在刚果,过去30年西方企业大多在撤离而非投资,而中国实体如今持有该国约90%项目的权益,但美国正在快速加码:美国企业在2025年12月拿到一批矿山与勘探地优先权,华盛顿还向洛比托走廊铁路投入5.53亿美元,并在2026年2月由包含美国政府的Orion CMC同意收购该国唯一西方控制铜钴矿40%的股权。更广泛地看,美国已与20多个国家签署矿产伙伴关系,并把乌克兰、委内瑞拉和格陵兰等地缘动作部分建立在矿产考量上,显示其矿产外交正从零散动作转向高频推进。

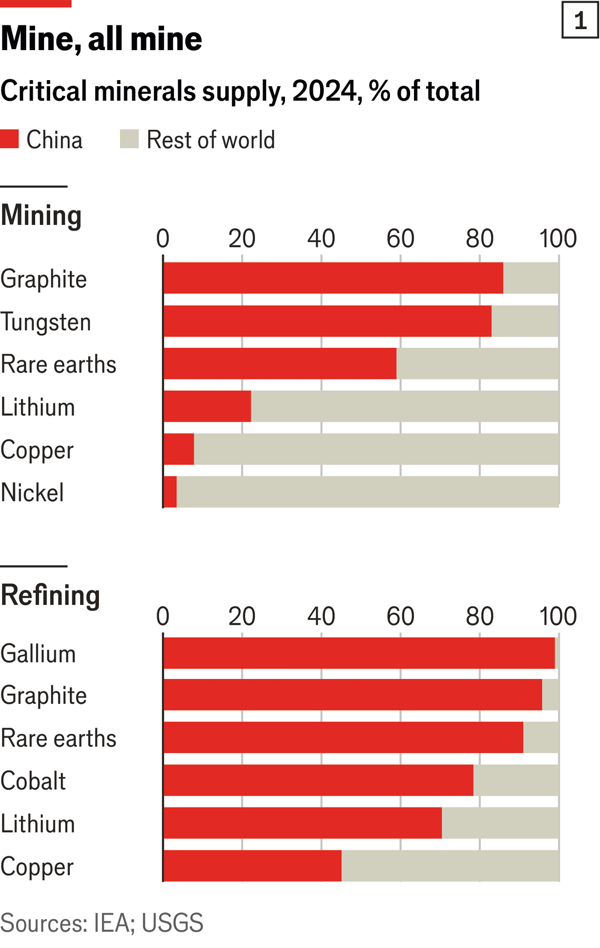

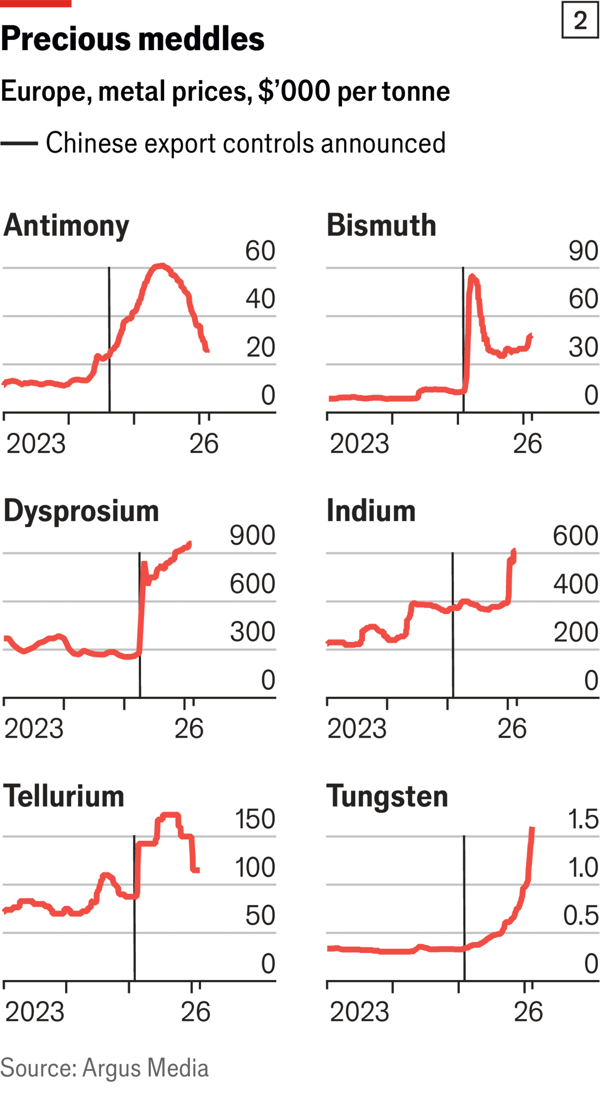

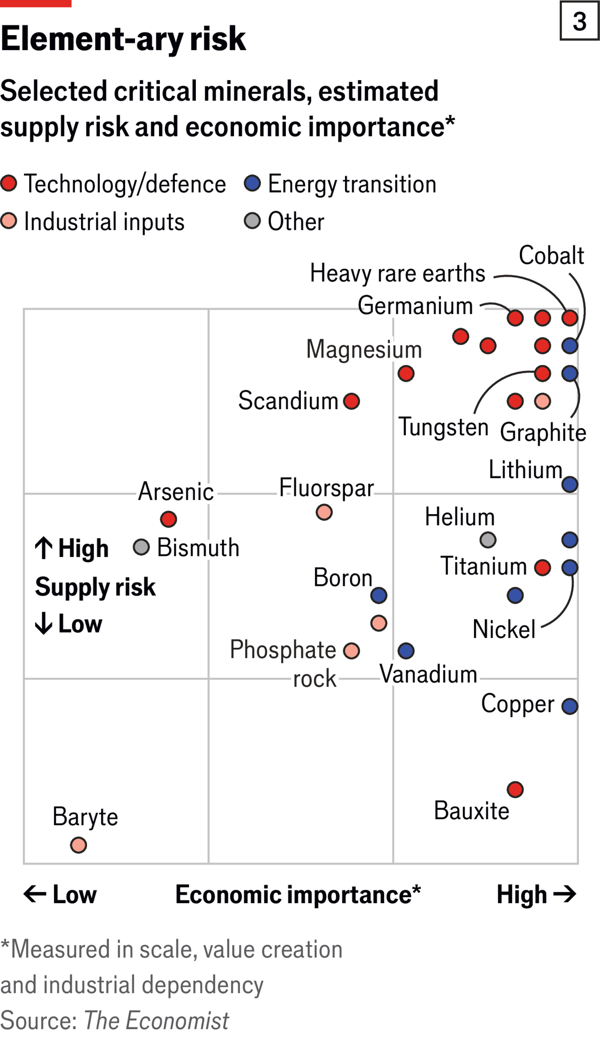

这场竞争的量级很大:中国在关键矿产上仍是“矿山+冶炼”双重主导方,关键矿物范围约30至60种,既包括2025年产量约2900万吨的铜,也包括部分年产仅几十吨的重稀土;2025年4月中国对7种高价值稀土设限并继续限制从锑到钨等约12种矿物,立即冲击军工与汽车供应链。美国的应对覆盖USGS列出的全部60种关键矿物,并用三大杠杆集中干预:截至目前五角大楼自2025年10月起向8个项目投放28亿美元股债,EXIM一年内发出150亿美元贷款意向(含美国稀土4.55亿美元、澳洲钴镍3.5亿美元),能源部批出70亿美元贷款,且新增21项双边协议并谈妥17项。

美国还拟用“库存+保底价”稳定供给:Project Vault以EXIM 100亿美元贷款和20亿美元私资建立民用储备,目标是覆盖数周至数月需求并对部分矿种覆盖最长一年,同时价格保底机制在MP Materials案中设定氧化钕镨10年每公斤110美元底价。核心风险同样可量化:MP保底前均价仅59美元/公斤而同期中国出口价约78美元/公斤,欧洲仅承诺30亿欧元覆盖34种矿物、单矿项目常需数十亿却仅拿到数百万到数千万美元支票,且美国宣布支持Round Top达16亿美元后市场仍普遍怀疑执行与回报,反映“高投入、低确定性”的统计特征。

In Congo, Western firms mostly exited rather than invested over the past 30 years, while Chinese entities now hold stakes in about 90% of projects, but the United States is accelerating quickly: in December 2025 American firms secured first rights to a batch of mines and exploration sites, Washington also put $553 million into the Lobito Corridor railway, and in February 2026 Orion CMC, which includes the US government, agreed to buy a 40% stake in the country’s only Western-controlled copper-cobalt mines. More broadly, the United States has signed mineral partnerships with more than 20 countries and has partly grounded moves in places such as Ukraine, Venezuela, and Greenland in mineral logic, showing a shift from sporadic actions to high-frequency mineral diplomacy.

