20 世纪 2000 年代初期,海力士半导体(Hynix Semiconductor)因销售额减半且市值跌至 5 亿美元左右而面临破产。经历十年的重组并在 2012 年被 SK 集团收购后,SK 海力士实现了惊人的逆袭。2025 年 5 月,公司市值突破 1 万亿美元,并在 6 月一度超越三星电子成为韩国市值最高的公司。7 月 10 日,该公司在纳斯达克上市,创纪录地募资 265 亿美元。自 2025 年初以来,受季度销售额同比翻两番的推动,其股价飙升了约 1000%。上市所融资金和运营产生的 500 亿美元现金将用于在未来五年内将产能翻倍的计划,包括与三星合作在 2040 年前向龙仁半导体集群投资超 2 万亿美元,以及在韩国西南部投资 2600 亿美元建设新集群。

SK 海力士的成功源于技术灵活性及与三星迥异的企业文化。2010 年代初期,三星控制着内存市场 40% 的份额,而海力士仅占 25%。为了突破物理极限,SK 海力士于 2008 年与 AMD 合作研发堆叠式图形内存,并于 2013 年开发出高带宽内存(HBM)。当三星在 2019 年缩减 HBM 团队时,SK 海力士吸收了流失的工程人才以及英特尔的工程师。与三星残酷的竞争机制不同,SK 海力士倡导合作和扁平化沟通。它还通过记录失败案例来推动技术创新,例如用于散热的“批量回流模塑料底填”技术,帮助其在 2022 年凭借 HBM3 成为英伟达的独家供应商。

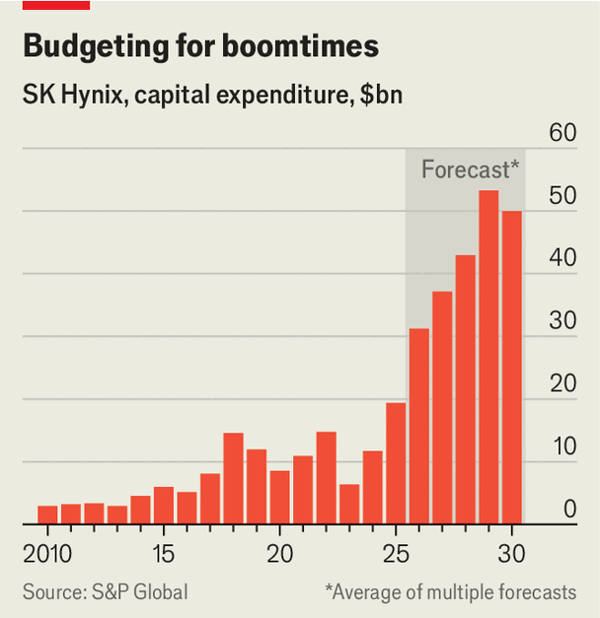

然而,在周期性极强的内存行业中风险依然存在。在 2018 年的行业周期顶点,SK 海力士的资本开支达到 150 亿美元(占营收的 40%),但 2019 年的下行周期导致内存价格减半,公司销售额下降 33%,营业利润暴跌 87%。为防范此类风险,公司承诺将资本开支限制在营收的三分之一以内(过去一年平均为 22%)。分析师警告称,随着三星、美光及中国厂商(如长鑫存储和长江存储)的新产能上线,内存价格可能在 2027 年见顶,并导致 SK 海力士在 2028 年销售额下滑 45%。此外,政治压力也在增加,国内需向西南部转移产能,国外则需在美国扩建,包括计划投资 40 亿美元的印第安纳工厂。

In the early 2000s, Hynix Semiconductor faced collapse as sales halved and market capitalization fell to just above $500 million. Following a decade of restructuring and acquisition by SK Group in 2012, SK Hynix has undergone a spectacular turnaround. In May 2025, its market capitalization crossed $1 trillion. In June, it briefly became South Korea's most valuable company. On July 10th, the firm listed on Nasdaq, raising a record-breaking $26.5 billion. Its stock has surged by around 1,000% since the start of 2025, fueled by a tripling of quarterly sales year-on-year. The listing proceeds and $50 billion of generated cash will fund plans to double capacity over five years, including over $2 trillion of joint investment with Samsung up to 2040 in Yongin and a $260 billion cluster in the south-west.

SK Hynix's success lies in its technological agility and cultural differences from Samsung. In the early 2010s, Samsung controlled 40% of the memory market while Hynix held 25%. Seeking to bypass physical scaling limits, SK Hynix collaborated with AMD in 2008 on stacked graphics memory, leading to the development of High-Bandwidth Memory (HBM) in 2013. When Samsung scaled down its HBM team in 2019, SK Hynix absorbed fleeing talent, alongside delayed Intel engineers. Unlike Samsung's cut-throat meritocracy, SK Hynix fosters a collaborative, flat communication style. It also documents failures to drive innovation, such as "mass reflow-molded underfill" for heat dissipation, allowing it to dominate the HBM3 market in 2022 as Nvidia's sole supplier.

However, risks remain in the notoriously cyclical memory industry. During the 2018 peak, SK Hynix's capital expenditure reached $15 billion (40% of revenue), but a 2019 downturn halved memory prices, causing sales to drop by 33% and operating profits to collapse by 87%. To mitigate this, the company has capped capital spending at a third of revenue, averaging 22% over the past year. Analysts warn that memory prices could peak in 2027, potentially precipitating a 45% sales decline by 2028 as capacity increases from Samsung, Micron, and Chinese rivals (CXMT and YMTC) come online. Political pressure also grows, both domestically to build in South Korea's south-west and internationally to expand in the US, where a $4 billion Indiana plant is planned.

Source: How SK Hynix became the king of advanced memory chips

Subtitle: Its advantages will not protect it if demand falters

Dateline: Jul 16, 2026 06:53 AM | SEOUL