG moved through Hormuz in 2025, Qatar’s shut Ras Laffan complex accounted for 75m tonnes or 17% of global exports, and each week of closure removes 1.5m tonnes from world supply; because Qatar supplied 30% of China’s LNG imports, 45% of India’s, and 99% of Pakistan’s last year, European gas could rise beyond EUR100 per MWh if exports do not resume by March 9. The macro impact is also large: the IMF estimates that every 10% oil-price rise cuts next-year global GDP growth by 0.15 percentage points and lifts inflation by 0.4 points, so a move to $100 oil would subtract about 0.4 points from growth and add 1.2 points to inflation.

Source: The nightmare war scenario is becoming reality in energy markets

Subtitle: The longer the war in the Gulf, the harsher the global economic fallout

Dateline: 3月 05, 2026 07:21 上午