The scale of the race is large: China remains the dual leader in both mining and refining across critical minerals, the critical-minerals set spans roughly 30 to 60 materials, and it ranges from copper at about 29 million tonnes in 2025 to heavy rare earths with annual output in only tens of tonnes; in April 2025 China restricted seven high-value rare earths and still limits about a dozen minerals from antimony to tungsten, immediately hitting defense and auto supply chains. The US response covers all 60 minerals on the USGS critical list and uses three intervention levers: so far, since October 2025 the Pentagon has committed $2.8 billion in equity and debt to eight projects, EXIM has issued $15 billion in letters of interest over the past year (including $455 million for US rare earths and $350 million for Australian cobalt-nickel), the Department of Energy approved $7 billion in loans, and Washington added 21 bilateral pacts while concluding 17 more negotiations.

The United States is also trying to stabilize supply with “stockpiles plus price floors”: Project Vault combines a $10 billion EXIM loan with $2 billion in private capital to build a civilian reserve targeting coverage from weeks to months, and up to one year for some minerals, while the MP Materials mechanism sets a 10-year $110/kg floor for NdPr oxide. The key risks are also numerical: MP’s pre-floor average was only $59/kg versus about $78/kg for comparable Chinese exports, Europe has committed just €3 billion across 34 minerals, single-mine projects often need billions but frequently receive checks in the millions or tens of millions, and even after a declared $1.6 billion US backing for Round Top, markets still broadly doubt execution and returns, indicating a “high spend, low certainty” pattern.

Source: America’s new era of state-sponsored mining

Subtitle: Desperate to break China’s grip on critical minerals, the Trump administration is splashing cash around the world

Dateline: 2月 26, 2026 04:27 上午 | BELO HORIZONTE, CAPE TOWN, RIYADH AND WASHINGTON, DC